Comprehensive Guide to FL Automobile Insurance: Strategic Protection for 2026

- siinsuranceflorida

- Mar 24

- 14 min read

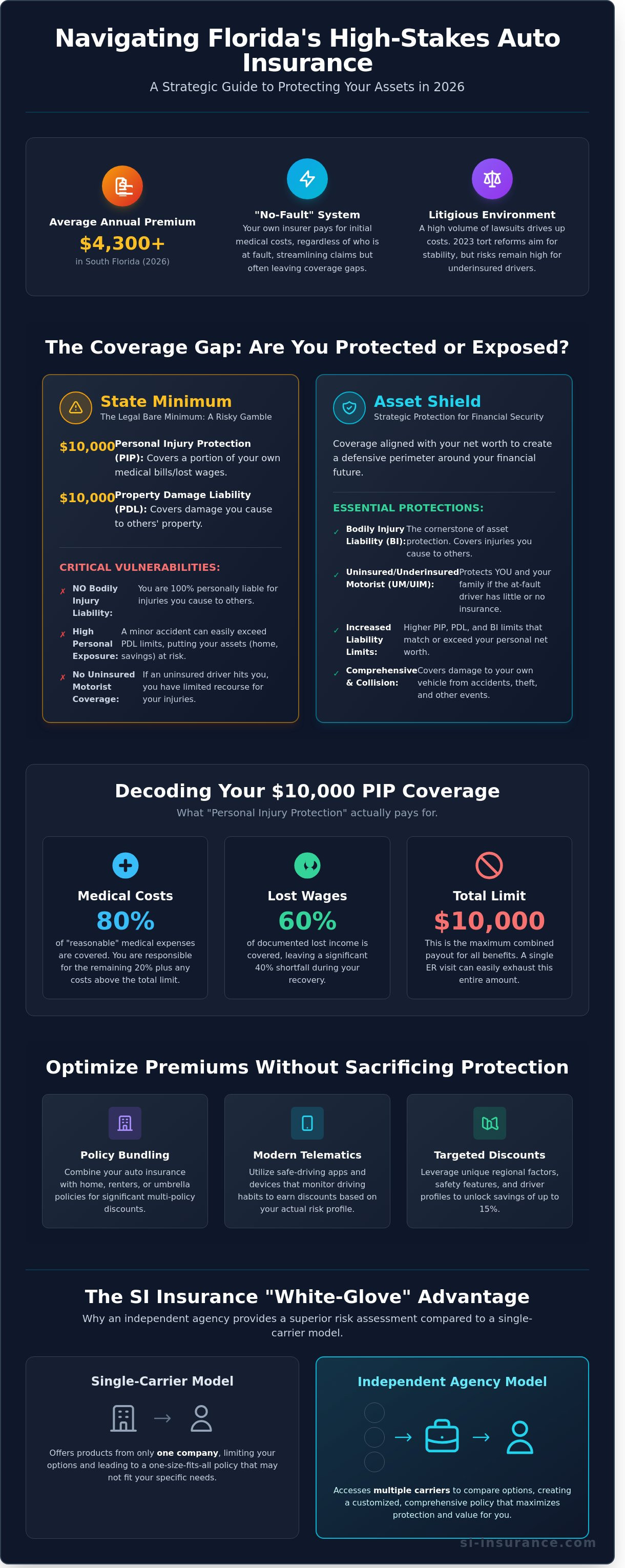

The reality of operating a vehicle in the Sunshine State has shifted from a simple matter of compliance to a high-stakes exercise in risk mitigation where a single oversight in your fl automobile insurance policy can expose your entire portfolio to predatory litigation. With South Florida drivers currently facing average annual premiums exceeding $4,300 as we enter 2026, the margin for error in your coverage selection has effectively vanished. You're likely aware that the state’s complex No-Fault statutes and the recent legislative reforms of 2023 haven't yet provided the immediate relief many expected for their personal balance sheets. It's frustrating to watch your costs climb while you remain uncertain if your current liability limits are actually sufficient to shield your assets in such a litigious environment.

SI Insurance is here to provide the strategic clarity you need to move beyond basic registration requirements and into a position of absolute financial security. We'll examine how to calibrate your liability thresholds for maximum protection, clarify the intricacies of Personal Injury Protection, and identify specific regional discounts that can reduce your overhead by up to 15% without compromising your safety.

Key Takeaways

Gain clarity on Florida’s "No-Fault" mandates to ensure your policy provides the immediate medical and property damage coverage required by law.

Learn the strategic importance of aligning your fl automobile insurance limits with your personal net worth to effectively shield your assets from litigation.

Identify the specific environmental and traffic risks unique to South Florida and how these regional factors influence your total risk profile.

Discover how to optimize your insurance costs by leveraging policy bundling and modern telematics without compromising on the quality of your protection.

See why a "white-glove" independent agency approach offers a more comprehensive risk assessment than traditional single-carrier insurance models.

Table of Contents The Landscape of FL Automobile Insurance in 2026 Decoding Coverage Tiers: From Compliance to Total Protection The South Florida Risk Profile: Broward County Dynamics Strategic Methods for Optimizing Your Insurance Premiums Navigating the Market with Si Insurance Agency

The Landscape of FL Automobile Insurance in 2026

Florida’s legal framework utilizes a no-fault insurance system designed to streamline medical claims following a collision. This structure ensures that your own provider pays for your immediate medical needs regardless of who caused the accident. Following the legislative adjustments that took effect on July 1, 2025, the market has stabilized slightly, yet premiums remain 15% higher than the national average. Managing your fl automobile insurance requires a strategic understanding of these moving parts to ensure your assets stay protected.

To better understand this concept, watch this helpful video:

Legislative reforms passed in early 2025 have fundamentally altered how insurers assess risk and manage litigation. These changes were intended to reduce the volume of frivolous lawsuits that historically drove up costs for every driver in the state. By January 1, 2026, the impact of the Tort Reform Act of 2023 became fully integrated into policy pricing, shifting the focus toward underwriting excellence and more accurate risk mitigation. While these laws aim for long term stability, the immediate reality for many drivers is a market that feels both exclusive and demanding.

The Mechanics of No-Fault Insurance

Personal Injury Protection, commonly known as PIP, functions as the primary mechanism for medical recovery. It's designed to cover 80% of your medical costs and 60% of lost wages, capped at a $10,000 limit. This system provides a quick financial buffer, but it often leaves a gap that drivers must cover out of pocket. Many policyholders find it frustrating that Florida doesn't mandate Bodily Injury coverage, leaving them vulnerable if they're hit by an underinsured driver.

The Permanent Injury Threshold acts as the gatekeeper for further legal action. You can't pursue a claim for non-economic damages, such as pain and suffering, unless a medical professional confirms a permanent loss of a bodily function or significant scarring. It's a high bar that prevents minor claims from clogging the court system. Because of this, securing a robust fl automobile insurance policy involves looking far beyond the state's bare minimum requirements.

Mandatory vs. Recommended Coverage

Florida law requires a minimum of $10,000 in PIP and $10,000 in Property Damage Liability (PDL). Relying on these "minimum-only" policies is a dangerous gamble, especially in high-traffic corridors like Sunrise and Pompano Beach. A single multi-car accident can easily result in property damage exceeding $15,000, leaving you personally liable for the difference. We recommend a more bespoke approach to coverage that aligns with your total net worth and strategic risk profile.

The Financial Responsibility Law dictates that drivers must provide proof of ability to pay for damages in accidents involving bodily injury or face the immediate suspension of their driving privileges and vehicle registrations. This law typically triggers after an accident where you're at fault and didn't carry Bodily Injury Liability. It's a harsh reminder that the state's "minimum" isn't a safety net; it's just the starting point for legal compliance.

Decoding Coverage Tiers: From Compliance to Total Protection

Florida's roads demand more than just a basic policy. While many drivers prioritize the lowest monthly premium, a sophisticated approach to fl automobile insurance requires a deep understanding of how coverage scales with your financial responsibility. It's not just about meeting a legal standard; it's about building a defensive perimeter around your wealth. When you're operating in a high-stakes environment, your policy should function as a strategic asset rather than a mere monthly expense.

Liability Limits and Asset Shielding

The gap between state minimums and professional-grade protection is vast. Most drivers start by looking at the FLHSMV insurance requirements, which only mandate $10,000 in Personal Injury Protection and $10,000 in Property Damage Liability. For a professional with a home, retirement accounts, and liquid assets, these limits are dangerously low. A 10/20/10 policy offers almost zero protection against a modern personal injury lawsuit. Transitioning to a 100/300/100 or 250/500/100 limit structure is a necessary step in risk mitigation.

A consultant at SI Insurance Agency doesn't just sell a policy; they perform a strategic alignment of your limits with your actual risk exposure. If your net worth exceeds $500,000, even the highest auto limits might not be enough. This is where Personal Umbrella Insurance becomes relevant. It acts as a secondary shield, providing $1 million to $5 million in additional liability protection that kicks in once your primary auto policy is exhausted. This ensures that a single lapse in judgment on the road doesn't jeopardize your long-term financial stability.

The Uninsured Motorist Necessity

Florida consistently ranks among the highest in the nation for drivers without coverage. According to 2021 data from the Insurance Research Council, 20.4% of Florida motorists are completely uninsured. This means there's a one-in-five chance that the person who hits you won't have the funds to pay for your medical bills or lost wages. Uninsured Motorist (UM) coverage is your primary defense in this scenario. It's a non-negotiable component of a robust fl automobile insurance strategy.

Stacked UM: This option allows you to combine coverage limits across multiple vehicles on your policy. If you have two cars with $100,000 in UM, you effectively have $200,000 in protection available for a single accident.

Non-Stacked UM: This limit applies only to the vehicle involved in the accident. It offers less flexibility but comes with a slightly lower premium.

Physical asset protection rounds out the policy through Comprehensive and Collision coverages. Collision handles impacts with other vehicles or objects, while Comprehensive covers non-collision events like theft, fire, or the frequent tropical storms that impact the region. Protecting the vehicle itself is important, but it's the liability and UM components that prevent a single accident from becoming a life-altering financial event. You can begin a tailored policy review to ensure your current limits reflect your current success.

The South Florida Risk Profile: Broward County Dynamics

Broward County isn't just another South Florida suburb; it's a high-velocity environment where strategic risk management is mandatory. In 2023, Florida Highway Safety and Motor Vehicles reported over 38,000 crashes in Broward County alone. This high volume directly influences how fl automobile insurance premiums are calculated for residents in Sunrise and Pompano Beach. Choosing a policy based solely on the lowest monthly premium often leaves a driver exposed to the 24.1% of Florida motorists who remain uninsured. We find that elite drivers require a more calculated approach, ensuring that their coverage isn't just a legal formality but a robust financial shield.

The reality of South Florida driving involves a mix of high-speed interstate travel and dense urban congestion. When you're navigating the Sawgrass Expressway or I-95, the margin for error is razor-thin. A "cheap" policy might save $50 a month, but it can lead to $50,000 in out-of-pocket expenses after a single multi-vehicle incident. SI Insurance Agency focuses on underwriting excellence to prevent these catastrophic gaps. We treat your policy as a bespoke risk transfer mechanism, prioritizing long-term stability over short-term savings. Our team acts as a strategic guardian, analyzing local traffic patterns to ensure your liability limits reflect the actual costs of modern medical care and vehicle replacement.

High-Traffic Hazards in Sunrise and Pompano

High-accident corridors like the intersection of Sunrise Boulevard and University Drive or the Atlantic Boulevard stretch in Pompano Beach necessitate higher property damage limits. In 2023, the average cost of a new vehicle exceeded $48,000; a standard $10,000 property damage limit is statistically insufficient. Local law enforcement in Broward County utilizes sophisticated crash reporting systems that insurers use to adjust rates in real time. We help you understand these metrics, ensuring your fl automobile insurance provides strategic alignment with the specific hazards of your daily commute.

SR 84 and I-595 Interchange: A primary zone for high-impact collisions requiring enhanced bodily injury protection.

US-1 Corridors: Frequent stop-and-go traffic increases the likelihood of rear-end accidents and complex liability claims.

Commercial Density: High volumes of delivery trucks in Pompano Beach industrial zones increase the risk of accidents with commercial entities.

Weather, Flood, and Comprehensive Risks

Standard policies often fail to distinguish between collision damage and environmental hazards. The historic April 2023 Fort Lauderdale flood, which dropped 25 inches of rain in 24 hours, proved that many drivers don't understand their comprehensive coverage. Without specific flood-related vehicle protection, a submerged car becomes a total loss with no recourse. We advocate for maintaining high-level comprehensive coverage throughout the year, not just during the peak of hurricane season from June to November.

SI Insurance Agency assists clients by performing a rigorous analysis of their storage and commuting habits. If you're parking in low-lying areas of Pompano Beach, your risk profile differs significantly from someone in a high-rise in Sunrise. We ensure your policy includes provisions for rising water, windborne debris, and seasonal storm surges. This meticulous attention to detail is what defines our white-glove service. It's about foresight; we prepare your portfolio for the 100-year storm before the clouds even gather. Our goal is to provide intellectual confidence, knowing your assets are protected by a steady and deliberate risk mitigation strategy.

Strategic Methods for Optimizing Your Insurance Premiums

Achieving a balance between comprehensive coverage and fiscal responsibility requires more than just a cursory glance at monthly quotes. It demands a calculated approach to risk management. Many drivers view their fl automobile insurance as a fixed cost, yet it's actually a dynamic variable that responds to specific strategic adjustments. By treating your policy as an evolving financial asset, you can secure superior protection while minimizing unnecessary capital outflow. This process involves a meticulous review of how your lifestyle choices and financial habits influence the mathematical models used by carriers.

The Art of Policy Bundling

Consolidating your diverse insurance needs under a single carrier remains one of the most effective methods for immediate premium reduction. Most major Florida insurers provide a multi-policy discount ranging from 15% to 22% when you combine auto, homeowners, and umbrella coverage. This strategic alignment does more than just lower costs; it streamlines your administrative burden by centralizing your risk portfolio. For example, a resident in Sunrise recently restructured their coverage by moving their property and auto policies to a single provider. This transition resulted in a verified annual savings of $842, effectively funding their umbrella policy for the entire year without increasing their total expenditure.

Underwriting Excellence and Discounts

Your premium is a reflection of your individual risk profile, which underwriters analyze with extreme precision. Data from 2023 Florida insurance market reports indicates that drivers with credit scores above 750 often pay 31% less than those with average scores. Maintaining a pristine driving record is equally vital. Beyond these foundational factors, SI Insurance recommends proactive measures like completing an approved defensive driving course. These courses typically trigger a 10% discount that remains active for three years. You should also consider the following overlooked opportunities for premium optimization:

Telematics Integration: Utilizing usage-based insurance (UBI) programs can lead to savings of up to 40% for disciplined drivers who demonstrate safe braking and acceleration habits.

Educational Incentives: Full-time students under age 25 who maintain a 3.0 GPA or higher can often secure a Good Student discount, reducing their specific portion of the premium by 15%.

Safety and Security Features: Vehicles equipped with adaptive cruise control, lane-departure warnings, or specialized anti-theft systems often qualify for equipment-specific credits.

Adjusting your deductible is another lever for managing cash flow against long-term risk retention. While a $500 deductible offers immediate peace of mind, increasing that threshold to $1,000 can lower your comprehensive and collision premiums by 15% to 30%. This decision should be based on your liquid savings. If you have the capital to cover a higher out-of-pocket expense in the event of a claim, retaining that risk yourself is a savvy financial move. We view these adjustments as bespoke risk transfer, ensuring your fl automobile insurance stays perfectly synchronized with your current lifestyle and financial goals. If you're ready to refine your coverage, it's time to schedule a strategic policy audit with our team today.

Stability in your insurance costs is not a matter of luck; it's the result of rigorous analysis and foresight. By identifying every available discount and aligning your deductibles with your actual risk tolerance, you transform from a passive policyholder into a strategic manager of your own security. Our firm remains committed to guiding you through these complex decisions with the precision and expertise you expect from an elite consultancy.

Navigating the Market with Si Insurance Agency

Choosing the right coverage requires more than a cursory glance at monthly premiums. While captive agents are bound to the limitations of a single carrier's underwriting appetite, Si Insurance Agency functions as an independent powerhouse. We leverage a network of more than 40 top-tier carriers to ensure your protection isn't a compromise. Our team treats every policy as a bespoke risk transfer project. This means we don't just sell you a plan; we engineer a defense for your assets. Our offices in Sunrise and Pompano Beach aren't just storefronts. They're command centers where local experts dissect the complexities of fl automobile insurance to find the exact fit for your lifestyle.

We believe in a white-glove approach that begins with a meticulous risk analysis. We don't guess. We analyze. By conducting a granular assessment of your current liability exposure, our team identifies gaps that automated systems often overlook. This strategic alignment ensures that every dollar spent on premiums translates into a tangible shield against financial loss. As of June 2024, Florida's insurance landscape remains one of the most volatile in the nation. Relying on a single carrier limits your options when rates fluctuate or underwriting guidelines change. Our independent status allows us to pivot on your behalf, maintaining your security regardless of market shifts.

Your Strategic Guardian in Broward County

The role of a true advisor is to act as an interpreter. Insurance contracts are dense, filled with technical jargon that can obscure the actual level of protection provided. We translate these complexities into clear, actionable intelligence. Our methodology involves matching you with carriers that demonstrate long-term fiscal stability and a history of fair claims processing. Algorithms don't understand the nuances of a multi-generational household or the specific risks associated with South Florida's seasonal traffic patterns. We do. This human connection ensures that your fl automobile insurance policy is built on logic and foresight, not just a generic data point.

Next Steps: Securing Your Future

Moving from uncertainty to absolute security is a logical, step-by-step progression. We've refined our onboarding process to be as efficient as it is thorough. It starts with a conversation where we listen more than we talk. This allows us to understand the specific financial landscape you're protecting. To make your first consultation with a Si Insurance expert as productive as possible, please have the following items ready:

Your current policy declarations page to establish a baseline for comparison.

Vehicle Identification Numbers (VIN) for all automobiles in your household.

Driver's license details and claims history for all household members.

A brief summary of your primary financial goals and liability concerns.

Our experts will take this information and perform a deep-dive analysis. We'll present you with a strategic selection of options that prioritize both coverage integrity and cost-efficiency. There's no pressure to rush. We provide the data, the context, and the professional recommendation, leaving you empowered to make an informed decision. Your financial future is too important to leave to chance or a simplified web form. It's time to experience the difference that elite expertise and personalized care can make. Secure your strategic auto insurance quote today and take the first step toward a more secure tomorrow.

Advancing Your Strategy for the 2026 Insurance Landscape

Securing a resilient financial future requires a move beyond the basic $10,000 personal injury protection mandates that many drivers rely on today. As traffic density and litigation rates in Broward County continue to evolve, your approach to fl automobile insurance must prioritize comprehensive risk transfer over simple regulatory compliance. We've seen that strategic premium optimization is most effective when it leverages data-driven insights and a diverse portfolio of coverage options. It's about finding that precise balance where cost meets absolute security.

Si Insurance Agency brings a sophisticated perspective to this process, rooted in our founding principles of strategic risk mitigation. With our physical presence in Sunrise and Pompano Beach, we provide the local expertise necessary to navigate South Florida's unique driving environment. Our clients benefit from direct access to a premier network of 30 top-rated insurance carriers, ensuring that every policy is engineered for high-value protection. You don't have to navigate these complex financial decisions alone when you have a dedicated partner focused on your long-term stability. We're ready to help you secure the elite protection your lifestyle demands.

Frequently Asked Questions

Is Bodily Injury Liability mandatory in Florida for 2026?

As of the current 2024 legislative outlook, Bodily Injury Liability (BIL) isn't a mandatory requirement for most private motorists under Florida's existing "No-Fault" statutes. You're only legally required to carry $10,000 in Personal Injury Protection and $10,000 in Property Damage Liability. However, if you've been convicted of a DUI or were at fault in a crash involving injuries, the Financial Responsibility Law requires you to carry BIL limits of at least $10,000 per person and $20,000 per occurrence.

What happens if I drive in Florida without insurance?

Driving without valid fl automobile insurance leads to an immediate suspension of your driving privileges and vehicle registration by the Department of Highway Safety and Motor Vehicles. You'll face a $150 reinstatement fee for a first offense, which climbs to $500 for subsequent violations within a three year period. Beyond these administrative penalties, you lose the strategic protection of limited liability, leaving your personal assets exposed to litigation after a collision.

How does the "No-Fault" law affect my ability to sue after an accident?

Florida's No-Fault system requires you to seek initial medical compensation through your own PIP coverage regardless of who caused the event. You can only initiate a lawsuit for pain and suffering if your injuries meet the "tort threshold" defined in Florida Statute 627.737. This requires proving a permanent loss of a bodily function, significant scarring, or death. Approximately 80% of minor accident claims are resolved through PIP without ever entering the court system.

Can I use out-of-state insurance if I am a part-time Florida resident?

You must register your vehicle and obtain a Florida specific policy if your car is physically present in the state for more than 90 days during the preceding 365 days. These days don't need to be consecutive to trigger the legal requirement. Relying on an out-of-state policy for a vehicle primarily garaged in Florida creates a significant risk of claim denial during the underwriting review process following a loss.

Why is car insurance in Broward County more expensive than in other regions?

Broward County premiums are higher because the region experienced a 15% higher rate of litigated claims compared to the state average in recent reporting cycles. High population density in cities like Fort Lauderdale increases the statistical frequency of multi-vehicle accidents and fraudulent PIP claims. Insurance carriers adjust their strategic risk pricing to account for these localized hazards and the increased cost of legal defense in South Florida.

What is the difference between "Stacked" and "Non-Stacked" UM coverage?

Stacked Uninsured Motorist coverage allows you to combine the limits of all vehicles insured under your policy or across multiple policies in your household. If you have two cars with $50,000 in coverage each, stacking provides a $100,000 total limit for a single accident. Non-stacked coverage limits you to the $50,000 stated on the individual vehicle. It's a vital component of bespoke risk transfer for families with multiple drivers.

Does Florida auto insurance cover damage from a hurricane or flood?

Your fl automobile insurance policy covers hurricane and flood damage only if you've elected to include comprehensive coverage. While PIP and PDL are mandatory, they don't protect your vehicle from rising water or windborne debris. Data from the 2022 hurricane season showed that comprehensive claims accounted for billions in vehicle losses, proving that this elective coverage is essential for long term asset preservation in coastal environments.

How often should I review my Florida automobile insurance policy?

You should conduct a formal review of your insurance portfolio at least once every 12 months or immediately following major life milestones. Events like purchasing a secondary residence, adding a teenage driver, or changing your daily commute by more than 10 miles impact your risk profile. Regular audits ensure your coverage limits maintain strategic alignment with your evolving net worth and the fluctuating costs of medical care and vehicle repairs.

Disclaimer

Disclaimer & Disclosure: Articles published on this website may be produced with the assistance of automated content generation tools and are reviewed periodically by our team. The content is provided for informational purposes only and does not constitute insurance advice, legal advice, or an offer of coverage. Insurance policies, coverage options, exclusions, and availability vary by carrier and state. For personalized guidance or policy recommendations, please contact a licensed insurance agent at our office.

Comments