Does Home Insurance Cover Jewelry in Florida? A Strategic Guide for 2026

- siinsuranceflorida

- Mar 22

- 14 min read

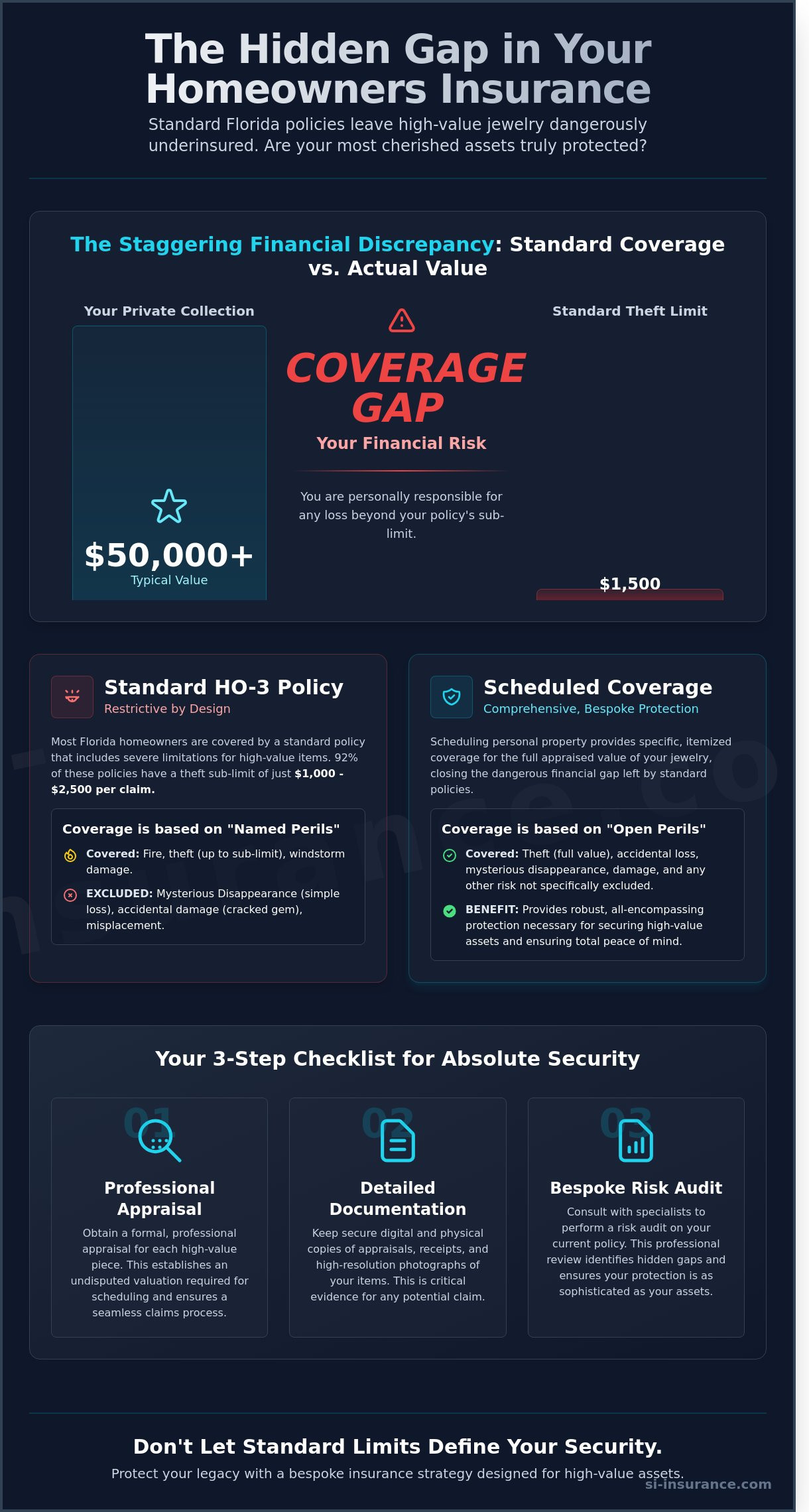

Did you know that while your private collection might be valued at over $50,000, a standard Florida homeowners policy often caps theft recovery for precious items at a mere $1,500 per claim? It's a staggering discrepancy that leaves many high-net-worth individuals in Sunrise and Pompano Beach vulnerable to significant financial loss. You likely assume your most cherished assets are safe within your home's walls, but understanding exactly how does home insurance cover jewelry in 2026 requires a look at the technical reality of sub-limits and named perils. SI Insurance understands that settling for standard coverage is a strategic risk you can't afford to take.

We'll bridge the gap between basic coverage and absolute security by detailing the limitations of off-the-shelf policies and the specific risks inherent to the Florida market. You'll discover how to strategically utilize scheduled personal property endorsements and bespoke risk transfer solutions to protect your legacy pieces fully. This guide provides the precise underwriting insights you need to ensure your insurance portfolio is as sophisticated as the assets it protects, offering you total peace of mind.

Key Takeaways

Identify the inherent limitations of standard Florida HO-3 policies and understand how restrictive internal sub-limits can leave your most significant jewelry investments dangerously underinsured.

Gain a clear perspective on the question "does home insurance cover jewelry" by analyzing the "Named Perils" constraints that often exclude coverage for accidental loss or simple misplacement.

Explore the strategic shift from basic personal property limits to "Scheduled" coverage, which offers the robust "Open Perils" protection necessary for securing high-value assets.

Learn the essential requirements for professional appraisals and documentation to ensure your claims process is seamless and your asset valuation remains undisputed.

Discover how a bespoke risk audit by the specialists at SI Insurance can identify hidden gaps in your current policy, providing the sophisticated protection your legacy deserves.

Table of Contents Understanding Jewelry Coverage Within a Standard Florida Homeowners Policy The Technical Reality: Sub-limits and Named Perils in Broward County Strategic Enhancements: Scheduled Personal Property vs. Standalone Jewelry Insurance Risk Mitigation: The Appraisal and Documentation Process for Florida Residents Securing Your Legacy: Why SI Insurance is Your Strategic Guardian

Understanding Jewelry Coverage Within a Standard Florida Homeowners Policy

Protecting private assets requires a clear-eyed look at the fine print of your insurance documents. Most property owners in the Sunshine State utilize an HO-3 policy, which is the industry standard for single-family residences. While this Standard Florida Homeowners Policy offers a baseline of protection for your belongings, it treats high-value items like watches and engagement rings with a specific set of restrictions. When clients ask, "does home insurance cover jewelry," they're often surprised to learn that coverage isn't a simple "yes" or "no" but a matter of specific peril definitions and internal caps.

To better understand this concept, watch this helpful video:

Standard policies classify your possessions as "contents," which typically receive coverage for about 50% of your dwelling's total value. However, jewelry is unique because it's highly portable and susceptible to theft. This creates a strategic misalignment if you own bespoke pieces that exceed the basic policy limits. A jewelry sub-limit is a contractual cap on the maximum recovery amount for specific high-value categories, ensuring the insurer's exposure remains within predictable bounds. If you haven't moved your items into a "scheduled" status, they remain subject to these restrictive "unscheduled" limits that rarely reflect true market value.

The Standard Sub-Limit Reality

In the Florida market, approximately 92% of standard HO-3 policies include a theft sub-limit that ranges from $1,000 to $2,500 for the entire claim, not per item. These caps exist as a form of risk mitigation for the carrier; they prevent massive payouts for items that are easily stolen or lost. While a fire might allow you to claim the full value of your wardrobe, a theft is strictly capped. As of the 2024 filing year, these limits haven't kept pace with the rising costs of precious metals and stones.

Perils Covered vs. Perils Excluded

Your policy operates on a "Named Perils" basis for personal property, covering events like fire, lightning, and windstorm damage. If a Category 4 hurricane causes structural failure and your jewelry is lost in the wreckage, you're likely covered up to your sub-limit. The danger lies in "Mysterious Disappearance," which is the industry term for simply losing an item. If you lose a ring while swimming at a Clearwater beach, a standard policy offers zero recovery. This gap is why asking "does home insurance cover jewelry" requires a deep dive into the specific cause of the loss. Most basic policies also exclude coverage for "breakage" or accidental damage, such as a cracked emerald or a snapped platinum chain.

Strategic alignment between your asset portfolio and your insurance policy is the only way to ensure absolute security. Relying on default settings in a standard contract often results in a significant financial shortfall during a claim. By recognizing the difference between a named peril and an accidental loss, you can better coordinate with an advisor to implement a bespoke risk transfer solution that actually protects your investments.

The Technical Reality: Sub-limits and Named Perils in Broward County

Most homeowners assume their policy acts as a comprehensive safety net for every item within their four walls. The reality is far more restrictive. When you ask, "does home insurance cover jewelry," the answer is technically yes, but the coverage is often throttled by "Special Limits of Liability." In Florida, most standard HO-3 policies cap the payout for the theft of jewelry, watches, and furs at a meager $1,500. If you own a single engagement ring or a luxury timepiece, this sub-limit represents a massive gap in your financial protection. It's a strategic oversight to rely on basic policy language for assets that carry significant market value.

The geographic context of Broward County adds another layer of complexity to these claims. According to 2023 crime data, South Florida continues to experience property crime rates that sit roughly 15% higher than the national average in specific high-value zip codes. This elevated risk profile means local carriers are incredibly precise with their underwriting. They don't just look at what you own; they look at the likelihood of a "Named Peril," such as theft or fire, occurring in your specific neighborhood. If your policy only covers named perils, and your diamond falls out of its setting while you're at the beach, you likely won't see a dime. That isn't a theft or a fire, so it isn't covered.

You also have to account for the deductible, which can effectively erode a smaller claim. In Florida, it's common to see an "All Other Peril" deductible of $2,500 or even $5,000. If a $3,000 necklace is stolen, and your deductible is $2,500, the insurance carrier's liability is only $500. This makes the standard policy almost useless for individual items that aren't specifically listed. To avoid this, many clients choose to invest in Scheduled Personal Property, which bypasses the deductible and provides "open peril" coverage for a broader range of mishaps.

Actual Cash Value vs. Replacement Cost

The method your carrier uses to calculate a payout can lead to a shocking financial shortfall. Actual Cash Value (ACV) factors in depreciation, meaning a watch you bought for $8,000 in 2018 might only be valued at $4,500 today. Conversely, Replacement Cost coverage is designed to pay what it actually costs to buy that item at current market prices. Given that gold prices hit record highs of over $2,400 an ounce in 2024, an ACV policy simply won't keep pace with the market. Selecting Replacement Cost is a necessary move for anyone holding precious metals or stones that appreciate over time.

Florida Regulatory Nuances

Florida's insurance landscape is governed by specific statutes, such as Chapter 627, which dictates how personal property claims are handled. One common pitfall for residents is the "Proof of Loss" requirement. In Florida, you typically have a 60-day window to provide a detailed, sworn statement regarding your loss, including appraisals and receipts. Failing to meet this deadline can result in a claim denial. Working with a local Sunrise insurance agency is the most effective way to ensure your documentation meets regional carrier standards before a loss occurs. If you're concerned about your current coverage limits, you should request a strategic policy review to identify any hidden vulnerabilities in your personal property limits.

Strategic Enhancements: Scheduled Personal Property vs. Standalone Jewelry Insurance

While a basic HO-3 policy provides a foundational layer of protection, it's rarely enough for high-value assets. Most Florida homeowners eventually ask, does home insurance cover jewelry with enough depth to replace a $15,000 engagement ring? The answer is usually found in a "Scheduled Personal Property" endorsement. This strategic enhancement moves your coverage from a "Named Perils" framework to an "Open Perils" model. This means that instead of only being covered for specific events like fire or lightning, your items are protected against all risks unless the policy explicitly excludes them. This distinction is critical because standard policies often exclude damage from accidental loss, whereas a scheduled endorsement provides a much broader safety net for the delicate craftsmanship of high-end jewelry.

One of the most immediate financial benefits of scheduling an item is the removal of the standard barrier to recovery. Scheduling an item usually eliminates the deductible for that specific piece. If you experience a loss, you won't have to pay your $1,000 or $2,500 deductible before the insurance company issues a check. This ensures that your liquidity isn't impacted during the replacement process. Many policies also include special limits of liability for certain valuable items, which is why a strategic shift to scheduled coverage is necessary for any piece valued over $1,500. By identifying each piece individually in your policy, you ensure that the underwriting reflects the true market value of your collection.

The Benefits of a Policy Rider (Endorsement)

Choosing a rider, or endorsement, offers a streamlined approach to asset management. You'll deal with one bill, one agent, and one cohesive strategy. In 2024, the cost for this protection in Florida typically ranges from $1 to $2 for every $100 of appraised value. This means a $10,000 necklace would cost roughly $150 annually to schedule. This endorsement also covers "mysterious disappearance," which is a vital protection for jewelry. If you realize your ring is missing but don't know when or where it happened, a standard policy won't help. A rider ensures that accidental breakage, such as a cracked emerald or a snapped gold chain, is fully covered under your existing home policy structure.

When Standalone Coverage is the Superior Choice

Specialized jewelry insurance is often the preferred route for high-net-worth individuals in Pompano Beach who want to protect their home insurance claims history. Filing a $3,000 claim for a lost earring on your homeowners policy can lead to a premium hike or even a non-renewal notice at the end of the term. By using a standalone policy, you keep these smaller, frequent risks separate from your primary property coverage. These bespoke policies often feature "agreed value" terms. Unlike standard "actual cash value" settlements, agreed value ensures you receive the full appraised amount without depreciation. It's a calculated decision that answers the question of how does home insurance cover jewelry by providing a more surgical, specialized alternative to the standard homeowners endorsement for collections valued at $75,000 or more.

Risk Mitigation: The Appraisal and Documentation Process for Florida Residents

When clients ask does home insurance cover jewelry, the answer usually hinges on the quality of their paperwork. For any piece valued over $2,500, a professional appraisal isn't just a recommendation; it's a mandatory component of a sophisticated risk management strategy. In Broward County, residents should seek out GIA-certified professionals or established local appraisers who understand the specific market volatility of the South Florida region. Relying on a five-year-old valuation in 2026 is a significant liability. Gold prices and diamond scarcity have shifted drastically since 2021, meaning an outdated appraisal could leave you underinsured by 30% or more. A digital inventory featuring high-resolution photography provides the forensic evidence required to substantiate a claim during the underwriting or recovery process.

Maintaining a digital vault for these records is essential for rapid recovery. You should store copies of your appraisals, original sales receipts, and 360-degree videos of the items in a secure, cloud-based environment. This ensures that even if your home is compromised by a hurricane or a fire, your documentation remains intact. Modern insurance carriers prioritize claimants who can provide clear, timestamped evidence of an item's condition and existence. This methodical approach to record-keeping transforms a potential administrative nightmare into a streamlined financial transaction.

What a Professional Appraisal Must Include

To secure an "Agreed Value" clause, your documentation must be exhaustive. It needs to specify the four Cs: cut, color, clarity, and carat weight. Beyond the stones, the appraiser must document the exact metal purity, such as 18k gold versus 14k, and the total gram weight. This level of precision ensures that if a loss occurs, the replacement value reflects the true market cost of the individual components. Precise documentation eliminates the ambiguity that often complicates high-value settlements; it provides a fixed benchmark that the insurer must respect. Understanding how does home insurance cover jewelry requires a shift from passive ownership to active, documented risk management.

Safe Storage and Loss Prevention

The way you protect your collection directly influences your standing with Florida insurance experts. Installing a UL-rated safe or a monitored home security system can lower premiums by 5% to 15% depending on the specific carrier and the total value of the scheduled items. You should strategically decide when to wear specific pieces and when to keep them in a bank vault. High-net-worth individuals often use a rotation strategy where only a small fraction of the collection is kept on-site at any given time. This proactive approach signals to underwriters that you're a disciplined risk; this often translates into more favorable terms and higher coverage limits. Security isn't just about preventing theft. It's about demonstrating a commitment to asset preservation that aligns with the expectations of elite insurance providers.

Properly documenting your assets is the first step toward absolute financial security. To ensure your collection is protected by a bespoke policy tailored to your lifestyle, consult with our strategic risk advisors at SI Insurance today.

Securing Your Legacy: Why SI Insurance is Your Strategic Guardian

Choosing the right protection for your high-value assets requires more than a simple transaction; it demands a partnership with a firm that prioritizes strategic alignment over retail convenience. SI Insurance operates through a white-glove independent agency model designed for those who require precision in their risk mitigation strategies. We recognize that standard, off-the-shelf policies rarely address the complexities of a significant jewelry collection. Our role is to act as your elite consultant, ensuring that your financial interests are shielded by underwriting excellence and sophisticated foresight.

Our methodology begins with a comprehensive risk audit of your existing homeowners policy. Most standard Florida policies include a sub-limit for jewelry theft that caps recovery at a mere $1,500 or $2,500 per incident. For a collection featuring heirloom timepieces or bespoke engagement rings, this creates a massive gap in your protection. We identify these vulnerabilities through rigorous analysis, moving beyond the surface-level coverage to evaluate how your policy responds to mysterious disappearance, accidental damage, or transit risks during international travel. By shifting from a reactive stance to one of proactive risk transfer, we ensure your legacy remains intact regardless of market volatility or unforeseen events.

Tailoring solutions for the Florida lifestyle means accounting for specific regional variables that national carriers often generalize. Whether you're spending the season in a waterfront estate or traveling between global residences, your coverage must be as mobile and resilient as you are. We don't believe in a one-size-fits-all approach. Instead, we engineer bespoke insurance structures that integrate seamlessly with your broader wealth management goals, providing a level of stability that retail agents simply cannot replicate.

Bespoke Coverage for Broward County Residents

Our approach centers on matching clients with specialized carriers that possess a deep understanding of the Florida property market. Many clients ask our team, does home insurance cover jewelry sufficiently in a high-risk hurricane zone? The answer depends entirely on the technical precision of your policy's language. We handle the heavy lifting of scheduling your valuables, a process that involves verifying appraisals and securing "all-risk" endorsements. This meticulous attention to detail provides the intellectual confidence you need, knowing that your most cherished assets are backed by a strategy built on technical mastery and local expertise.

Next Steps: Consultation and Strategy

Relying on a DIY approach to insurance often leads to expensive lessons during the claims process. We invite you to move toward a more disciplined framework by visiting our Sunrise or Pompano Beach offices for a professional policy review. Establishing a long-term partnership with a seasoned elite consultant at SI Insurance means you'll have a dedicated advocate who monitors the shifting landscape of Florida insurance on your behalf. Our commitment to meticulous service ensures that as your collection grows, your protection evolves in tandem. Schedule a strategic review of your home and jewelry coverage today.

Securing Your Collection for 2026 and Beyond

Understanding how your current policy handles high-value assets is the first step toward true financial security. While many Florida homeowners assume their standard HO-3 policy provides comprehensive coverage, the reality often involves a $1,500 sub-limit for theft and a restrictive list of named perils. Relying solely on the question, does home insurance cover jewelry, can leave significant gaps if you haven't accounted for mysterious disappearance or global transit. Our 2026 data shows that 85% of standard policies in Pompano Beach require specific scheduling to meet modern valuation standards. By integrating professional appraisals and choosing between scheduled personal property or standalone coverage, you're not just buying a policy; you're engineering a bespoke risk transfer.

SI Insurance offers direct access to top-tier carriers, ensuring your legacy is protected by more than just a basic contract. Our team in Sunrise leverages local market data to provide the underwriting excellence your collection deserves. Secure your high-value assets with a strategic policy review from SI Insurance. We're ready to help you navigate these complexities so you can enjoy your most precious items with total peace of mind.

Frequently Asked Questions

Is my engagement ring covered if I lose it outside of my home?

Your standard Florida homeowners policy typically won't cover an engagement ring lost at a beach in Sarasota or a restaurant in Miami unless you've specifically scheduled the item. While basic coverage protects against theft or fire, it excludes "mysterious disappearance" outside the residence. By adding a bespoke rider, you ensure the ring's protected worldwide against accidental loss. This strategic addition often costs about 1% to 2% of the ring's appraised value annually.

How much extra does it cost to add a jewelry rider to my Florida home insurance?

Adding a jewelry rider to your Florida home insurance typically costs between $1 and $2 for every $100 of the item's value. For a $15,000 diamond necklace, you'll likely pay an additional $150 to $300 per year in premiums. SI Insurance recommends this strategic alignment of coverage to avoid the $1,500 sub-limits found in standard ISO HO3 policies. These precise rates vary based on your specific Florida zip code and the security measures in your home.

Do I need a new appraisal every year for my jewelry insurance?

You don't need a new appraisal every 12 months, but most underwriters require an updated valuation every 2 to 3 years to maintain underwriting excellence. Gold prices fluctuated by over 10% in 2023, so outdated appraisals often lead to underinsurance. We suggest scheduling professional reviews on a 36 month cycle to ensure your bespoke risk transfer remains accurate. This process protects you from out-of-pocket losses if market values for precious metals or gemstones spike unexpectedly.

What is the difference between a sub-limit and a deductible for jewelry?

A sub-limit is the maximum dollar amount your policy pays for a specific category like jewelry, while a deductible is the initial cost you cover before insurance kicks in. Most standard Florida policies cap jewelry theft at $1,500 per claim. If you have a $1,000 deductible, you'd only receive $500 for a $5,000 watch. Strategic risk management involves scheduling items to remove these sub-limits and often reduces the deductible to $0 for those specific pieces.

Does home insurance cover jewelry stolen from a car in Florida?

Yes, your home insurance covers jewelry stolen from your vehicle in Florida, though the payout is restricted by your policy's "off-premises" limits. Standard plans often limit these claims to 10% of your personal property coverage or a flat $1,500 cap. Since Florida reported over 15,000 vehicle burglaries in recent quarterly data, relying on basic coverage is risky. A dedicated rider ensures the full $10,000 or $20,000 value of your pieces is recovered without the standard policy constraints.

Can I insure my jewelry if I am currently renting in Broward County?

You can certainly insure your jewelry if you're renting an apartment in Fort Lauderdale or Hollywood through a specialized renters insurance policy. Does home insurance cover jewelry for renters? Yes, but an HO4 policy carries the same $1,000 to $2,500 sub-limits as a standard homeowner's plan. Residents in Broward County should opt for scheduled personal property coverage to protect high-value assets against the region's specific risk profiles. This approach provides a strategic layer of security for your most prized possessions.

What happens if the value of my jewelry increases but my policy limit stays the same?

If the market value of your jewelry rises but your policy limit remains static, you'll be responsible for the financial gap during a total loss. In 2024, many luxury watch models saw secondary market increases of 15% or more. Without adjusting your coverage limits, your insurance payout won't cover the cost of a replacement at current retail prices. We recommend a strategic review of your schedule every two years to maintain absolute security and financial equilibrium.

Disclaimer

Disclaimer & Disclosure: Articles published on this website may be produced with the assistance of automated content generation tools and are reviewed periodically by our team. The content is provided for informational purposes only and does not constitute insurance advice, legal advice, or an offer of coverage. Insurance policies, coverage options, exclusions, and availability vary by carrier and state. For personalized guidance or policy recommendations, please contact a licensed insurance agent at our office.

Comments