Commercial Auto Insurance in Broward County: A Strategic Guide to Protecting Your Business Fleet (2026)

- siinsuranceflorida

- 6 days ago

- 13 min read

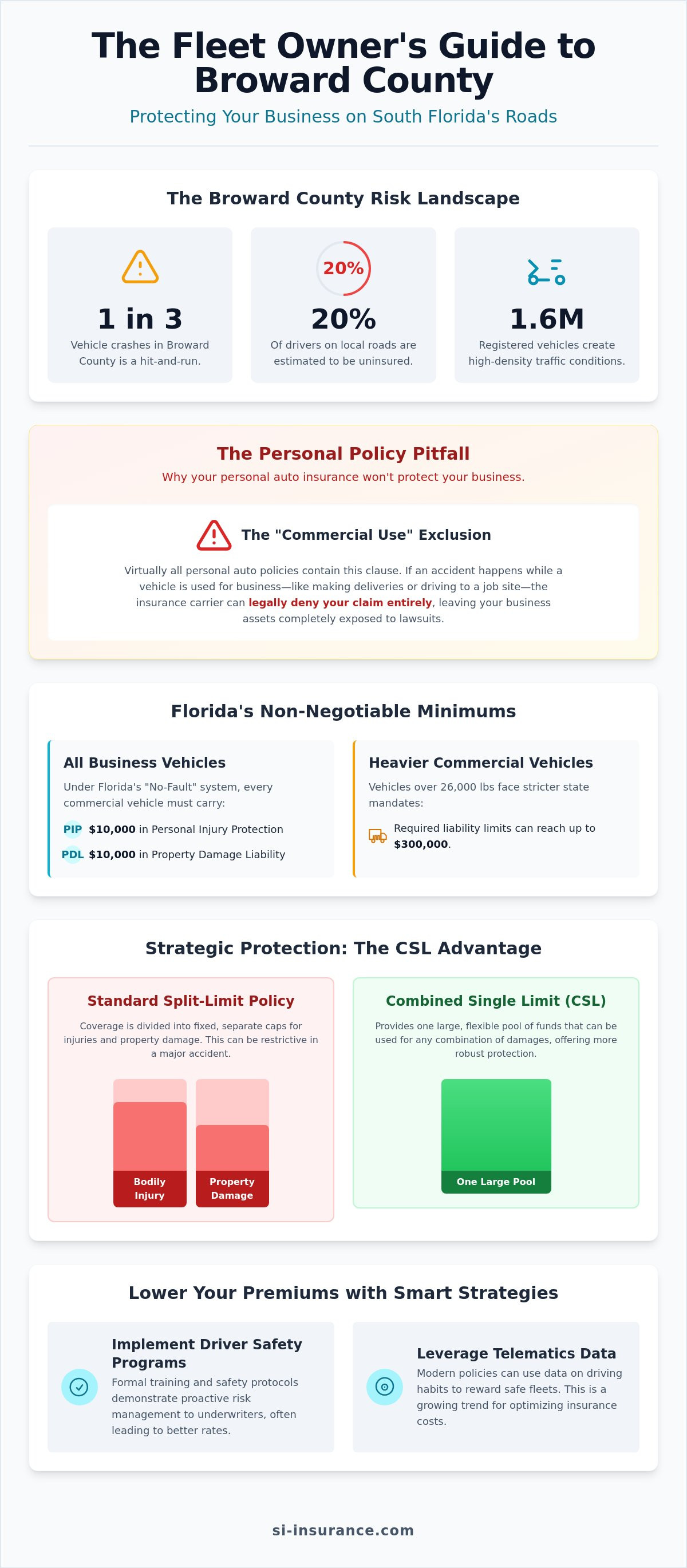

Did you know that roughly one in three vehicle crashes in Broward County is a hit-and-run, and an estimated 20% of drivers on our roads carry no insurance at all? It's a sobering reality for any business owner managing a fleet in South Florida. You likely feel the pressure of balancing rising operational costs with the need for absolute security against the unpredictable nature of local traffic and our seasonal hurricane risks. Finding the right commercial auto insurance Broward County requires more than just meeting the state's minimum PIP requirements; it demands a strategy that accounts for local volatility and the high density of our 1.6 million registered vehicles.

We understand that the boundary between personal and commercial liability can feel blurred, leaving you concerned about being underinsured during a major incident. This guide will show you how to navigate Florida's unique regulatory environment while optimizing your premiums and ensuring your company's assets remain shielded. We'll explore the specific coverage limits required for your vehicle weight class, the nuances of protecting employees who drive for your firm, and how to leverage the current downward trend in Florida's insurance rates to secure a more resilient financial future for your business.

Table of Contents

Beyond the Basics: Why Your Broward County Business Needs Dedicated Commercial Auto Coverage

Strategic Protection: Essential Coverage Components for Florida Commercial Fleets

Risk Mitigation and Optimization: How to Lower Your Business Insurance Expenses

Securing Your Livelihood: Why Si Insurance is Broward’s Choice for Commercial Protection

Beyond the Basics: Why Your Broward County Business Needs Dedicated Commercial Auto Coverage

Commercial auto insurance isn't merely an optional add-on; it's a specialized risk management contract designed to protect any vehicle utilized in business operations. For many entrepreneurs in Fort Lauderdale or Hollywood, the distinction between a personal commute and a business trip seems minor. However, insurance carriers view these activities through a completely different lens. While the average driver understands the basics of vehicle insurance, business owners must account for significantly higher liability exposure and more rigorous state requirements. Securing robust commercial auto insurance Broward County ensures that whether you’re a contractor in Sunrise or running a specialized delivery service in Pompano Beach, your company’s balance sheet remains protected. The stakes are high, and professional-grade protection is your best defense.

To better understand how these policies function in a real-world setting, watch this helpful breakdown:

The Personal Policy Pitfall: Why "Good Enough" Isn’t Enough

It's a common misconception that a personal auto policy provides a safety net for business-related driving. In reality, almost every personal policy in Florida contains a "Commercial Use" exclusion. This means that if an employee is involved in a collision while delivering a product or traveling between job sites, the carrier can legally deny the claim entirely. This usage gap represents the perilous distance between what your personal policy covers and what your business actually does. Beyond claim denials, a lawsuit directed at a business entity often seeks much higher damages than one against an individual. Without dedicated protection, a single incident could jeopardize the very existence of your company. Don't leave your livelihood to chance.

Legal Compliance in the State of Florida

Remaining compliant with the Florida Department of Highway Safety and Motor Vehicles (FLHSMV) is a non-negotiable aspect of operating a fleet. Despite various legislative discussions, Florida's "No-Fault" system remains the law of the land in 2026. This means every business vehicle must carry at least $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL). For heavier commercial motor vehicles over 26,000 lbs, Florida Statute 627.7415 mandates even higher liability limits, reaching up to $300,000 for the heaviest classes. Maintaining these standards isn't just about safety; it's about preserving your operational permits and business license. Partnering with a local consultant like SI Insurance ensures your commercial auto insurance Broward County stays ahead of these evolving regulatory benchmarks while providing the elite expertise your business deserves.

Strategic Protection: Essential Coverage Components for Florida Commercial Fleets

Building a resilient fleet protection strategy starts with moving beyond the restrictive nature of standard split-limit policies. For many sophisticated business owners, a Combined Single Limit (CSL) policy offers a more flexible and robust safeguard. Instead of having separate, fixed caps for bodily injury and property damage, a CSL policy provides one large pool of coverage that can be applied wherever it's needed most during a claim. This approach is particularly effective when ensuring your business exceeds Florida's minimum liability coverage, providing a higher level of financial certainty in the face of unpredictable litigation. When you're managing commercial auto insurance Broward County, these nuances in policy structure can mean the difference between a minor setback and a catastrophic loss.

One of the most critical, yet frequently overlooked, gaps in business coverage involves Hired and Non-Owned Auto (HNOA) protection. Many modern Broward firms rely on employees to run errands or attend meetings in their own personal vehicles. If an accident occurs during these business-related tasks, your company could be held liable for damages that exceed the employee's personal policy limits. HNOA coverage acts as a vital secondary shield, protecting your corporate assets from being targeted in a lawsuit. Given that nearly 20% of drivers in our region are uninsured, adding Uninsured/Underinsured Motorist (UM) coverage is equally essential. It ensures that your employees and vehicles are protected even when the at-fault party lacks the resources to pay for the damage they've caused.

Liability and Physical Damage: The Core Pillars

While liability coverage protects others, physical damage coverage preserves your own capital investments. In South Florida, "Comprehensive" coverage is your primary defense against non-collision events like flash flooding, hurricane debris, or theft. This is distinct from "Collision" coverage, which handles impact-related damage. For growing companies, an "Any Auto" designation can significantly simplify fleet management, as it automatically extends coverage to vehicles your business acquires, hires, or uses during the policy term without the administrative burden of scheduling every individual unit immediately.

Specialized Endorsements for Modern Businesses

Standard policies often fail to account for the valuable assets inside your vans or trucks. Inland Marine endorsements are necessary to protect tools, equipment, or specialized cargo while in transit between job sites. To maintain business continuity, we also recommend Roadside Assistance and Rental Reimbursement. These aren't just conveniences; they're strategic tools that keep your team moving and your revenue flowing even when a primary vehicle is sidelined for repairs. If you're ready to refine your current strategy, a quick review with the team at SI Insurance can help identify which of these specialized components best align with your operational goals.

Underwriting a fleet in South Florida involves a complex calculation of geographic and operational variables that go far beyond simple vehicle counts. While we've discussed the structural components of a policy, understanding the "why" behind your premium requires a look at the local landscape. The high traffic density on arteries like I-95, I-595, and the Florida Turnpike creates a volatile environment where collision frequency is statistically higher than in Florida's more rural counties. This "Broward Factor" is a primary driver of cost, as insurers must account for the increased probability of an incident in such a crowded transit corridor. Additionally, your specific industry—whether you're a local HVAC contractor or a heavy-hauling firm—drastically alters your risk profile. Heavier vehicles carry greater kinetic energy, and for those operating across state lines, Federal insurance requirements also come into play, adding another layer of complexity to the cost structure of commercial auto insurance Broward County.

In 2026, the industry has shifted toward data-driven pricing models that reward precision. Telematics systems, which monitor braking, speed, and cornering, allow underwriters to move away from generic industry averages. Instead, they offer rates based on the actual, objective performance of your drivers. This shift provides a unique opportunity for well-managed fleets to decouple their costs from the regional average and secure more favorable terms through proven safety metrics.

Local Risk Factors: From Fort Lauderdale Traffic to Hurricane Season

The environment itself is a persistent risk factor in our region. South Florida's hurricane season and frequent flash flooding necessitate robust Comprehensive coverage, which protects your assets from water damage and wind-blown debris. Beyond the weather, the high cost of litigation in our area directly inflates the "Liability" portion of your bill. Proximity to major logistical hubs like Port Everglades also introduces a higher concentration of heavy commercial traffic, which underwriters view as a high-exposure zone. These geographic realities mean that a business in Fort Lauderdale may face a different premium structure than one in a quieter part of the state.

The Role of Deductibles in Financial Strategy

A strategic deductible choice balances immediate cash flow with long-term risk. For cash-rich, established businesses, opting for a higher deductible can substantially lower monthly premiums, essentially self-insuring for minor incidents to preserve capital for growth. Startups or companies with tighter margins may prefer a lower deductible to ensure that a single accident doesn't create an unmanageable out-of-pocket expense. A strategic deductible choice balances immediate cash flow with long-term risk, ensuring your commercial auto insurance Broward County remains a sustainable part of your overhead. By aligning this choice with your company's liquidity, you create a more stable financial foundation.

Risk Mitigation and Optimization: How to Lower Your Business Insurance Expenses

Reducing the financial burden of commercial auto insurance Broward County requires a transition from reactive payments to proactive risk management. Underwriters in 2026 are increasingly focused on verifiable data rather than industry generalizations. By implementing a formal Driver Safety Program, you provide the documentary evidence necessary to justify lower risk classifications. This goes beyond simple rule-setting; it involves a cultural shift within your organization that prioritizes safety as a core business value. Combining these programs with regular vehicle maintenance audits ensures that mechanical failures don't lead to preventable accidents, which can be devastating for your loss history and future premiums.

Technology serves as a powerful ally in this optimization process. Utilizing dash cams and GPS tracking provides objective data that can be invaluable in the event of a claim. In a region where hit-and-run incidents are statistically prevalent, having video evidence can protect your business from fraudulent claims or unfair liability assignments. Many carriers also offer multi-policy discounts when you bundle your fleet coverage with a Business Owners Policy (BOP). This strategic bundling not only streamlines your administrative tasks but also leverages your total premium volume to secure more competitive rates across your entire insurance portfolio.

The Power of Professional Fleet Management

The fastest way to influence your premium is through meticulous personnel management. Hiring drivers with clean Motor Vehicle Reports (MVRs) is a fundamental prerequisite for a high-performing fleet. The long-term ROI of safety training and defensive driving courses often manifests in significantly lower insurance expenses over time. Consistent education reduces the frequency and severity of incidents, which is the primary metric underwriters use to calculate your renewal rates. At SI Insurance, we act as a specialized consultant to help audit your current safety protocols and identify areas where small adjustments could lead to substantial premium reductions.

Policy Review and Strategic Adjustments

Your fleet is dynamic, and your coverage should be too. Annual reviews are essential to ensure your protection levels align with the current size and market value of your vehicles. For instance, removing Collision coverage on older, fully depreciated units can be a sensible way to reduce costs without compromising your core liability protection. To understand how these decisions fit into your broader organizational goals, we recommend reading our Guide to Business Insurance in Broward County. If you're ready to optimize your current plan, reach out to a local expert at SI Insurance to begin a comprehensive review of your fleet’s risk profile.

Securing Your Livelihood: Why Si Insurance is Broward’s Choice for Commercial Protection

Selecting a partner for your commercial auto insurance Broward County is a decision that directly influences your company's long-term financial resilience. We've explored the volatility of South Florida's traffic, the nuances of Florida's legal requirements, and the technological shifts in 2026 premiums. These complexities require more than a generic policy; they demand a sophisticated risk management framework engineered by experts who understand the local landscape. At Si Insurance, we position ourselves as your dedicated consultants, moving beyond transactional sales to provide the calm, calculated guidance necessary to protect your fleet. We treat your business as a partner, ensuring that every asset, from a single delivery van to a large-scale transport fleet, is shielded by airtight logic and precision-crafted coverage.

Our status as an independent agency provides a distinct advantage in a market where the top five insurance groups are currently averaging an 8% rate decrease. Unlike captive agents who are limited to a single provider, we maintain relationships with a curated selection of elite carriers. This access allows us to compare diverse financial structures and specialized endorsements, ensuring your premium is optimized without sacrificing the integrity of your protection. We don't believe in one-size-fits-all solutions. Instead, we perform a rigorous analysis of your specific industry risks, whether you're managing the high-exposure needs of heavy hauling or the logistical intricacies of local service contracting.

The Si Insurance Advantage: Local Expertise, Global Standards

Our commitment to the Broward community is reflected in our active presence in Sunrise and Pompano Beach. This local footprint allows us to witness the same traffic patterns on I-595 and the Turnpike that your drivers face every day. We combine this local insight with global standards of professional excellence, acting as a protective guardian for your business interests. Our elite consultant persona isn't just about technical mastery; it's about providing a steady hand in a complex financial environment. To see how our methodology and carrier access stack up against the rest of the market, you can see how we compare to other Florida auto insurance companies in our detailed strategic comparison.

Next Steps: Initiating Your Strategic Coverage Review

Initiating a comprehensive review of your commercial auto insurance Broward County is a straightforward, meticulous process designed to respect your time while ensuring no detail is overlooked. We begin with a deep dive into your current fleet operations, driver safety records, and existing policy structures. From there, we identify hidden gaps, such as the Hired and Non-Owned Auto vulnerabilities discussed earlier, and present a refined strategy that aligns with your 2026 organizational goals. Our process is thorough and professional, providing you with the intellectual confidence that your livelihood is secure. When you're ready for a partner who values foresight and stability as much as you do, we invite you to request your personalized commercial auto insurance analysis from Si Insurance Agency and experience a higher standard of commercial protection.

Positioning Your Fleet for Long-Term Resilience

Success in our local market requires a shift from viewing insurance as a mandatory expense to treating it as a strategic asset. We've explored how moving beyond basic PIP requirements to include sophisticated tools like Hired and Non-Owned Auto coverage can bridge dangerous liability gaps. By embracing telematics and formal safety training, you don't just react to the high-density traffic of South Florida; you actively master it. Securing the right commercial auto insurance Broward County ensures that your business remains shielded from the unpredictable litigation and weather risks that define our region.

As an independent agency with deep roots in the South Florida market, Si Insurance Agency brings elite expertise and a personalized risk management approach to small and mid-sized businesses. We represent top-rated national carriers to provide you with a range of options that generic agencies simply can't match. It's time to move forward with a plan that is as meticulously engineered as your own operations. Protect your business assets with a tailored commercial auto policy from Si Insurance Agency. We look forward to helping you build a more secure and confident future for your fleet.

Frequently Asked Questions

Is commercial auto insurance required by law in Florida for all business vehicles?

Yes, any vehicle registered for business use in Florida must carry at least $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL). If your business operates heavier vehicles with a Gross Vehicle Weight Rating of 26,000 lbs or more, Florida Statute 627.7415 requires significantly higher liability limits. These legal benchmarks ensure you maintain your operational permits and protect the public in the event of an accident.

Can I use my personal vehicle for my Broward County business without a commercial policy?

Using a personal vehicle for business tasks is a significant risk because almost all personal policies in Florida contain a "Commercial Use" exclusion. If an accident occurs while you're delivering goods or traveling between job sites, your carrier will likely deny the claim entirely. This creates a dangerous gap that leaves your personal and business assets vulnerable to lawsuits. It's much safer to transition to a policy designed for commercial auto insurance Broward County to ensure continuous protection.

What is Hired and Non-Owned Auto (HNOA) insurance, and do I need it?

HNOA coverage protects your business when employees use their own personal vehicles or rented cars for company errands. If an employee causes an accident while driving for work, your business can be held liable for damages that exceed their personal policy limits. You definitely need this coverage if your team members ever use their own cars to visit clients, pick up supplies, or attend off-site meetings. It acts as a vital secondary shield for your corporate assets.

How much does commercial auto insurance typically cost in Broward County?

The cost of your premium depends on several variables, including the weight of your vehicles, the driving records of your employees, and your specific industry. In Broward County, rates are often influenced by high traffic density and the local litigation environment. While specific prices vary, businesses often find that implementing safety programs and using telematics can help secure more favorable terms. We recommend a personalized analysis to determine the most efficient structure for your budget.

Will my commercial auto policy cover my employees if they get into an accident?

Your policy will typically cover employees as long as they are listed as drivers on the policy and were operating the vehicle for business purposes at the time of the incident. If you utilize an "Any Auto" designation, coverage can even extend to newly hired staff or temporary drivers. It's essential to keep your driver list updated with your agent to ensure there are no surprises when you need to file a claim. Clear documentation is your best defense.

Does commercial auto insurance cover the tools and equipment inside my van?

Standard commercial auto policies generally do not cover the tools, equipment, or cargo inside the vehicle. To protect these high-value assets, you'll need to add an Inland Marine endorsement or a scheduled property floater to your plan. This ensures that if your specialized equipment is damaged in a collision or stolen from the van, you can recover the replacement costs. Without this specific addition, your primary policy only covers the vehicle itself.

How can I lower my commercial auto insurance premiums in South Florida?

The most effective way to reduce your commercial auto insurance Broward County expenses is by demonstrating a lower risk profile through data. Implementing a formal driver safety program and installing dash cams or GPS tracking provides underwriters with objective proof of safe operations. You can also lower costs by choosing a higher deductible if your business has the cash flow to handle minor out-of-pocket expenses. Bundling your auto coverage with a Business Owners Policy often triggers additional multi-policy discounts.

What happens if my business vehicle is damaged in a hurricane?

Damage from wind, flying debris, or flooding during a hurricane is covered under the "Comprehensive" portion of your policy. Since Broward County is a high-risk zone for tropical systems, maintaining this physical damage coverage is a critical part of a resilient risk management strategy. It's important to review your policy before the season starts to ensure your deductibles are manageable. This protection ensures that a major storm doesn't result in a permanent loss of your operational fleet.

Comments