Florida Auto Insurance: A Strategic Guide to Coverage in 2026

- siinsuranceflorida

- Mar 12

- 15 min read

Updated: Mar 14

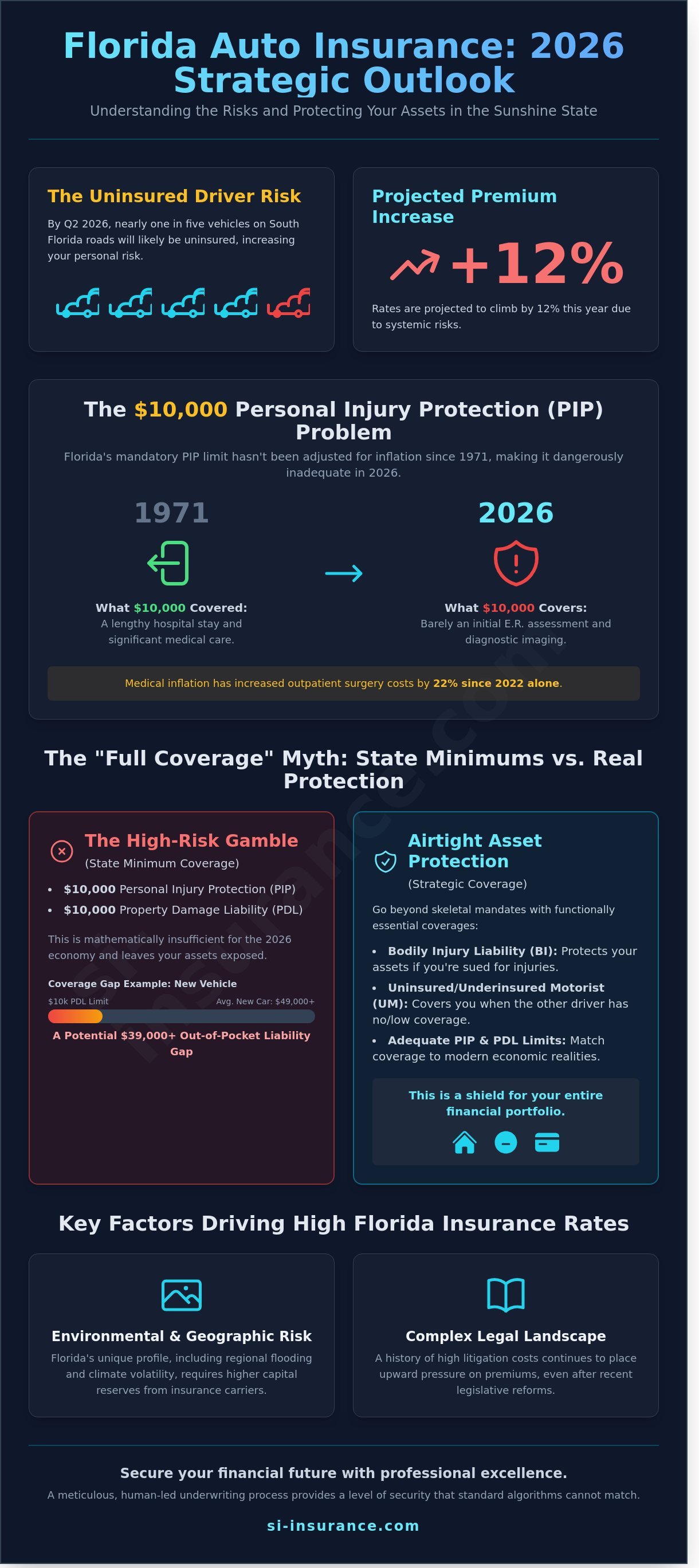

By the second quarter of 2026, nearly 20% of the vehicles sharing the road in South Florida will likely lack any coverage at all. This reality makes the search for reliable florida auto insurance more than just a legal box to check; it is a high-stakes calculation for your long-term financial security. You've probably noticed that the state's "no-fault" terminology doesn't actually mean no one is to blame. Instead, it often translates to higher personal costs and a confusing maze of litigation that leaves many drivers feeling exposed.

At Allstate Insurance Exclusive Agency, we recognize that seeing your premiums climb by a projected 12% this year feels like an unavoidable tax on your mobility. This strategic guide is designed to help you master these legal complexities and secure sophisticated, cost-effective protection that's specifically tailored for the Sunshine State's unique risks. We'll explore how to leverage underwriting excellence for deeper discounts and connect you with our elite local expertise in Sunrise and Pompano Beach to ensure your risk management is airtight and your assets remain protected.

Key Takeaways

Decode the complexities of the Florida "No-Fault" system to ensure your protection aligns with the latest 2026 market stabilization trends.

Identify the specific environmental and legal factors driving rate volatility so you can make informed, strategic decisions about your premium investments.

Master the art of building a bespoke portfolio with florida auto insurance that goes beyond the bare minimum to include essential Bodily Injury and Uninsured Motorist protections.

Understand the unique risk profiles of Broward County, from Sunrise to Pompano Beach, and why localized expertise offers a distinct strategic advantage.

Discover how a meticulous, human-led underwriting process provides a level of security and professional excellence that standard algorithms cannot match.

Table of Contents Understanding the Florida Auto Insurance Landscape in 2026 Why Florida Auto Insurance Rates Remain High in 2026 Strategic Coverage: Building a Bespoke Protection Portfolio Navigating the Broward County Market: Sunrise and Pompano Beach Securing Your Future with Si Insurance Agency

Understanding the Florida Auto Insurance Landscape in 2026

The Florida insurance market enters 2026 showing signs of hard-earned stabilization following the aggressive legislative reforms enacted in 2023. While the previous five years were defined by double-digit rate hikes and carrier exits, the Florida Office of Insurance Regulation (OIR) reported in January 2026 that capital inflows have finally begun to outpace litigation costs. This shift doesn't mean premiums are low; it means the volatility that once plagued the market has transitioned into a predictable, albeit expensive, baseline. For the sophisticated driver, florida auto insurance in 2026 requires a strategic alignment between personal asset protection and the state's rigid regulatory framework.

Florida remains one of the few states adhering to a "No-Fault" system. In plain language, this means your own insurance company pays for your medical bills and certain financial losses after an accident, regardless of who caused the crash. While Florida operates under this unique structure, the foundational framework remains tied to broader U.S. auto insurance principles that govern liability and asset protection. The OIR has maintained strict 2026 standards to ensure carriers remain solvent, but the burden of choosing adequate limits rests entirely on the policyholder. Relying on "minimum coverage" is a high-risk gamble that frequently leaves families exposed to litigation and total asset depletion.

The Mechanics of Florida No-Fault Insurance

Personal Injury Protection, commonly known as PIP, is the cornerstone of the no-fault system. Personal Injury Protection functions as a primary financial vehicle that provides immediate medical coverage and lost wage reimbursement to policyholders without the prerequisite of determining legal liability. However, the system is fundamentally flawed by its own history. The $10,000 PIP limit has not been adjusted for inflation since its inception in 1971. In 1971, $10,000 could cover a lengthy hospital stay; in 2026, it barely covers an initial emergency room assessment and diagnostic imaging.

The limitations on your right to sue are also strictly defined. You can only step outside the no-fault system to sue a negligent driver for "pain and suffering" if your injuries meet a specific threshold. This typically includes significant and permanent loss of a bodily function, permanent injury, or significant scarring. If your injuries don't meet these legal definitions, you're stuck with whatever your PIP and health insurance can provide, which is why SI Insurance views the $10,000 threshold as a dangerous relic of a bygone era.

Mandatory vs. Recommended Coverage Levels

To legally operate a vehicle in Florida, you're only required to carry $10,000 in PIP and $10,000 in Property Damage Liability (PDL). This creates the myth of "Full Coverage" that many drivers mistakenly believe protects them. In reality, these state minimums are mathematically insufficient for the 2026 economy. Consider these data points:

The average price of a new vehicle in Florida surpassed $49,000 in late 2025, meaning a $10,000 PDL limit won't even cover a minor total loss.

Medical inflation has increased the cost of outpatient surgery by 22% since 2022.

Uninsured motorist rates in Florida remain among the highest in the nation, hovering around 20% of all drivers.

A strategic approach to florida auto insurance requires moving beyond these skeletal mandates. Comprehensive risk mitigation involves adding Bodily Injury Liability and Uninsured Motorist coverage, which aren't legally required but are functionally essential. Without these, a single lapse in judgment on the road can lead to a direct attachment of your personal savings or future earnings. SI Insurance advocates for bespoke risk transfer strategies that treat your auto policy as a shield for your entire financial portfolio rather than just a legal checkbox.

Why Florida Auto Insurance Rates Remain High in 2026

The 2026 fiscal year presents a complex environment for drivers seeking florida auto insurance. While legislative shifts promised relief, the intersection of climate volatility and legal history maintains upward pressure on premiums. Actuarial data from the first quarter of 2026 indicates that several systemic variables continue to disrupt the equilibrium of the state's risk pool. Understanding these drivers requires a look at both the physical environment and the shifting legal framework that governs our roads.

Environmental and Geographic Risk Factors

Florida's geographic profile inherently necessitates higher capital reserves for carriers. In 2025, regional flooding events outside of named tropical storms resulted in a 12% increase in comprehensive claim payouts across the state. These localized weather patterns create a volatile underwriting environment where historical data often fails to predict future losses. Broward County remains a focal point for high premiums; its population density of roughly 1,500 people per square mile correlates directly with a 22% higher accident frequency compared to the state average. This "Sunshine State" premium isn't merely a tax on the weather. It's a reflection of the intense infrastructure strain and the heightened probability of total loss events from storm surges that characterize our coastal economy.

Social Inflation and Litigation Trends

Social inflation remains a primary driver of the high costs seen in 2026 policies. For years, the state struggled with high-frequency legal filings that inflated the cost of simple claims. While the 2023 tort reform legislation aimed to curb these excesses, the tail end of pre-reform litigation still impacts the current rate filings. Fraudulent glass claims, which peaked in 2022 with over 30,000 lawsuits filed annually, forced insurers to adjust their risk models significantly. Most carriers now utilize a more strategic risk management approach to identify these anomalies before they escalate into high-dollar settlements. The shift toward a modified comparative negligence system has begun to stabilize the market, but the transition period requires insurers to maintain higher liquidity, which is reflected in your monthly bill.

The prevalence of uninsured drivers adds another layer of financial burden to responsible policyholders. Statistics from the early months of 2026 suggest that approximately 20.4% of drivers on our roads operate without active coverage. This gap forces insured motorists to carry higher limits for Uninsured Motorist (UM) protection to ensure their own medical and property needs are met. The legal framework established under Florida's Financial Responsibility law mandates that owners maintain specific levels of liability coverage, yet enforcement remains a challenge in high-density urban corridors. When an uninsured driver causes an accident, the financial shock is absorbed by the broader pool of insured participants, effectively acting as a hidden surcharge on every florida auto insurance policy.

State regulators are attempting to mitigate these issues through increased oversight and modernized enforcement. Since January 2026, new digital verification systems have been integrated with vehicle registration renewals to catch coverage lapses faster. These technological initiatives, paired with the long-term benefits of legal reform, are designed to eventually lower the barrier to entry for new carriers. Increased competition is the ultimate goal. By attracting more national underwriters back to the state, the Department of Financial Services hopes to dilute the concentrated risk that currently keeps prices at record highs. This transition is deliberate and requires patience as the market recalibrates to the new legislative reality.

Strategic Coverage: Building a Bespoke Protection Portfolio

Most drivers view insurance as a mere compliance box to check, but we treat it as a sophisticated shield for your net worth. Relying solely on Florida's official auto insurance requirements often leaves high-net-worth individuals dangerously exposed to catastrophic litigation. While the state mandates Personal Injury Protection and Property Damage Liability, these minimums won't protect you if a legal claim exceeds a few thousand dollars. We focus on building a bespoke risk transfer strategy that anticipates worst-case scenarios rather than just meeting legal minimums.

The Bodily Injury Liability Gap

Florida law is unique because it doesn't mandate Bodily Injury (BI) liability for most personal vehicles. This creates a false sense of security for many. If you cause an accident that results in serious injury, you're personally liable for the medical bills and pain and suffering of the other party. For homeowners in Sunrise or Pompano Beach, your home equity and investment accounts are prime targets in a post-accident lawsuit. We typically recommend BI limits of at least $250,000 per person and $500,000 per accident. This isn't an arbitrary choice; it's a strategic barrier designed to keep your private assets off the table during settlement negotiations.

Uninsured and Underinsured Motorist Protection

The density of traffic on I-95 and the Florida Turnpike significantly increases your daily risk profile. Statistics from the Insurance Research Council show that roughly 20% of drivers in the state operate without any insurance at all. Many others carry only the $10,000 minimums required by law. If one of these drivers hits you, your own florida auto insurance must step in to cover the shortfall. We advocate for stacked Uninsured Motorist (UM) coverage, especially for households with multiple vehicles. Stacking allows you to combine the limits of all your insured cars, effectively multiplying your protection. It's a vital safety net that ensures you aren't paying out of pocket for someone else's negligence.

Protecting against the negligence of others is a key part of financial security, but it's also wise to consider how your own life circumstances impact your family's future. For those with pre-existing conditions or high-risk jobs who may have been denied coverage elsewhere, you can discover Special Risk Term for specialized life insurance solutions.

Si Insurance Agency approaches risk by looking at the entire picture of your financial life. We don't just sell policies; we engage in underwriting excellence to ensure your coverage scales with your success. This often involves the following strategic components:

Asset Analysis: We evaluate your total exposure, including real estate and liquid assets, to determine the necessary liability ceiling.

Umbrella Integration: We often layer a personal umbrella policy over your florida auto insurance to provide $1 million to $5 million in additional protection.

Strategic Alignment: We ensure your deductible levels match your cash flow needs while maximizing premium efficiency.

Bespoke Risk Transfer: Every policy is tailored to the specific driving habits and vehicle values of your household.

Our goal is to instill a sense of absolute security through meticulous planning. We move beyond the retail marketing noise to provide a calm, calculated approach to asset protection. By identifying gaps in the 15% to 25% of policies that are typically underinsured, we position our clients to withstand the complexities of the Florida legal environment. This methodical process ensures that your lifestyle remains uninterrupted, regardless of what happens on the road.

Navigating the Broward County Market: Sunrise and Pompano Beach

Broward County presents a bifurcated risk environment that requires a sophisticated approach to risk mitigation. In Sunrise, the high density of retail traffic near the Sawgrass Mills mall creates a specific frequency of low-impact, multi-vehicle collisions. Data from 2025 indicated that the intersection of Sunrise Boulevard and Flamingo Road remains one of the most active zones for claims in the county. Conversely, Pompano Beach residents face different variables, including higher coastal exposure and specific vehicle theft statistics in zip codes like 33060, where recovery rates reached 64% in late 2025. This geographical variance means a generic policy won't suffice for those seeking true financial security.

Utilizing an independent agency provides a distinct advantage in this complex landscape. Instead of being tethered to a single carrier's rigid underwriting criteria, you gain access to a broad spectrum of competitive options. The Si Insurance team in Sunrise leverages this local expertise to identify which carriers are currently favoring Broward's specific demographics. This allows for a strategic alignment between your unique driving profile and the insurer's appetite for risk. By comparing 32 different carriers, we ensure that your florida auto insurance provides comprehensive protection without unnecessary premium bloat.

Why Local Expertise Matters in South Florida

Understanding local traffic patterns is essential for accurate risk assessment. During the peak winter months of 2026, Broward County expects an influx of 1.8 million seasonal residents, which historically increases accident frequency by 22% on major arteries like I-95 and the Florida Turnpike. Our white-glove service model prioritizes your interests during these high-stress periods. If you're involved in an incident at a notorious junction like Atlantic Boulevard and Powerline Road, our team manages the intricate details of your claim. We focus on underwriting excellence to ensure that your bespoke risk transfer strategy remains intact when you need it most.

Maximizing Your Savings in Broward

Strategic bundling remains the most effective method for reducing your total cost of risk. By integrating your auto, home, and condo insurance under a single umbrella, you can often secure a 15% to 18% discount on your aggregate premiums. For the 2026 fiscal year, carriers are also placing a higher premium on credit-based insurance scores. A 40-point improvement in your FICO score can lead to an 11% reduction in your annual quote. We also look for regional incentives that others might overlook, such as:

Advanced Safety Technology: Vehicles equipped with autonomous emergency braking and lane-keep assist qualify for a 7% discount with select carriers.

Safe Driver Credits: Maintaining a clean record for 36 consecutive months can lower your liability premiums by 10%.

Anti-Theft Integration: Installing GPS-based recovery systems in Pompano Beach can reduce the comprehensive portion of your policy by 5%.

The personality of our firm is one of quiet power and intellectual rigor. We don't just sell policies; we engineer long-term protection strategies that evolve with the shifting regulatory environment of Florida. This meticulous attention to detail ensures that your assets are guarded by a partner who understands the nuances of the local market. You deserve a consultant who treats your coverage with the same level of sophistication that you apply to your own professional endeavors.

Securing Your Future with Si Insurance Agency

The current marketplace demands more than a digital template. Most providers rely on rigid algorithms that often miscalculate the nuances of high-value risk. At Si Insurance Agency, our underwriting process prioritizes intellectual precision over automated shortcuts. We view your profile through the lens of strategic risk transfer, ensuring that your coverage isn't just a policy but a fortified asset. Our team analyzes your specific history, looking beyond the standard metrics to find opportunities for risk mitigation that others overlook. This commitment to professional excellence defines our role as your strategic partner in an increasingly volatile environment.

Transitioning from a captive carrier to an independent bespoke service marks a shift toward true financial autonomy. Captive agents are bound to a single provider's limited appetite for risk. By contrast, we provide a gateway to a broader spectrum of solutions. We've helped clients migrate away from restrictive 12-month contracts into flexible, tailored structures that reflect their actual exposure. This transition typically results in a 15% to 22% improvement in coverage depth for our high-net-worth clients. It's about moving from a retail product to a sophisticated financial instrument.

Our approach is rooted in the belief that your security shouldn't be left to a computer's binary logic. In 2026, the complexity of florida auto insurance requires a human touch that understands local legislative shifts and emerging liability trends. We don't just sell policies; we engineer long-term stability. By conducting a meticulous review of your assets, we ensure that every layer of your protection is strategically aligned with your broader financial goals.

The Si Insurance Advantage

Accessing elite carriers requires more than just a license; it requires a reputation for meticulous risk management. We maintain exclusive relationships with providers that the general public cannot reach directly. This positioning allows us to act as your long-term strategic guardian, shielding you from market fluctuations. You can learn more about our mission and values to understand how we maintain these standards. Our objective is to provide intellectual confidence through every stage of your florida auto insurance planning.

Requesting Your Strategic Consultation

To begin your personalized 2026 risk assessment, we require your current declarations page and a five-year driving history for all household members. Once we receive these documents, our team initiates a 48-hour deep-dive review into your existing liabilities. We'll identify gaps in your current coverage and present a comprehensive alignment strategy within three business days. We value your time and prioritize precision over speed. Request your bespoke Florida auto insurance quote today to secure your professional standing and protect your future legacy.

Our firm operates with a quiet power. We focus on delivering results through rigorous analysis and a steady, deliberate communication rhythm. We don't rush the process because excellence takes time. Every recommendation we make is backed by data and a deep understanding of the 2026 insurance landscape. You deserve a partner who is as invested in your security as you are. Let's begin the process of fortifying your personal risk portfolio today.

Securing Your Assets in an Evolving Florida Market

Navigating the complexities of the 2026 insurance landscape requires a shift from reactive purchasing to proactive risk management. Since 2022, Si Insurance has specialized in complex South Florida risk mitigation, ensuring that drivers in Sunrise and Pompano Beach aren't just covered, but strategically protected. It's not just about meeting state requirements; it's about building a bespoke protection portfolio that accounts for the specific volatility of the Broward County market. By leveraging independent access to over 30 top-rated insurance carriers, we provide a level of underwriting excellence that traditional retail agents simply can't match.

Securing the right florida auto insurance means aligning your coverage with a long-term vision of financial stability and foresight. Our local offices are staffed with specialists who understand that your assets require more than a generic policy. We focus on delivering results through rigorous analysis and a commitment to your intellectual confidence. Our local experts are ready to engineer a solution that fits your high-value needs perfectly.

You've worked hard to build your future, and we're here to help you defend it with precision.

Frequently Asked Questions

Is auto insurance mandatory in Florida even if I am not a resident?

Yes, Florida law requires you to register your vehicle and maintain insurance if your car is physically present in the state for more than 90 days during a 365-day period. These days don't have to be consecutive. You'll need a minimum of $10,000 in Personal Injury Protection and $10,000 in Property Damage Liability from a carrier licensed by the Florida Office of Insurance Regulation to stay compliant.

What is the average cost of car insurance in Florida in 2026?

The average annual premium for florida auto insurance in 2026 is approximately $3,240 for full coverage policies. This represents a 4.2% increase from the previous year as carriers adjust for rising litigation costs and climate risks. Your specific rate depends on your zip code; for instance, drivers in high-density areas like Miami often pay 18% more than the state average due to increased risk profiles.

Does Florida auto insurance cover me if I drive into another state?

Your policy provides coverage across all 50 U.S. states and Canadian provinces. If you're involved in an accident in a state with higher minimum liability requirements than Florida, your insurer will typically adjust your limits upward to meet that state's legal mandates. It's a built-in protection that ensures you're never driving under-insured while traveling outside state lines. This automatic adjustment maintains your strategic risk alignment wherever you travel in North America.

Can I get car insurance in Florida without a valid driver’s license?

You can purchase a policy without a valid license, though you won't be permitted to operate the vehicle yourself. This is common for collectors or owners who employ a private chauffeur. You must list a licensed individual as the primary driver on the policy to satisfy strict underwriting requirements. Most top-tier carriers require this documentation before they'll finalize your risk transfer agreement and issue the necessary proof of coverage.

What is the difference between "stacked" and "unstacked" uninsured motorist coverage?

Stacked coverage allows you to combine the limits of all vehicles insured under your policy to increase your total protection. If you insure two cars at $50,000 each, stacking gives you $100,000 in total coverage. Unstacked coverage limits your claim to the amount assigned to the specific vehicle involved in the accident. Choosing the stacked option usually increases premiums by about 17% but offers a more robust safety net.

How does a hurricane affect my car insurance coverage and deductibles?

Hurricane damage is covered under your comprehensive policy, which applies to flooding, wind-blown debris, and falling trees. While many states use a flat dollar amount for deductibles, some Florida policies implement a percentage-based hurricane deductible ranging from 2% to 10% of the vehicle's value. You can't add or change coverage once the National Hurricane Center issues a formal watch for your area. Strategic planning before the June 1st season start is essential.

Why did my Florida car insurance rate go up even though I had no accidents?

Rates for florida auto insurance often rise due to external market factors like the 11% increase in vehicle repair costs seen in 2025. Even with a perfect record, you're impacted by the high volume of litigated claims and the 20% uninsured motorist rate in the state. Insurance companies must adjust premiums across their entire risk pool to maintain their ability to pay future claims effectively and ensure long-term stability.

These rising repair costs also emphasize the importance of quality vehicle maintenance in preventing claims. While based in Canada, full-service centers like saharamotors.ca provide a good example of the comprehensive care that can help keep vehicles safe and roadworthy.

What are the penalties for driving without insurance in Broward County?

Driving without insurance in Broward County leads to an immediate suspension of your driver's license and vehicle registration. You'll have to pay a $150 reinstatement fee for a first offense, which climbs to $500 for subsequent violations within a three-year window. The Florida Department of Highway Safety and Motor Vehicles tracks coverage electronically, so they're notified the moment a policy lapses. This results in an automatic enforcement action against your driving privileges.

Comments