Florida No-Fault Insurance Explained: A Strategic Guide for 2026

- siinsuranceflorida

- Apr 24

- 12 min read

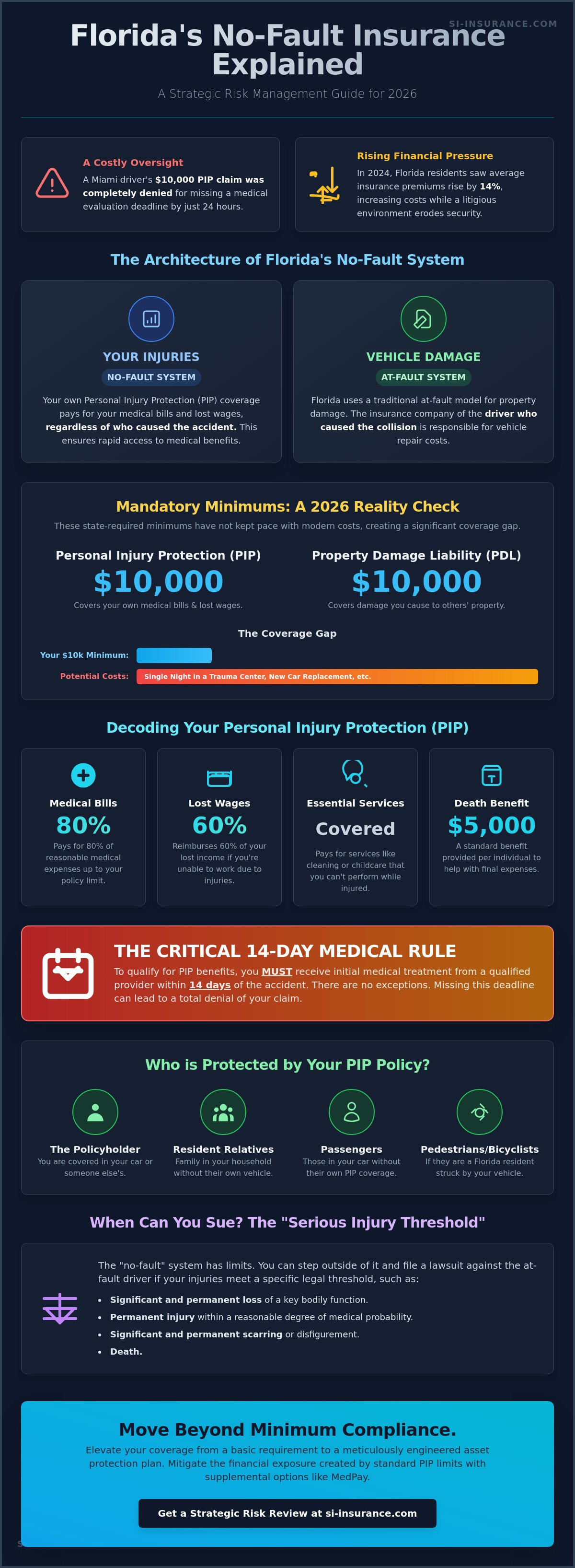

On a Tuesday in October 2023, a driver in Miami discovered that missing a medical evaluation by just twenty four hours resulted in a total denial of their $10,000 Personal Injury Protection claim. It's a sobering example of how easily a lack of technical clarity can lead to significant financial exposure. Having Florida no-fault insurance explained through a lens of strategic risk management is essential for navigating the state's unique legal landscape in 2026. You likely share the frustration of many residents who saw average premiums rise by 14% in 2024; it's exhausting to pay more while feeling less secure in a litigious environment.

We'll help you master these complexities so you can strategically engineer your coverage for maximum protection and intellectual confidence. You'll learn to distinguish between PIP and Liability and how to select policy limits that actually safeguard your personal assets. This guide clarifies the mandatory 14-day medical rule and defines the specific legal thresholds required to pursue a claim against another driver.

Key Takeaways

This guide provides Florida no-fault insurance explained through a lens of strategic risk management, ensuring you understand how your policy serves as an immediate financial safeguard regardless of liability.

Master the mechanics of Personal Injury Protection (PIP) to effectively manage the 80/60 reimbursement structure for medical bills and lost wages during a recovery period.

Uncover the specific legal conditions of the "Serious Injury Threshold" that allow you to step outside the no-fault system and pursue traditional litigation when circumstances demand it.

Evaluate the necessity of supplemental options like Medical Payments (MedPay) to mitigate the financial exposure created by standard PIP limits in the modern Florida landscape.

Learn how a tailored, consultative approach to risk management can elevate your coverage from basic legal compliance to a meticulously engineered asset protection plan.

Table of Contents The Architecture of Florida’s No-Fault Insurance System Personal Injury Protection (PIP): The Core Mechanism Debunking Misconceptions: When Can You Sue in Florida? Strategic Risk Mitigation: Beyond the Legal Minimums Navigating the Florida Landscape with Si Insurance Agency

The Architecture of Florida’s No-Fault Insurance System

Florida's regulatory framework for motor vehicle coverage operates on a principle of immediate financial stabilization. Under a no-fault insurance system, your own insurance carrier assumes responsibility for your medical expenses and lost wages after an accident, regardless of who caused the collision. This structure wasn't designed by accident. The Florida Legislature established this mandate to decrease the overwhelming volume of small-claims litigation in state courts while ensuring that injured parties receive medical payouts without waiting for a lengthy liability investigation. While the term might suggest total immunity from blame, this Florida no-fault insurance explained guide clarifies that the "no-fault" designation applies strictly to bodily injuries. For vehicle damage, Florida still adheres to a traditional at-fault model where the negligent party's insurer pays for repairs.

For those seeking underwriting excellence, SI Insurance views these mandates as the bare foundation of a sophisticated risk management plan. The system functions as a trade-off; drivers give up some rights to sue for minor injuries in exchange for guaranteed, rapid access to medical benefits. This strategic alignment between policyholders and carriers helps maintain a level of predictability in the state's volatile insurance market.

The Mandatory Minimums for Florida Drivers

Florida law requires every driver to carry two specific types of coverage through the Florida Highway Safety and Motor Vehicles (FLHSMV) department. These include $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL). These minimum requirements haven't changed since their inception, even as medical costs and vehicle repair technologies have advanced significantly by 2026. This stagnation creates a strategic gap for many drivers, as $10,000 often fails to cover a single night in a modern trauma center or a total loss on a late-model electric vehicle.

Who is Covered Under Your No-Fault Policy?

The protective reach of a PIP policy is broader than many realize. It acts as a shield for several groups involved in a transit incident. Understanding who falls under this umbrella is a core part of having Florida no-fault insurance explained for a comprehensive risk management strategy. Coverage generally includes:

The Policyholder: Coverage applies whether you're in your own vehicle or someone else's car.

Resident Relatives: Family members living in your household who don't own their own vehicle.

Passengers: Individuals in your car who don't have their own PIP coverage.

Pedestrians and Bicyclists: Florida residents struck by your vehicle are often covered by your PIP.

Geographical boundaries matter. PIP typically follows the driver throughout Florida, but coverage often vanishes for non-resident passengers if an accident occurs outside state lines. This limitation requires careful foresight when planning interstate travel or managing corporate fleets.

Personal Injury Protection (PIP): The Core Mechanism

Understanding the internal architecture of Personal Injury Protection is the first step toward effective risk management. Under the current framework of Florida no-fault insurance explained for modern policyholders, PIP acts as your immediate financial buffer. This coverage adheres to a specific 80/60 calculation; it systematically pays 80% of your reasonable medical expenses and 60% of lost income resulting from accident-related injuries. For those managing complex professional lives, this 60% wage reimbursement provides a necessary, though partial, safety net during the recovery period.

Standard policies also integrate a $5,000 death benefit per individual, which serves as a strategic resource for funeral and burial costs. Beyond direct medical costs, PIP provides for "Essential Services." This component covers the costs of hiring help for household responsibilities, such as cleaning or childcare, that you're unable to perform due to your injuries. When selecting a policy, you'll choose a deductible, often ranging from $250 to $1,000. Selecting a higher deductible reduces your monthly premium but increases your immediate financial exposure after an incident.

The Critical 14-Day Medical Treatment Rule

Timing is a non-negotiable variable in the PIP claims process. You must seek medical attention within 14 days of the accident to preserve your eligibility for benefits. The extent of your coverage depends heavily on the initial diagnosis. If a physician identifies an Emergency Medical Condition (EMC), you can access your full $10,000 limit. However, if the injury doesn't meet the EMC threshold, your benefit is capped at $2,500. This distinction is vital for long-term health and financial stability, as outlined in recent legislative reviews like the Florida Senate Bill Analysis.

Navigating the Claims Process for Medical Benefits

The administrative burden of medical billing is largely shifted away from the policyholder. Medical providers typically bill your PIP carrier directly, streamlining the recovery phase. It's essential to recognize that PIP functions as the primary payer in Florida auto accidents, preceding health insurance coverage. Only after your PIP limits are exhausted or the 20% co-insurance is applied does your private health insurance begin to contribute. For executives looking to refine their personal risk profiles, ensuring strategic alignment between these two layers of coverage is a prudent move.

Debunking Misconceptions: When Can You Sue in Florida?

The term "no-fault" frequently creates a false sense of security for many drivers. There's a common belief that because your own policy pays for your initial medical bills, you're immune from being sued or held liable for an accident. This isn't the case. While Florida no-fault insurance explained emphasizes immediate access to medical care through Personal Injury Protection (PIP), it doesn't offer a total shield against legal responsibility. When looking at Florida no-fault insurance explained through a legal lens, the system is designed to reduce small claims, not to eliminate liability for major accidents. If you're at fault in a collision that results in serious harm, the legal barriers protecting you can be breached, leaving your personal assets exposed to significant litigation.

Understanding the Serious Injury Threshold

To step outside the no-fault system and file a claim against an at-fault driver for pain and suffering, a victim must meet the "serious injury threshold." Florida law defines this through specific legal criteria. A victim must demonstrate a significant and permanent loss of a bodily function, a permanent injury within a reasonable degree of medical probability, or significant and permanent scarring. When these conditions are met, the limitations of PIP are removed, allowing the injured party to seek full compensation for non-economic damages.

This threshold is the primary reason why Bodily Injury Liability (BI) coverage is a strategic necessity for high-net-worth individuals and careful planners. Even though Florida law doesn't mandate BI for every driver, the absence of this coverage can be catastrophic. Analyzing recent Florida crash data shows that severe accidents happen daily; without BI, you're personally responsible for every dollar of a victim's medical costs and suffering once the threshold is crossed.

Property Damage and the At-Fault Reality

Remember that the no-fault rule only applies to bodily injuries. Property damage is always handled on an at-fault basis in Florida. If you're responsible for an accident, your Property Damage Liability (PDL) coverage pays for the repairs to the other driver's vehicle. However, PDL does nothing for your own car. To protect your own investment, you must carry Collision coverage. This becomes especially important if you're involved in an incident with an uninsured driver or if you're found to be the primary cause of the crash.

Strategic risk management involves looking beyond the basic legal requirements to ensure comprehensive protection. You can learn more about balancing these various mandates in our detailed review of Florida Auto Insurance: A Strategic Guide to Coverage in 2026. Understanding these distinctions ensures that a minor lapse in judgment doesn't turn into a permanent financial setback.

Strategic Risk Mitigation: Beyond the Legal Minimums

Relying on the state-mandated minimums is a precarious position for any Florida driver. While the law requires $10,000 in Personal Injury Protection (PIP), this figure is functionally obsolete in 2026. With medical inflation rates hovering around 4.5% annually over the last decade, a standard emergency room visit following a collision can exhaust a $10,000 limit in hours. When Florida no-fault insurance explained through the lens of modern costs, it's clear that the minimum coverage acts as a temporary bandage rather than a robust financial shield.

Strategic drivers utilize Medical Payments (MedPay) to close the inherent 20% gap left by PIP. Since PIP only covers 80% of your medical expenses, MedPay steps in to cover the remaining portion and your deductible. This ensures that a $5,000 hospital bill doesn't result in a $1,000 out-of-pocket expense for you. Beyond medical bills, Bodily Injury (BI) coverage is the most critical tool for asset protection. Florida doesn't require BI for most drivers, but without it, your personal savings, home equity, and future earnings are vulnerable to lawsuits if you're found liable for another person's injuries.

Layering Coverage for Comprehensive Security

A "Strategically Engineered Policy" focuses on total risk transfer rather than just checking a legal box. In South Florida, specifically Broward and Miami-Dade counties, the risk of encountering an uninsured driver remains high. Current data from the Insurance Research Council suggests that approximately 20% of Florida drivers lack active insurance. Uninsured Motorist (UM) coverage is your only protection in these scenarios, providing funds for your medical needs and lost wages when the at-fault party has no assets to seize.

For high-net-worth individuals, an Umbrella policy provides a final layer of defense. It sits above your primary auto and homeowners' limits, offering a massive buffer against catastrophic claims. This is essential in a litigious environment where personal injury settlements frequently exceed standard policy limits.

The Interaction with Health Insurance and Medicare

Your PIP coverage acts as a "deductible eater" for your primary health insurance. In the event of an accident, PIP pays out first, which can help you meet your health insurance plan's annual out-of-pocket maximum without dipping into your savings. However, the interaction isn't always seamless. You must account for subrogation, a process where your health insurer or Medicare seeks reimbursement from any legal settlement you win. Managing these overlapping layers requires a sophisticated understanding of how Florida no-fault insurance explained in a legal context affects your total recovery.

To ensure your auto coverage aligns with your property protection, you should learn how to bundle home and auto insurance in Florida to maximize your credits and simplify your risk management strategy.

Don't leave your personal wealth to chance; contact our specialists to audit your current policy limits and build a bespoke protection plan.

Navigating the Florida Landscape with Si Insurance Agency

Si Insurance Agency operates as a sophisticated partner for those seeking clarity in a volatile market. Having Florida no-fault insurance explained by a local specialist ensures you aren't just buying a document, but securing a calculated defense against risk. Our roots in Broward County, specifically in Sunrise and Pompano Beach, allow us to offer a white-glove service that generic national carriers simply can't match. We treat insurance as a bespoke risk transfer mechanism, aligning your coverage with the specific realities of the Florida roads.

Local Expertise in Sunrise and Pompano Beach

The traffic patterns in Sunrise and Pompano Beach present distinct variables for every driver. With Broward County experiencing high density, the risk of a Personal Injury Protection (PIP) claim is statistically significant. In 2023, the Florida Department of Highway Safety and Motor Vehicles reported over 41,000 crashes in Broward County alone. This high volume makes local knowledge essential for quick recovery. While we focus on Broward, our insights extend to traffic risks across all cities in the State of Florida, where rising litigation rates and repair costs have shifted the insurance environment. Our team monitors these regional trends and the local legal landscape to provide stable, long-term protection. We've built relationships with trusted repair facilities and understand the specific underwriting requirements that keep Florida families secure.

Securing Your Quote with Si Insurance Agency

Obtaining a quote through si-insurance.com is the first step toward institutional-grade protection. We move beyond the limitations of automated online forms by providing a personalized consultation. This process involves a rigorous analysis of your financial exposure to ensure your policy acts as a strategic guardian for your future. We don't offer off-the-shelf products; instead, we engineer solutions that meet high-value needs through elite expertise. Our goal is to instill intellectual confidence in every client we serve. We act as a calm and calculated partner, ensuring that your transition into a new policy is seamless and professionally managed.

The complexity of Florida's insurance market requires more than just a policy. It requires a seasoned, elite consultant who acts as your strategic guardian. If you're ready to move away from generic retail marketing and toward a partnership focused on foresight and stability, our team is prepared to assist. Contact us today for a bespoke risk assessment that prioritizes your financial stability and long-term security.

Securing Your Financial Architecture for 2026

Navigating the complexities of the Sunshine State's roads requires more than just basic compliance. Understanding how Florida no-fault insurance explained in this guide functions is the first step toward true financial immunity. Since we founded our independent agency in 2022, we've focused on the unique risk profiles found throughout Broward County. We ensure that high-value assets remain shielded from the volatility of modern litigation. While the state mandates a $10,000 PIP minimum, these figures rarely suffice for families with significant wealth to protect. It's vital to look past the statutory requirements; you need to align your coverage with a bespoke risk transfer strategy that anticipates the legal shifts of 2026. Our team provides the intellectual foresight needed to manage these intricate liabilities with precision. You shouldn't leave your legacy to chance when professional underwriting excellence is within reach.

Take the proactive step today to ensure your peace of mind remains absolute as you navigate the road ahead.

Frequently Asked Questions

Is Florida still a no-fault state in 2026?

Yes, Florida maintains its status as a no-fault jurisdiction through the 2026 calendar year. This specific system requires every driver to carry Personal Injury Protection (PIP) to cover their own initial medical expenses regardless of who caused the collision. While the 2021 legislative session saw a veto of Senate Bill 54, which aimed to repeal this system, the current statutes remain the primary framework for local risk mitigation.

What happens if medical bills exceed the $10,000 PIP limit?

Once your medical expenses surpass the $10,000 PIP threshold, you're responsible for the remaining balance through health insurance or personal funds. If your injuries meet the permanent injury threshold defined in Florida Statute 627.737, you can pursue a strategic claim against the at-fault driver's Bodily Injury Liability coverage. This secondary layer of recovery is vital for managing high-value medical liabilities that exceed basic statutory requirements.

Does no-fault insurance cover my car repairs if I am not at fault?

No-fault insurance doesn't apply to vehicle repairs because it's strictly designed for medical costs and lost wages. In a scenario where you're not at fault, you'll seek recovery through the other driver's Property Damage Liability (PDL) coverage or your own collision policy. Understanding how Florida no-fault insurance explained in this context distinguishes between personal injury and tangible asset protection is key for any strategic recovery plan.

Can I be sued in Florida if I have no-fault insurance?

You can still face a lawsuit in Florida if the other party's injuries are classified as permanent or result in significant scarring or loss of bodily function. While PIP provides a limited immunity for minor claims, it doesn't offer absolute protection against high-stakes litigation. We recommend maintaining robust Bodily Injury Liability limits, such as $100,000 per person, to safeguard your personal assets from these specific legal vulnerabilities.

What is the 14-day rule for Florida car accidents?

The 14-day rule requires you to seek initial medical treatment within exactly 14 days of the accident to qualify for PIP benefits. If you miss this window, your insurer will likely deny the claim entirely. Additionally, a physician must determine you have an Emergency Medical Condition (EMC) for you to access the full $10,000 limit. Without an EMC diagnosis, your medical benefit is capped at $2,500.

Do I need Bodily Injury Liability if Florida is a no-fault state?

Florida law doesn't mandate Bodily Injury (BI) Liability for most private passenger vehicles, but it's strategically essential for risk management. Without BI coverage, you're personally liable for the other party's medical bills and pain and suffering if you cause a serious accident. Carrying at least $100,000 per person in BI coverage is a standard recommendation for protecting your long-term financial stability against unpredictable legal challenges.

How does PIP work if I am a passenger in someone else’s car?

If you're a passenger, your own Florida PIP policy acts as the primary coverage for your medical needs. If you don't own a vehicle or have a policy, you'll typically be covered by the PIP policy of a relative you live with. If neither option exists, the insurance policy of the vehicle's owner provides the necessary coverage for your immediate medical stabilization after a collision.

Is PIP coverage required for motorcycles in Florida?

No, Florida law doesn't require motorcycle owners to purchase PIP coverage. Because riders aren't covered by PIP, they often face higher financial exposure after an accident. This gap makes it imperative to secure a bespoke health insurance plan or specialized medical payments coverage. This Florida no-fault insurance explained guide highlights that motorcycles operate under different statutory requirements than standard four-wheeled vehicles in 2026.

Comments