Florida State Minimum Auto Insurance Requirements 2026: A Strategic Guide

- siinsuranceflorida

- 37 minutes ago

- 12 min read

If you believe that meeting the legal minimum for your car insurance provides a safety net for your personal wealth, you might be surprised to learn how quickly a single accident can dismantle your financial stability in the Sunshine State. We recognize that the escalating cost of premiums, with full coverage rates often reaching $4,100 per year, creates a significant burden for many drivers. It's understandable why you'd seek the most cost-effective path toward compliance with the florida state minimum auto insurance requirements 2026. However, staying within the legal baseline of $10,000 in Personal Injury Protection and $10,000 in Property Damage Liability might actually be your most expensive mistake if a serious incident occurs.

In this guide, we'll demystify the current no-fault system and show you exactly how to handle the mandates that Governor DeSantis maintained after vetoing the 2021 repeal efforts. You'll master the nuances of the 2026 mandates and discover why a strategic coverage plan is essential for true asset protection. We'll provide a clear framework for choosing limits that go beyond mere compliance, ensuring you avoid FLHSMV penalties while establishing a sophisticated defense for your financial future.

Key Takeaways

Identify the specific legal thresholds for the florida state minimum auto insurance requirements 2026 and why simply meeting them might leave your personal assets vulnerable.

Unpack the mechanics of Personal Injury Protection (PIP) to understand how it serves as your first line of defense for medical expenses in a no-fault environment.

Clarify the dangerous misconceptions surrounding "no-fault" status to ensure your policy actually satisfies the rigorous demands of Florida’s Financial Responsibility Law.

Evaluate the adequacy of your current limits against rising 2026 healthcare costs to determine if your coverage truly protects your long-term financial legacy.

Table of Contents Navigating the 2026 Florida Auto Insurance Landscape The Core Components: Understanding PIP and PDL in 2026 The No-Fault Fallacy: Strategic Misconceptions to Avoid Evaluating the Adequacy of State Minimums for Florida Drivers Strategic Risk Mitigation with SI Insurance

Navigating the 2026 Florida Auto Insurance Landscape

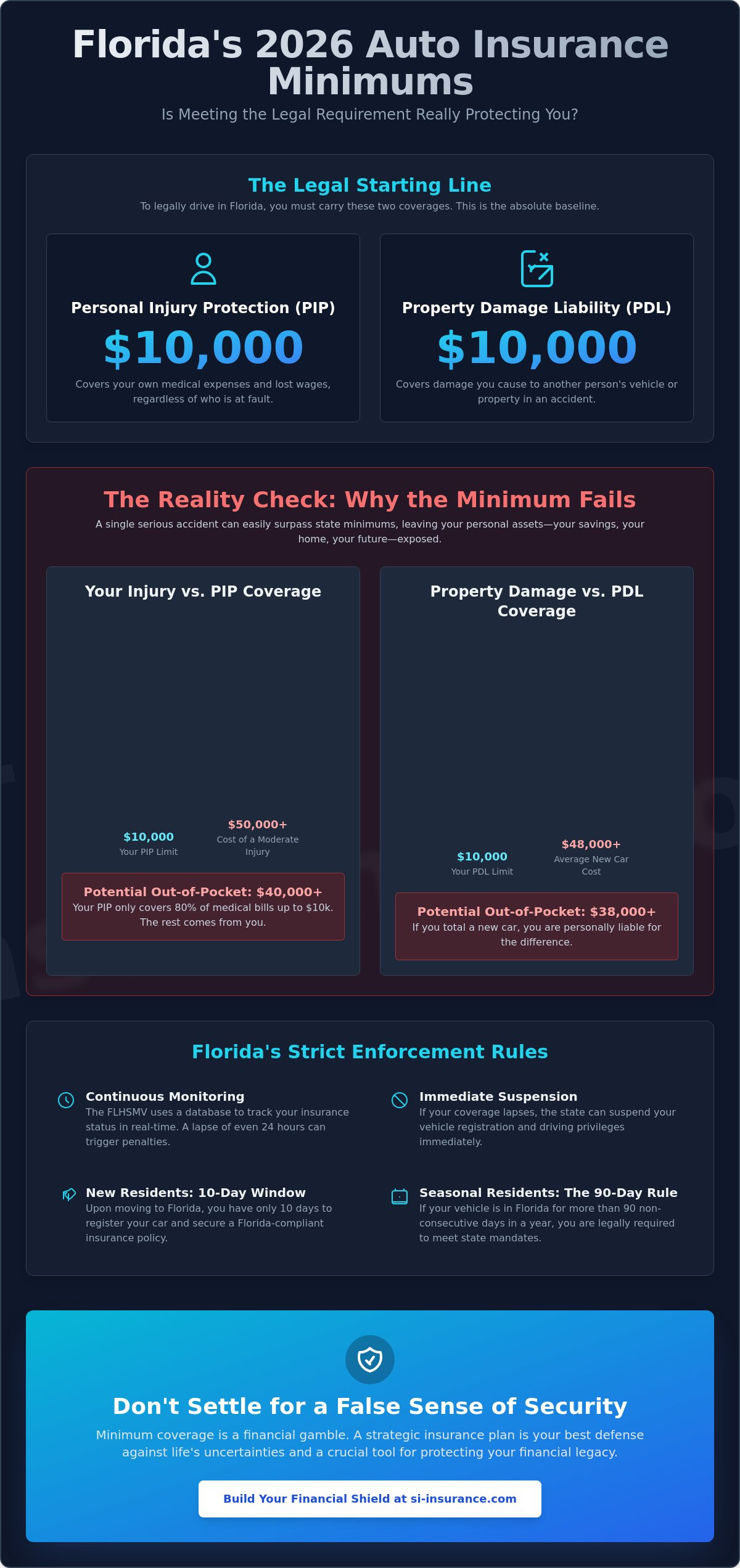

Florida’s insurance environment remains one of the most complex in the nation. To legally operate a vehicle with four or more wheels, you must secure a policy that meets the Florida's no-fault system standards. This requires maintaining $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL). These florida state minimum auto insurance requirements 2026 serve as the entry point for legal compliance, yet they represent a strategic baseline rather than a comprehensive shield for your assets.

The FLHSMV maintains a sophisticated database to monitor every registered vehicle in Broward County. If your coverage lapses for even 24 hours, the state’s automated systems can trigger a registration suspension. This rigorous oversight ensures that every driver contributes to the collective risk pool, but it also places the burden of proof squarely on the policyholder. It's not just about having a card in your glovebox; it's about verified, continuous data transmission between your carrier and the state.

To better understand how these components interact on the road, watch this helpful video:

The 2026 Regulatory Environment

Although recent legislative sessions saw attempts like SB 1256 to overhaul the system, the current PIP framework remains the law of the land for 2026. The latest reforms focus heavily on carrier transparency and the efficiency of claim processing. For high-net-worth individuals, these shifts mean that while the florida state minimum auto insurance requirements 2026 stay the same, the way carriers evaluate your total risk exposure is becoming more precise. Aligning your policy with these modern underwriting standards is essential for long-term stability.

Who Must Comply with Florida Mandates?

Compliance isn't optional for anyone calling Sunrise or Pompano Beach home. If you've just moved here, the state gives you a narrow 10-day window to register your car and secure a policy from a Florida-licensed agent. This rule applies even if you're a seasonal resident. If your vehicle spends more than 90 non-consecutive days in Florida during a 365-day period, you're legally bound to meet the state mandates. Many snowbirds overlook this 90-day threshold, but ignoring it can lead to severe legal penalties and the immediate suspension of your driving privileges. For those seeking a more bespoke insurance solution, understanding these timelines is the first step in a broader risk management strategy.

The Core Components: Understanding PIP and PDL in 2026

Let's get into the details. Every car insurance policy in Florida starts with two specific pieces. While the legal language can feel cold, these are just tools to manage the immediate mess after an accident. We see these florida state minimum auto insurance requirements 2026 as your first line of defense. They provide quick money when things go wrong. But here's the reality. If you don't understand how these parts work together, you're leaving your future to chance. It's about more than just a card in your wallet. It's about your peace of mind.

It is also worth remembering that these rules change if you're not just driving a personal car. For those running a business, the stakes are even higher. Taxis and commercial fleets have much tougher requirements to follow. You can't just stick to the basic minimums if you have employees on the road. Securing a bespoke auto insurance policy ensures your coverage actually fits your life or your business needs.

Personal Injury Protection (PIP) Mechanics

PIP is the part of your policy that pays out no matter who caused the wreck. It's often called "no-fault" for that reason. In 2026, the $10,000 limit follows a specific split. It covers 80% of your medical bills and 60% of your lost wages. It even includes a $5,000 death benefit. It's portable. That means it follows you whether you're in your car, a friend's SUV, or walking down the street. But be careful with your deductible choice. A high deductible lowers your monthly bill, but it also eats into that $10,000 cushion when you're already stressed from an injury. Check your deductible today. It matters more than you think.

Property Damage Liability (PDL) Realities

PDL is strictly for the other guy. It pays for things you hit, like their car, a fence, or even a building. The $10,000 state mandate hasn't kept up with the times. Think about it. The average new car in 2026 costs over $48,000. A small dent in a new electric vehicle can easily blow past your $10,000 limit. Repairs add up fast. If you cause a wreck in Broward County and the damage is higher than your limit, you're on the hook for the rest. This isn't just a legal threat. It can mean liens on your home or losing your savings. We've seen drivers lose everything over a single split-second mistake. It's a real risk that requires a better plan.

The No-Fault Fallacy: Strategic Misconceptions to Avoid

The term "no-fault" is perhaps the most misunderstood phrase in the Florida insurance lexicon. Many drivers operate under the dangerous assumption that this label provides a total shield against litigation, but this couldn't be further from the truth. While the florida state minimum auto insurance requirements 2026 ensure your own carrier handles your initial medical costs, they don't grant you immunity if you're responsible for a serious collision. Relying on the legal floor often stems from a misplaced confidence in "no-fault" protections that simply don't exist when high-value damages are on the line.

There's also a pervasive myth regarding "full coverage." Many people believe that if they've satisfied the state's mandates, they're fully protected against every possible scenario. In reality, "full coverage" isn't a legal or technical term; it's a marketing concept that often masks significant gaps in a risk management plan. A policy that only meets the florida state minimum auto insurance requirements 2026 is actually a "bare-bones" policy, leaving you exposed to the Financial Responsibility Law's strict post-accident penalties. For those who prioritize long-term security, a strategic auto insurance review is necessary to identify where these myths might be compromising your financial safety.

Liability Beyond PIP

Florida’s no-fault system only limits the right to sue for minor injuries. If an accident results in what the state defines as a "serious injury"—such as permanent loss of a bodily function, significant scarring, or death—the no-fault threshold is crossed. At this point, the injured party can pursue a lawsuit against you for pain, suffering, and medical costs that exceed their own PIP limits. Without Bodily Injury Liability (BIL) coverage, which isn't a mandatory part of the state's initial registration requirements, you're left to pay these legal fees and settlements out of your own pocket. BIL acts as a sophisticated barrier between your personal assets and the high costs of litigation.

The Financial Responsibility Law

The Financial Responsibility Law serves as a regulatory trigger that mandates higher limits exactly when you're most vulnerable. While you don't need BIL to get your tags, you must prove you have at least 10/20/10 coverage ($10,000 per person and $20,000 per accident for BIL, plus $10,000 for PDL) if you cause an accident involving injuries. If you're at fault and don't have this coverage, the state can suspend your driving privileges and vehicle registration until you provide proof of future financial responsibility. Essentially, the Financial Responsibility Law acts as a trigger for higher limits that effectively mandates BIL after an incident has occurred. Failing to plan for this "de facto" requirement can lead to immediate license suspension and a permanent stain on your driving record.

Evaluating the Adequacy of State Minimums for Florida Drivers

While satisfying the florida state minimum auto insurance requirements 2026 keeps you legally compliant, equating legality with safety is a dangerous strategic error. In the high-stakes environment of Florida's roadways, these entry-level limits often fail to account for the reality of modern financial exposure. Consider a standard multi-car collision on I-95 in Broward County. If you're deemed at fault in a chain-reaction accident involving three vehicles, your $10,000 Property Damage Liability limit will likely be exhausted by the first bumper repair. When you consider that the average cost of a new vehicle has climbed significantly, hitting a single late-model luxury car or a high-tech electric vehicle can leave you with an out-of-pocket deficit reaching tens of thousands of dollars. Choosing 'cheap' insurance might lower your monthly expenses, but it creates a massive hole in your financial defense that can lead to personal bankruptcy or asset seizure.

Medical Inflation and PIP Limitations

The $10,000 Personal Injury Protection limit has remained static for decades while medical costs have surged. By May 2026, a single emergency room visit followed by diagnostic imaging like an MRI can consume your entire PIP benefit in a matter of hours. This leaves you personally responsible for the remaining 20% of medical bills and any costs that exceed the cap. To address this, we often recommend Medical Payments (MedPay) as a strategic supplement. This additional layer covers the 20% gap that PIP leaves behind and provides a vital buffer for your immediate healthcare needs without the constraints of no-fault deductibles. For a deeper dive into these options, see our Florida Auto Insurance: A Strategic Guide to Coverage in 2026.

Asset Protection and Umbrella Solutions

For high-net-worth residents, the process of matching coverage limits to one’s total net worth represents the only logical path toward comprehensive risk mitigation. Relying on state minimums is effectively a high-stakes gamble with your primary residence, your diversified savings, and your future earnings potential. There's a distinct strategic advantage in bundling your auto policy with your Home Insurance in Florida to create a cohesive and impenetrable financial shield. This deliberate alignment often paves the way for a personal umbrella policy, which provides an elite layer of security that typically initiates at $1 million in additional liability coverage. It is the ultimate tool for individuals who have spent a lifetime meticulously building their legacy and refuse to see it dismantled by a single moment of misfortune on the road. To ensure your protection is as robust as your investment portfolio, consult with an SI Insurance advisor for a comprehensive policy review.

Strategic Risk Mitigation with SI Insurance

At SI Insurance, we don't think of insurance as just another monthly bill. We see it as a promise to protect the life you've worked so hard to build. Most companies are happy to sell you a policy that barely meets the florida state minimum auto insurance requirements 2026 and then move on. But we know your life isn't a one-size-fits-all situation. We take the time to really get to know you and find the hidden gaps that could cause trouble later. By working with a wide range of top-tier carriers, we find high-quality coverage that fits your specific needs without breaking your budget.

This isn't about pushing products you don't need. It's about making sure you have a real plan in place for 2026. Our team looks at your current coverage with a fresh pair of eyes to see where you might be vulnerable. We focus on your long-term safety and the preservation of your savings. It's a careful, thoughtful approach designed to give you total confidence every time you get behind the wheel. We're here to be your partner, not just your insurance agency.

Why a Local Broward County Agent Matters

Having a local agent here in Broward County makes a world of difference. South Florida has its own unique driving culture and local rules that big, out-of-state companies often don't fully grasp. When you work with us, you're talking to a neighbor who knows these roads as well as you do. We provide a personal touch that you won't find at a giant call center. If you ever have to file a claim, we're right here to walk you through it and make sure you're treated fairly. We're committed to looking ahead and keeping you protected as things change in our community.

Request Your Strategic Coverage Review

Moving from basic legal compliance to real, lasting security doesn't have to be a headache. Our team is ready to help you look at your options with a clear, honest analysis. we'll compare your current policy to the florida state minimum auto insurance requirements 2026 and show you exactly where a few small changes could make a massive difference for your safety. We've made it simple to get a quote that actually fits your life. Contact SI Insurance for a strategic auto insurance review today. Let's make sure you and your family are truly covered.

Securing Your Financial Legacy on Florida’s Roadways

Adhering to the florida state minimum auto insurance requirements 2026 is merely a regulatory starting point rather than a complete defense for your personal wealth. We've explored how the $10,000 caps on PIP and PDL often fail to meet the rising costs of medical care and vehicle technology. True security requires a shift from passive compliance to active risk management. You've worked hard to build your assets; protecting them demands a sophisticated approach that accounts for the reality of liability in Broward County.

Since our founding in 2022, SI Insurance has operated as an independent firm dedicated to elite risk management. We specialize in navigating the intricate South Florida market by providing bespoke coverage options from a network of premier carriers. Our advisors don't offer generic policies; they engineer strategic solutions tailored to your specific net worth and lifestyle. You deserve a partner that prioritizes foresight and intellectual precision over simple transactions. It's time to move beyond the minimums and establish a robust shield for your future. Secure your assets with a strategic auto insurance plan from SI Insurance. We look forward to helping you drive with absolute confidence.

Frequently Asked Questions

What happens if I cancel my Florida auto insurance without surrendering my plate?

Canceling your insurance without surrendering your license plate triggers an immediate electronic notification to the FLHSMV, which will likely lead to the suspension of your driver's license and registration. Florida law requires continuous coverage as long as a plate is active. To reinstate your privileges after a lapse, you'll be required to pay a fee ranging from $150 to $500, depending on whether it's your first or a subsequent offense.

Does Florida PIP coverage apply if I am in an accident outside of the state?

Your Florida PIP coverage generally extends to accidents occurring outside the state if you're driving your own insured vehicle or are a passenger in a relative's vehicle. However, this portability is strictly limited to the policyholder and residing family members. It won't cover you if you're struck as a pedestrian while outside of Florida. This is a vital nuance for seasonal residents who travel between states during the year.

Is Bodily Injury Liability (BIL) required for all drivers in Florida in 2026?

Bodily Injury Liability is not a mandatory requirement for initial vehicle registration under the florida state minimum auto insurance requirements 2026. While you only need PIP and PDL to secure your tags, BIL becomes a legal necessity under the Financial Responsibility Law if you're involved in an at-fault accident. Failing to have this coverage beforehand leaves your personal assets vulnerable to direct legal claims and state-mandated license suspensions.

How do the 2026 Florida insurance reforms affect my current PIP benefits?

The 2026 regulatory environment maintains the existing $10,000 PIP benefit structure because recent legislative attempts to repeal the no-fault system weren't enacted into law. These reforms primarily target insurance fraud and carrier transparency rather than altering the core 80/60 reimbursement rules. Consequently, your current benefits for medical expenses and lost wages remain subject to the same $10,000 limit that's been in place for several years.

Can I use an out-of-state insurance policy if I am living in Florida temporarily?

You can't use an out-of-state insurance policy if you live in Florida for more than 90 non-consecutive days within a 365-day period. Once you hit this threshold, or if you take a job or enroll a child in a local school, you must register your vehicle and secure a Florida-specific policy. Florida-licensed agents must issue these policies to ensure they comply with the specific statutes governing PIP and PDL.

What is the "Serious Injury Threshold" under Florida no-fault law?

The Serious Injury Threshold is a legal standard that allows an injured party to bypass no-fault restrictions and sue for non-economic damages like pain and suffering. To meet this criteria, the injury must involve significant and permanent loss of a bodily function, permanent scarring, or death. This threshold is the primary reason why state minimums are insufficient, as it opens the door to high-value litigation that PIP won't cover.

How much does property damage liability (PDL) actually cover in a 2026 accident?

Property Damage Liability covers exactly $10,000 in damages to another person's property per the florida state minimum auto insurance requirements 2026. In a modern context, this amount is often inadequate given that the average price of a new vehicle in 2026 is approximately $48,000. If you cause a collision that totals a newer car, you're personally responsible for the remaining $38,000 deficit, which can lead to significant financial distress.

Why is Florida considered a no-fault state if I can still be sued?

Florida is a no-fault state only in the sense that your own PIP handles your initial medical bills regardless of who caused the accident. This designation doesn't provide immunity from being sued for property damage or for bodily injuries that exceed the serious injury threshold. If you're at fault, the other party can pursue you for any costs that their own insurance doesn't cover, making liability insurance a strategic necessity for asset protection.

Comments