How to Lower Car Insurance Rates in Florida: A Strategic 2026 Guide

- siinsuranceflorida

- Apr 19

- 13 min read

Updated: Apr 28

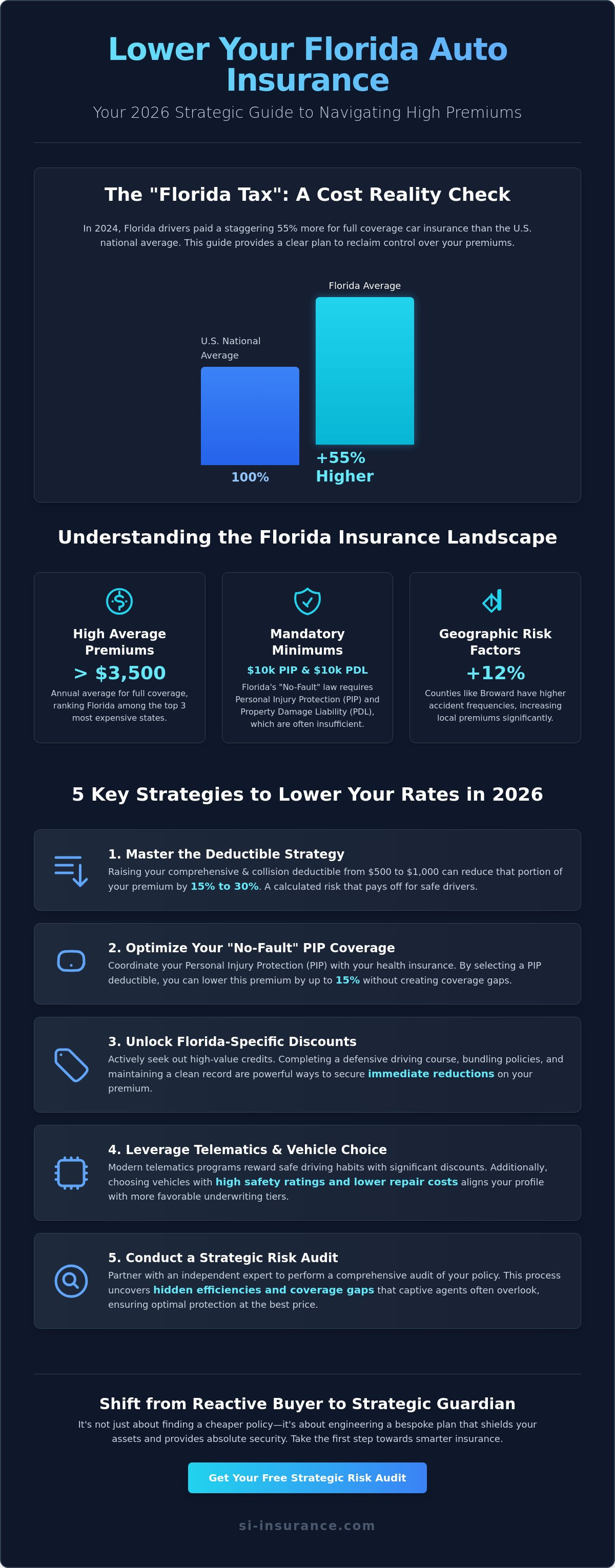

Did you know that Florida drivers paid an average of 55% more for full coverage than the rest of the country in 2024, a disparity that continues to challenge even the most meticulous financial planners? It's natural to feel frustrated by this persistent "Florida tax," especially when the nuances of Personal Injury Protection (PIP) and no-fault requirements remain so opaque. Most policyholders are actively seeking how to lower car insurance rates in Florida while ensuring their assets remain shielded by a strategic risk mitigation approach.

At SI Insurance, we prioritize underwriting excellence to help you reclaim control over your premiums. We'll show you how to secure the most competitive rates in the 2026 market without the vulnerability of subpar coverage. This guide provides a deliberate, step by step analysis of Florida's unique insurance landscape. You'll gain a clear plan to reduce your monthly costs and the confidence that your bespoke policy is engineered for both value and absolute security.

Key Takeaways

Gain a sophisticated understanding of Florida’s 2026 "No-Fault" system and how PIP requirements fundamentally dictate your premium structure.

Master the art of balancing risk and reward by learning how to lower car insurance rates in Florida through calculated deductible adjustments and strategic coverage limits.

Identify high-value defensive driving credits and exclusive Florida-specific discounts that offer immediate reductions in your annual insurance expenditure.

Leverage modern telematics and precise vehicle selection to align your profile with more favorable underwriting tiers in the evolving 2026 market.

Discover how a comprehensive Strategic Risk Audit by an independent partner can uncover hidden efficiencies that traditional captive agents often overlook.

Table of Contents Understanding the Florida Insurance Landscape in 2026 Strategic Policy Adjustments: Balancing Premium and Protection Leveraging Florida-Specific Discounts and Defensive Credits Risk Mitigation Through Technology and Vehicle Selection The SI Insurance Advantage: Your Strategic Partner in Florida

Understanding the Florida Insurance Landscape in 2026

Florida's auto insurance market entered 2026 with a reputation for both complexity and high costs. The state consistently ranks among the top three most expensive regions for drivers, with average annual premiums often exceeding $3,500 for full coverage. This financial pressure is driven by high population density in coastal corridors and a legal environment that has historically favored high-volume litigation. While state lawmakers passed significant tort reform in 2023, the actual impact on premiums only began to stabilize in late 2025. If you're looking for how to lower car insurance rates in Florida, you've got to look beyond simple discounts and understand the underlying risk structures. To build a solid foundation, it's helpful to review the broader context of Vehicle Insurance in the United States before diving into local nuances.

To better understand the fundamentals of reducing your premiums, watch this helpful video:

SI Insurance views the "Strategic Guardian" approach as a shift from reactive buying to proactive risk management. It isn't just about finding the cheapest policy; it's about aligning your coverage with your specific financial profile. This ensures you aren't over-insured for minor risks while remaining vulnerable to catastrophic ones. By 2026, litigation reforms have reduced "bad faith" lawsuits by approximately 22% in some sectors, yet the cost of vehicle repairs and medical care continues to climb, making a calculated approach to coverage essential for long-term security.

The Impact of Florida’s No-Fault Laws

Florida's "No-Fault" system requires every driver to carry $10,000 in Personal Injury Protection (PIP). This coverage is often seen as a fixed cost, but there's room for strategy. By coordinating your PIP with a primary health insurance policy, you can often apply a deductible to your PIP coverage, reducing that portion of your premium by up to 15%. This requires careful underwriting to ensure no gaps in medical care exist. Florida PIP works as a primary payer in 2026, providing immediate medical coverage regardless of who caused the accident.

Why Broward County Rates Differ from the Rest of Florida

Geography plays a massive role in your rate. In Broward County, drivers face some of the highest premiums in the state due to a 12% higher accident frequency compared to the state average. Dense traffic on the I-95 corridor and increasing flood risks from seasonal storms mean comprehensive coverage is more expensive here than in the Panhandle. Understanding these local variables is a key part of how to lower car insurance rates in Florida. For a deeper look at regional variations, check out our Florida Auto Insurance: A Strategic Guide to Coverage in 2026.

Strategic Policy Adjustments: Balancing Premium and Protection

Refining your insurance policy isn't just about cutting costs; it's about engineering a risk profile that aligns with your current financial standing. Many drivers wonder how to lower car insurance rates in Florida without exposing themselves to catastrophic loss. The answer lies in a meticulous audit of your policy's structural components. You must distinguish between what the state demands and what your assets actually require for safety. Florida law mandates $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL), but these figures rarely provide sufficient protection for modern financial risks. A balanced approach ensures you aren't overpaying for redundant features while remaining shielded from significant liabilities.

The Deductible Strategy: When to Raise Your Limits

Choosing a $1,000 deductible over a $500 option can often reduce your comprehensive and collision premiums by 15% to 30%. To determine if this is a sound move, calculate your break-even point. If the higher deductible saves you $250 annually, you'll need to go two years without an at-fault claim to recoup the potential $500 out-of-pocket difference. We recommend placing these annual savings into a dedicated high-yield account. This creates a self-insured buffer that maintains your liquidity while lowering your monthly overhead. It's a calculated decision that rewards long-term safety records with immediate cash flow improvements.

Auditing Comprehensive and Collision on Older Vehicles

As vehicles depreciate, the cost of insuring them against physical damage often outweighs the potential payout. A standard guideline involves the 10% rule. If the annual premium for collision and comprehensive coverage exceeds 10% of the car's total book value, the coverage is likely inefficient. For a vehicle valued at $5,000, paying $600 a year for full coverage rarely makes financial sense after accounting for your deductible. While you must maintain the state-required property damage liability, transitioning to liability-only for older secondary vehicles is a proven method for those looking at how to lower car insurance rates in Florida. This adjustment removes the expense of protecting an asset that the insurance company would simply total out in a minor accident.

It's vital to look beyond the minimums. The Florida Bar's Consumer Guide to Auto Insurance clarifies that while some coverages are optional, they are often essential for risk mitigation. Uninsured Motorist (UM) coverage is a prime example. Since roughly 20% of Florida drivers operate without insurance, UM acts as a critical safety net for your medical expenses and lost wages. Auditing your policy for redundant add-ons like roadside assistance or car rental reimbursement, which might already be covered by your credit card or vehicle warranty, allows you to reallocate those funds toward higher UM or liability limits. Strategic risk management requires a partner who understands the nuances of the local market. You can explore tailored risk solutions that prioritize both your budget and your long-term security.

Leveraging Florida-Specific Discounts and Defensive Credits

Finding effective ways for how to lower car insurance rates in Florida involves looking beyond the standard premium quote and identifying specific credits that reward proactive risk management. In the 2026 market, insurance carriers have refined their underwriting models to favor households that consolidate their exposure and demonstrate superior driving habits. These discounts aren't just minor adjustments; they represent a calculated reduction in your total cost of ownership when applied with precision.

Understanding the regulatory environment is a prerequisite for these savings. The Florida Bar consumer guide on auto insurance provides a clear baseline for the state's minimum coverage requirements, which helps policyholders identify which portions of their premium are most eligible for reduction. By aligning your coverage with these legal standards while maximizing available credits, you'll achieve a more efficient financial structure for your policy.

Defensive Driving: A Guaranteed Path to Savings

Enrolling in a Florida DHSMV-approved defensive driving course is one of the most reliable methods to secure a mandatory premium reduction. Florida law requires insurers to provide a discount to drivers aged 55 and older who complete an accident prevention course. This "Senior Citizen" credit typically applies for three consecutive years before a refresher course is necessary. To qualify for this reduction, the course must meet specific criteria:

The program must be officially approved by the Florida Department of Highway Safety and Motor Vehicles.

It must consist of at least six hours of instruction, though many 2026 providers offer streamlined digital formats.

You must provide a formal certificate of completion to your carrier to trigger the underwriting adjustment.

While the state mandate focuses on older drivers, many carriers extend similar credits to younger demographics who proactively seek training. It's a strategic move that signals to the insurer that you're a lower-risk asset. Most participating drivers see a 10% reduction in their liability and collision premiums immediately following certification.

Bundling Home and Auto: The Power of Strategic Alignment

Carriers offer their most aggressive pricing when they manage your entire risk portfolio. This concept, often referred to as Multi-Policy Strategic Alignment, reduces the administrative burden on the insurer and creates a more stable relationship. You can explore how this fits into a broader financial plan by reviewing our Home Insurance in Florida: A Strategic Guide. Beyond a percentage-based discount, bundling often unlocks the "single deductible" benefit. If a single event like a hurricane damages both your vehicle and your residence, some Florida carriers allow you to pay only one deductible, saving you thousands of dollars in out-of-pocket costs.

For families with students, Florida offers unique opportunities to lower expenses. Students maintaining a 3.0 GPA or higher often qualify for "Good Student" credits, which can reduce premiums by up to 15%. Additionally, the "Away at School" credit is vital if your child attends a university more than 100 miles from home without a car. This adjustment acknowledges the significantly reduced frequency of use while keeping the student covered during visits home. Implementing these strategies is essential for anyone researching how to lower car insurance rates in Florida effectively.

Risk Mitigation Through Technology and Vehicle Selection

Strategic risk management in 2026 requires a sophisticated understanding of how personal data and asset choice intersect with premium costs. To understand how to lower car insurance rates in Florida, you've got to look beyond basic coverage and examine the data-driven metrics insurers now prioritize. The shift toward bespoke risk transfer means your daily habits and your driveway's contents are under constant analytical scrutiny. This isn't just about following the rules; it's about aligning your lifestyle with the mathematical models that define underwriting excellence.

Telematics: Trading Data for Lower Premiums

Usage-based insurance (UBI) has matured into a standard tool for Florida drivers seeking premium optimization. By utilizing programs like Snapshot or DriveEasy, you allow carriers to monitor your driving telemetry in real time. These systems focus on high-risk behaviors, particularly hard braking events and operation during high-accident windows, such as the period between midnight and 4:00 AM. While the financial benefits are clear, there's a strategic trade-off. If the data reveals aggressive driving patterns, some carriers in the 2026 market may apply a surcharge rather than a discount. Drivers who are ideal candidates for these programs usually share specific traits:

Commuters with daily round-trips under 15 miles.

Individuals who rarely operate a vehicle after 11:00 PM.

Drivers who maintain consistent speeds and avoid sudden, jerky movements in heavy traffic.

Those comfortable with "white-glove" digital monitoring in exchange for a 10% to 30% discount.

Selecting a Car for Underwriting Excellence

The vehicle you choose dictates your placement within an insurer’s underwriting tiers. In high-density regions like Broward County, where theft rates and repair costs remain elevated, high-performance vehicles or models with known security vulnerabilities trigger immediate rate spikes. Choosing the right vehicle is a primary factor when considering how to lower car insurance rates in Florida while maintaining high-tier coverage. Mid-sized SUVs and sedans equipped with advanced driver-assistance systems (ADAS) consistently qualify for more competitive rates because they reduce the carrier's liability for bodily injury claims.

It's a calculated move to secure insurance quotes before you sign a purchase agreement. This foresight ensures your new asset aligns with your broader financial goals rather than creating an unexpected liability. Your credit-based insurance score also plays a silent but pivotal role here; carriers view a high score as a proxy for responsible asset management, often resulting in a 15% to 20% reduction in the final quoted rate compared to those with lower scores. Achieving absolute security in a volatile market requires a partner who understands these intricate variables.

Learn more about our approach to strategic risk management to protect your assets effectively.

The SI Insurance Advantage: Your Strategic Partner in Florida

Many drivers in the Sunshine State find themselves restricted by a captive agent who only represents a single brand. This narrow focus limits your options to one set of underwriting rules and pricing tiers. SI Insurance operates as an independent agency, which means we work for you rather than a specific carrier. We maintain professional relationships with a broad network of over 30 insurance providers to ensure your coverage is never a compromise. Our process begins with a Strategic Risk Audit. This isn't a simple price comparison; it's a deep dive into your current policy to identify hidden savings and technical redundancies that often inflate costs. Our team understands how to lower car insurance rates in Florida by aligning your specific risk profile with the carriers most likely to offer preferential terms in 2026.

Why an Independent Agency Wins in a High-Rate State

Florida’s insurance market is notoriously complex and volatile. With average premiums increasing by approximately 15 percent in 2024, finding value requires a sophisticated approach rather than a retail mindset. We compare dozens of carriers simultaneously to find the exact intersection of premium efficiency and robust protection. Our consultants advocate for you during the underwriting process. We ensure that every safety feature, professional discount, and loyalty credit is meticulously documented and applied to your file. This elite level of service is designed for clients who view insurance as a critical component of their broader financial portfolio. We offer a calm, calculated partnership that replaces the stress of rising rates with the confidence of expert foresight and stability.

Your Next Steps Toward Strategic Savings

Taking control of your insurance costs starts with a simple, professional consultation. You can initiate your 2026 strategy today by requesting a bespoke quote through SI Insurance Agency. We encourage our clients to undergo a Total Risk Review. This comprehensive evaluation examines your auto, property, and specialty assets to find cross-policy efficiencies that typical agents overlook. By looking at your entire risk landscape, we often uncover bundling advantages that help solve the puzzle of how to lower car insurance rates in Florida. Our firm remains committed to being the meticulous guardian of your assets and your lifestyle. We provide the stability and intellectual authority you need to navigate the high-stakes Florida insurance environment with absolute certainty and long-term protection.

Securing Your Strategic Advantage on Florida Roads

Navigating the complex 2026 insurance landscape requires more than just a passive approach. You've seen how Florida's 2023 Tort Reform Act continues to influence premium structures and why balancing your deductible with comprehensive protection is vital for long-term stability. By integrating advanced vehicle safety technology and leveraging Florida-specific defensive credits, you're not just saving money; you're engineering a more resilient financial profile. Understanding how to lower car insurance rates in Florida involves a meticulous blend of market foresight and disciplined risk mitigation—a strategy that also applies to home maintenance, where you can explore Water Heater Repair & Replacement to help prevent property damage and future insurance claims.

At SI Insurance, we don't believe in generic solutions for high-stakes environments. Our team provides specialized expertise in the Broward County and South Florida markets, ensuring your policy aligns with local risk variables. We perform a 360-degree risk audit for every client, utilizing our independent access to 30+ top-rated Florida carriers to find your ideal fit. It's time to move beyond standard retail options and embrace a more sophisticated method of asset protection. Request a bespoke strategic review of your Florida auto policy at SI Insurance to ensure your coverage is as robust as it is cost-effective. You've got the tools to succeed, and we're here to help you refine them.

Frequently Asked Questions

Why is car insurance in Florida so much more expensive than other states?

Florida's elevated premiums stem from a high volume of litigated claims and the state's unique no-fault system. Data from the Insurance Information Institute indicates that Florida generates 79% of the country's insurance litigation despite only having 9% of the claims. This creates a challenging environment for strategic risk mitigation, forcing carriers to adjust their underwriting excellence to account for these systemic costs. High accident frequency in dense urban areas like Miami also contributes to this volatility.

Does a defensive driving course really lower my insurance in Florida?

Completing an approved accident prevention course provides a reliable and strategic method for how to lower car insurance rates in Florida. Florida Statute 627.0652 requires insurers to provide a discount for three years to drivers aged 55 or older who finish a state-certified course. Most drivers see a 10% reduction in their premiums after presenting their certificate of completion to their carrier. It's a simple way to demonstrate a commitment to safe driving.

What is the minimum car insurance coverage required by Florida law in 2026?

Florida law in 2026 mandates a minimum of $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL). These requirements are established by the Florida Department of Highway Safety and Motor Vehicles to ensure basic financial responsibility. While these levels represent the legal floor, SI Insurance often suggests higher limits to ensure a more robust and bespoke risk transfer. This strategic approach protects you from the rising costs of medical care and litigation.

How much can I save by bundling my home and auto insurance in Florida?

Bundling your home and auto policies creates a strategic alignment that typically results in a premium reduction of 15% to 25%. This multi-policy approach simplifies your portfolio management while leveraging the carrier's appetite for total account retention. It's a proven tactic for those seeking a more sophisticated way to manage their overall risk profile. Most major Florida carriers offer these incentives to reward client loyalty and consolidate risk under a single underwriting umbrella.

Will my credit score affect my car insurance rates in Florida?

Your credit-based insurance score is a critical component in the underwriting process because carriers view it as a predictor of future claims. A 2024 report from the Federal Trade Commission found that drivers with poor credit scores pay 60% more on average than those with excellent ratings. Improving your score is a strategic move that directly influences the long-term stability of your insurance costs. It ensures you qualify for the most favorable underwriting tiers available.

What happens if I lower my coverage and then get into an accident?

Lowering your coverage limits increases your personal financial exposure if an accident occurs. If you carry only the state-mandated $10,000 in PDL and cause $25,000 in damages, you're legally responsible for the $15,000 shortfall. Data from the Florida Office of Insurance Regulation suggests that such deficits can lead to asset seizure or wage garnishment, undermining your strategic financial goals. It's vital to balance monthly savings with the potential for catastrophic out-of-pocket expenses.

Are there specific discounts for hybrid or electric vehicles in Florida?

Several carriers in the Florida market offer specialized discounts for hybrid and electric vehicles as part of their environmental risk mitigation strategies. For instance, companies like Travelers provide a 10% discount for drivers of alternative fuel vehicles. This incentive rewards clients who choose modern automotive technology, aligning their vehicle choice with strategic financial planning. It's an excellent way to reduce your carbon footprint while simultaneously optimizing your insurance expenditures through advanced underwriting credits.

How often should I shop for new car insurance rates in Florida?

You should perform a strategic review of your policy every 12 months to ensure you're receiving the most competitive rates available. Market conditions in Florida shift rapidly, and a 2025 consumer report highlighted that shopping annually can reveal price differences of $450 or more for the same coverage. Consistent evaluation is essential for maintaining a high level of underwriting excellence in your personal portfolio. It's a key tactic for how to lower car insurance rates in Florida effectively.

Comments