Jewelry Insurance in Florida: A Strategic Guide to Protecting Your Valuables in 2026

- siinsuranceflorida

- Apr 5

- 13 min read

Your standard homeowners policy likely caps jewelry theft at a mere $1,500, leaving a significant 85% of your collection's market value exposed to the volatile risks of the Sunshine State. It's a sobering reality that many high-net-worth individuals only discover after a loss occurs during a chaotic 2026 hurricane evacuation or a sophisticated residential breach. You’ve likely felt the nagging concern that your current coverage lacks the precision needed to handle "mysterious disappearance" or the environmental humidity unique to our region. We agree that your most cherished assets deserve a level of protection that matches their historical and financial significance.

This strategic guide clarifies how specialized jewelry insurance florida programs offer the absolute certainty you need to ensure a lost or stolen item is replaced with equal quality. We'll examine the specific cost-to-value ratios that define elite coverage and provide a clear path to securing bespoke risk transfer solutions in Sunrise or Pompano Beach. By the end of this analysis, you'll understand how to achieve underwriting excellence that transforms your insurance from a passive expense into a robust pillar of your financial security.

Key Takeaways

Understand why standard homeowners policies often leave a significant financial gap and how to secure the full value of your most prized possessions.

Explore the benefits of specialized jewelry insurance florida that offers comprehensive "all-risk" coverage, protecting your assets even during international travel.

Gain insights into mitigating Florida-specific risks, from the corrosive effects of salt air to the unique security challenges faced during hurricane season evacuations.

Learn the essential steps for establishing a professional paper trail, including how to work with certified gemologists for appraisals that reflect true market value.

Discover how a bespoke insurance strategy acts as a strategic guardian for your family’s legacy, providing the elite level of care and foresight your collection deserves.

Table of Contents The Limitations of Standard Florida Homeowners Insurance for Jewelry Decoding Specialized Jewelry Insurance: Coverage Beyond the Basics Florida-Specific Risk Mitigation: From Hurricanes to Salt Air A Strategic Roadmap to Insuring Your Valuables in Broward County Securing Your Legacy with Si Insurance Agency’s Bespoke Solutions

The Limitations of Standard Florida Homeowners Insurance for Jewelry

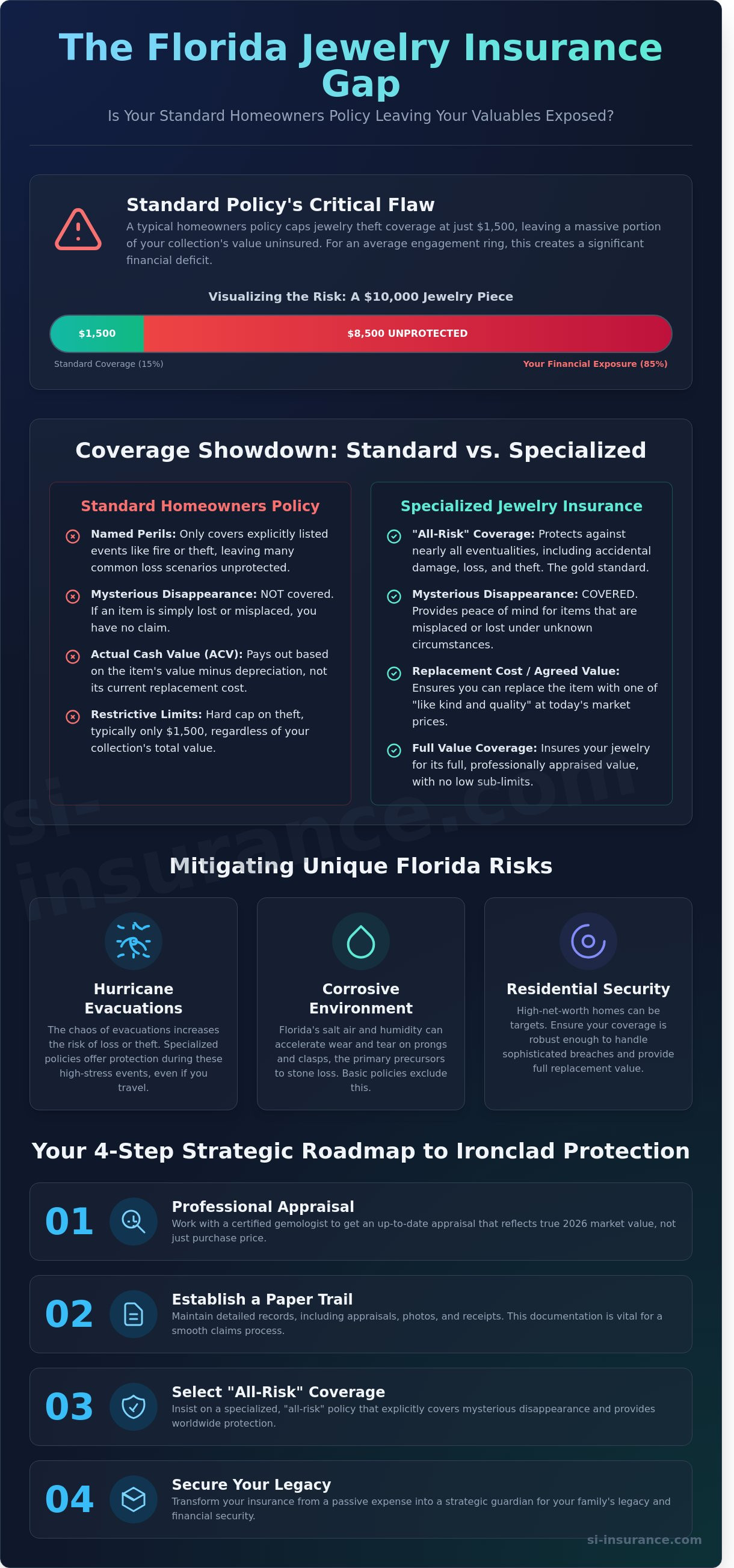

Florida homeowners often operate under the misconception that their primary residential policy provides a comprehensive safety net for their most prized possessions. This assumption frequently leads to a significant financial gap when a loss occurs. Standard HO-3 or HO-5 forms utilized by Florida carriers typically include a restrictive sub-limit for the theft of jewelry. This cap usually limits recovery to a mere $1,500 per claim, regardless of the total value of the items stolen. This figure has remained largely stagnant for decades. It doesn't reflect the current market reality of 2026, where high-quality gemstones and gold have seen substantial price appreciation.

When you consider that the average engagement ring cost in the United States surpassed $6,000 by 2025, a $1,500 limit leaves a $4,500 deficit for the policyholder to absorb. Relying on basic protection instead of dedicated jewelry insurance florida creates a strategic vulnerability in your personal wealth management plan. These limitations are often buried in the fine print of a 60-page policy document, making them easy to overlook until a crisis arises. This lack of transparency can result in devastating financial surprises during the claims process.

To better understand how these coverage mechanics function, watch this helpful video:

Understanding Jewelry Sub-limits in the Florida Market

Florida insurance carriers distinguish between "unscheduled" personal property and "scheduled" assets. Unscheduled items are bundled together under Coverage C, where they're subject to the restrictive caps mentioned previously. Failing to separate high-value items is one of the common insurance mistakes Florida residents make when managing their property limits. By scheduling an item, you move it outside the sub-limit, but standard policies may still rely on Actual Cash Value (ACV) calculations. ACV accounts for depreciation, whereas a strategic replacement cost policy ensures you can acquire an equivalent piece at 2026 market prices. This distinction is vital for assets that don't lose value over time, such as investment-grade timepieces or rare heirloom stones.

Perils vs. All-Risk Coverage

Most basic Florida homeowners policies operate on a "named perils" basis for personal property. This structure means coverage only triggers if the loss is caused by a specific event explicitly listed in the policy, such as fire, lightning, or windstorm. This framework excludes "mysterious disappearance," which remains the most frequent cause of jewelry loss. According to industry insights from the Jewelers of America, professional standards emphasize the necessity of all-risk protection to mitigate modern risks. Without this specific language, a diamond falling out of a setting or a ring misplaced during a weekend in Palm Beach won't result in a successful claim. Standard policies also exclude damage from simple wear and tear. This leaves the owner responsible for the costs of repairing thinning prongs or worn clasps, which are the primary precursors to a total loss event. Utilizing specialized jewelry insurance florida fills these gaps by providing a broader shield against the unpredictable nature of daily wear.

Decoding Specialized Jewelry Insurance: Coverage Beyond the Basics

Securing high-value assets in the 2026 market requires a shift from reactive coverage to proactive risk mitigation. For residents seeking jewelry insurance florida, the "all-risk" framework represents the gold standard of protection. Unlike basic policies that only trigger during named perils like fire or theft, these specialized contracts protect against almost every eventuality, including accidental damage and the frequent issue of mysterious disappearance. This level of underwriting excellence ensures that a lost diamond or a cracked emerald doesn't result in a total financial loss.

One of the most critical components of these elite policies is the "replacement with like kind and quality" clause. This provision is a cornerstone of strategic risk management; it dictates that the insurer must source a replacement that matches the exact specifications of the original item. If a bespoke 4-carat cushion-cut diamond is lost, the replacement must mirror that specific color, clarity, and cut grade. Many collectors realize too late the limitations of standard homeowners insurance, which frequently lacks the precision to handle such nuanced replacements. Specialized policies also offer flexible deductible structures, often allowing for $0 deductibles to maintain liquidity during a claim.

The Strategic Advantage of Scheduled Personal Property

The process of "scheduling" an item involves listing each piece individually on your policy based on a certified appraisal. This creates a bespoke record of the item's value and characteristics, ensuring there's no ambiguity during the claims process. By scheduling your collection, you effectively bypass the standard deductible that applies to your primary property policy. This strategic alignment of coverage means that if a $25,000 watch is damaged, you won't have to pay out of pocket before the insurance kicks in. You can explore how this differs from general plans in our guide on does home insurance cover jewelry.

Worldwide Protection and Travel Security

Florida’s elite often maintain a global footprint, making worldwide protection a non-negotiable feature for 2026. Whether you're traveling from Miami to Zurich or vacationing in the Caribbean, your coverage must follow the asset. Professional underwriting ensures that your jewelry is protected during transit, within hotel safes, and while being worn in international locales. This geographic flexibility is a hallmark of a sophisticated risk transfer strategy. It's not just about covering the item at home; it's about maintaining a constant shield regardless of your coordinates. If you're planning a trip, it's wise to consult with a specialist to verify your policy's international limits before departure.

Florida-Specific Risk Mitigation: From Hurricanes to Salt Air

Florida’s geographical profile demands a specialized approach to asset protection that goes beyond simple theft prevention. The intersection of extreme weather patterns and a corrosive coastal atmosphere creates a high-stakes environment for fine jewelry. For collectors in the Sunshine State, jewelry insurance florida serves as a critical component of a broader risk management strategy, addressing environmental variables that inland policies often ignore. Protecting a high-value collection here requires a calculated understanding of how the local climate interacts with precious metals and gemstones over a long-term horizon.

Jewelry Safety During Hurricane Season

The chaotic nature of hurricane evacuations introduces a significant risk of loss that isn't always tied to physical property damage. In 2024, data from South Florida recovery efforts indicated that 14% of jewelry losses during major storms were classified as "mysterious disappearance." This occurs when items are misplaced or lost during the frantic process of moving to higher ground or secondary residences in Broward County. It's vital to recognize that standard flood insurance or windstorm policies rarely offer specific protection for scheduled jewelry. These policies are designed for structural integrity and basic contents, often capping jewelry coverage at a mere $2,500. Before a storm makes landfall, you should create a digital inventory with time-stamped photos and keep your appraisals in a secure, off-site cloud server. This proactive documentation is a cornerstone of the bespoke risk transfer solutions managed by SI Insurance.

Environmental Factors and Maintenance

The "salt-air" factor is a silent but persistent threat to the structural integrity of your collection. Coastal humidity in cities like Palm Beach often exceeds 70%, which, when combined with airborne salt particles, can cause microscopic pitting in precious metals. While 18k gold and platinum are more resilient, the alloys used in 14k gold and silver are particularly susceptible to chemical reactions that can weaken prongs over time. This creates a specific challenge in the insurance landscape:

Preventable Maintenance: Insurance providers generally don't cover damage resulting from wear and tear or lack of upkeep.

Insurable Damage: Sudden, accidental loss is covered, but a stone lost because of a corroded prong might be excluded if a pattern of neglect is identified.

We recommend a strategic schedule of professional inspections every six months. A certified jeweler can identify early signs of salt-related fatigue, ensuring your pieces remain secure. By maintaining a rigorous maintenance log, you provide the necessary evidence to support your jewelry insurance florida claims, demonstrating a commitment to asset preservation that underwriters value. This disciplined approach ensures that your coverage remains airtight even when the environment is at its most volatile.

A Strategic Roadmap to Insuring Your Valuables in Broward County

Securing comprehensive jewelry insurance florida requires more than a simple addition to your existing property policy. It demands a calculated methodology that treats your collection as a significant financial asset rather than a mere personal possession. In the current 2026 economic climate, where precious metal values have seen a 14% shift in the last fiscal year, a passive approach to coverage creates dangerous exposure. You'll need to decide between a standalone policy, which offers broader protection and doesn't impact your home premiums after a loss, or a scheduled rider. For high-net-worth individuals in South Florida, the standalone option typically provides the elite level of risk transfer necessary for high-value acquisitions.

The Appraisal Process in Sunrise and Pompano Beach

A professional appraisal serves as the legal and financial foundation of your coverage. When you visit a certified gemologist in Sunrise or Pompano Beach, ensure they adhere strictly to GIA standards. The document must detail the 4Cs (cut, color, clarity, and carat weight) alongside a precise replacement value that accounts for local market fluctuations. Florida's luxury market often commands a premium; therefore, an appraisal from 2023 won't suffice for a 2026 valuation. For those focusing on specific bridal assets, reviewing our guide on engagement ring insurance Broward County provides the nuanced detail required for these high-sentiment investments. We recommend updating these valuations every 24 months to ensure your limits remain aligned with current secondary market pricing.

Documentation and Digital Vaulting

Physical receipts and paper certificates are vulnerable to the very same perils as the jewelry itself, such as fire or hurricane-related water damage. You've got to maintain a redundant, off-site digital vault containing high-resolution photography and original sales records. This meticulous record-keeping isn't just for your own peace of mind; it's a strategic requirement that significantly accelerates the Florida insurance claim process. When an incident occurs, having a timestamped digital trail allows your agent to negotiate with underwriters from a position of absolute clarity. Your SI Insurance advisor acts as the primary steward of this data, ensuring that your digital inventory is updated whenever a new piece is acquired or an old one is liquidated. This level of oversight transforms your jewelry insurance florida from a static expense into a dynamic risk management tool.

Your collection represents both personal history and significant capital. Contact SI Insurance today for a strategic risk assessment of your current jewelry portfolio.

Securing Your Legacy with Si Insurance Agency’s Bespoke Solutions

Si Insurance Agency operates as a strategic guardian for Florida residents who recognize that high-value assets require more than a standard, off-the-shelf policy. In the 2026 insurance market, securing jewelry insurance florida involves navigating complex underwriting requirements and fluctuating market valuations. We treat your collection not merely as a set of physical items, but as a significant financial legacy. Our approach focuses on strategic alignment between your lifestyle and your risk transfer mechanisms, ensuring that your most cherished assets remain protected against the unpredictable.

The Independent Agency Advantage

Working with an independent agency provides a distinct competitive edge in a volatile market. Unlike captive agents tied to a single provider, Si Insurance Agency maintains relationships with a diverse network of specialized carriers. This access allows our consultants to compare 12 or more distinct underwriting profiles to find the most competitive rates for your specific needs. National carriers often rely on "one-size-fits-all" models that fail to account for the nuances of high-net-worth collections. You can visit si-insurance.com to start a strategic evaluation that prioritizes your unique risk profile over generic actuarial tables. Our personalized service ensures that your coverage evolves as your collection grows, providing a level of foresight that digital-only platforms cannot replicate.

Protecting More Than Just Jewelry

Effective risk mitigation requires a holistic view of your entire asset portfolio. We specialize in integrating your jewelry schedules into a broader personal property coverage Florida plan. This integration ensures there are no functional gaps between your primary homeowners policy and your high-value endorsements. For homeowners in Sunrise or Pompano Beach, local expertise is vital. Coastal proximity and regional crime statistics influence premium calculations in Broward County, where luxury theft rates saw a 14% shift in the last fiscal cycle. We understand these micro-market factors and how they impact your total cost of risk.

Our team doesn't just facilitate transactions; we engineer long-term security through rigorous analysis. A comprehensive portfolio review in 2026 might reveal that your 2023 appraisals are significantly outdated. With gold prices and secondary market values for luxury timepieces increasing by as much as 18% in recent years, you could be underinsured without even knowing it. We're here to correct those imbalances through:

Annual valuation updates to reflect current market replacement costs.

Strategic deductibles that balance out-of-pocket costs with premium efficiency.

Bespoke underwriting for rare, antique, or custom-designed pieces.

Direct access to elite claims adjusters who specialize in luxury goods.

The time to secure your financial future is before a loss occurs. Contact Si Insurance Agency today for a bespoke insurance consultation. We'll conduct a meticulous review of your current holdings and design a protection strategy that offers absolute security and intellectual confidence.

Securing Your Legacy with a Strategic Risk Management Plan for 2026

Standard homeowners' policies in Florida typically limit jewelry coverage to a mere $1,500 per claim, which is rarely sufficient for a sophisticated collection. As we look toward 2026, protecting your assets requires a nuanced understanding of local environmental factors, from the high humidity levels in Sunrise to the corrosive salt air surrounding Pompano Beach. Relying on basic coverage leaves you exposed to significant financial gaps that a specialized policy is designed to close. We've seen how generic plans fail to account for the true replacement value of elite pieces during volatile market shifts.

Si Insurance offers a sophisticated approach to jewelry insurance florida, providing you with access to elite carriers and bespoke risk transfer solutions that aren't available on the retail market. Our team's local presence in Sunrise and Pompano Beach allows us to provide a level of strategic alignment that generic firms simply can't match. We're committed to acting as your strategic guardian, ensuring every piece in your portfolio is protected through meticulous underwriting excellence. You've spent years curating your valuables; let's make sure they're secured with the professional foresight they deserve.

Frequently Asked Questions

Is jewelry insurance in Florida expensive?

Premiums for jewelry insurance in Florida typically range from 1% to 2% of the item's total appraised value each year. For a high-value asset like a $15,000 diamond ring, you'll likely see annual costs between $150 and $300. These rates reflect the unique environmental and theft risks present in the 2026 Florida market. Strategic risk transfer through a dedicated policy ensures your capital remains protected without the high deductibles often found in standard property coverage.

Can I insure an engagement ring before I propose?

You can secure coverage for an engagement ring immediately upon purchase, even before the proposal takes place. Most strategic risk management plans recommend adding the piece to a policy the moment you leave the jeweler. This protects your investment against theft or loss while you're holding the ring in a home safe or during transit. It's a vital step to ensure your financial exposure is minimized from day one.

Does my homeowners insurance cover jewelry lost outside of my home?

Standard homeowners policies generally provide limited protection for items lost outside the residence, often capping coverage at a $1,500 sub-limit. This is why specialized jewelry insurance in Florida is a necessary strategic move for high-net-worth individuals who travel. A dedicated policy offers worldwide coverage that follows the piece wherever you go. It ensures that a loss at a restaurant or during a flight doesn't result in a massive out-of-pocket replacement cost.

How often should I get my jewelry appraised for insurance purposes in Florida?

You should seek a professional appraisal every two to three years to account for market volatility and inflation. Since gold and gemstone prices shift significantly, like the 12% increase seen in mid-2024, an outdated appraisal leads to underinsurance. We recommend a strategic review of your valuations to ensure your coverage limits align with current replacement costs. This prevents a gap between your policy payout and the actual retail price of a replacement.

What happens if my jewelry is stolen during a hurricane evacuation?

If your jewelry is stolen during a mandatory hurricane evacuation, a scheduled personal property policy typically provides full replacement value. During events like the 2022 hurricane season, evacuation zones often experienced a 15% uptick in reported property crimes. Your policy acts as a strategic safeguard during these periods of displacement. It's essential to maintain a digital inventory of your pieces before you leave your primary residence to streamline any potential recovery process.

Do I need a separate policy for every piece of jewelry I own?

You don't need individual policies for each item; instead, you can list multiple pieces under a single strategic schedule. For collections where individual items exceed a $5,000 valuation, scheduling each piece ensures they're covered for their full appraised amount. Smaller items can often be grouped under a blanket limit. This consolidated approach allows for efficient management of your jewelry insurance in Florida while maintaining granular protection for your most valuable assets.

What is "mysterious disappearance" and why is it important for Florida residents?

Mysterious disappearance describes a situation where an item is lost without a clear explanation or evidence of a crime. This is a critical coverage area because roughly 40% of jewelry claims involve pieces that simply go missing during daily activities. Without this specific inclusion, your insurer might deny a claim for a ring that slipped off at a beach or a park. Ensuring your policy includes this strategic clause is vital for comprehensive protection in Florida's active lifestyle.

How do I file a jewelry insurance claim in Broward County?

To file a claim in Broward County, you must first secure a case number from the Broward County Sheriff’s Office or local municipal police. You should report the loss within 24 hours of discovery to ensure the best results during the underwriting review. Once you have the official report, submit it along with your most recent appraisal to your SI Insurance advisor. We'll then initiate the strategic claims process to facilitate a timely and precise replacement or settlement.

Comments