Understanding My Florida Auto Policy: A Strategic Guide to Your Coverage in 2026

- siinsuranceflorida

- Apr 22

- 13 min read

Would you remain financially secure if a single traffic incident in 2026 triggered a lawsuit exceeding your current liability limits? With Florida's private passenger auto insurance rates increasing by approximately 14% since the start of 2024, many policyholders find themselves paying more for coverage they don't fully comprehend. It's exhausting to manage the rising costs of living while worrying that a "no-fault" label won't actually protect you from a courtroom. At SI Insurance, we recognize that understanding my Florida auto policy is no longer just a clerical task; it's a vital component of your broader strategic risk management. You likely feel that the gap between your premiums and your actual peace of mind is widening. This guide will clarify the technical jargon found in your documents and help you align your coverage with the state's evolving legal landscape. We'll explore how to optimize your policy limits and implement bespoke risk transfer strategies that prioritize both institutional stability and personal affordability. By the end of this analysis, you'll have the intellectual confidence to navigate your insurance renewals with precision.

Key Takeaways

Decode your Declarations Page to identify potential coverage gaps and ensure your policy period aligns with your long-term security goals.

Uncover the reality behind Florida’s "No-Fault" requirements and learn how to structure your Personal Injury Protection for genuine medical benefit.

Protect your financial future by debunking the "full coverage" myth and addressing the critical liability risks that minimum policies often ignore.

Gain a strategic advantage in understanding my Florida auto policy by learning how to tailor your coverage for unique regional threats like hurricanes and flooding.

Discover how a professional policy audit can replace generic insurance with a bespoke risk management plan designed for your specific needs.

Table of Contents Decoding the Declarations Page: Your Florida Auto Policy Blueprint Mandatory vs. Strategic Coverage: Navigating Florida’s Requirements The 'Full Coverage' Trap: Why Minimums May Leave You Vulnerable Beyond the Minimums: Tailoring Protection for the Sunshine State Optimizing Your Policy with Si Insurance Agency

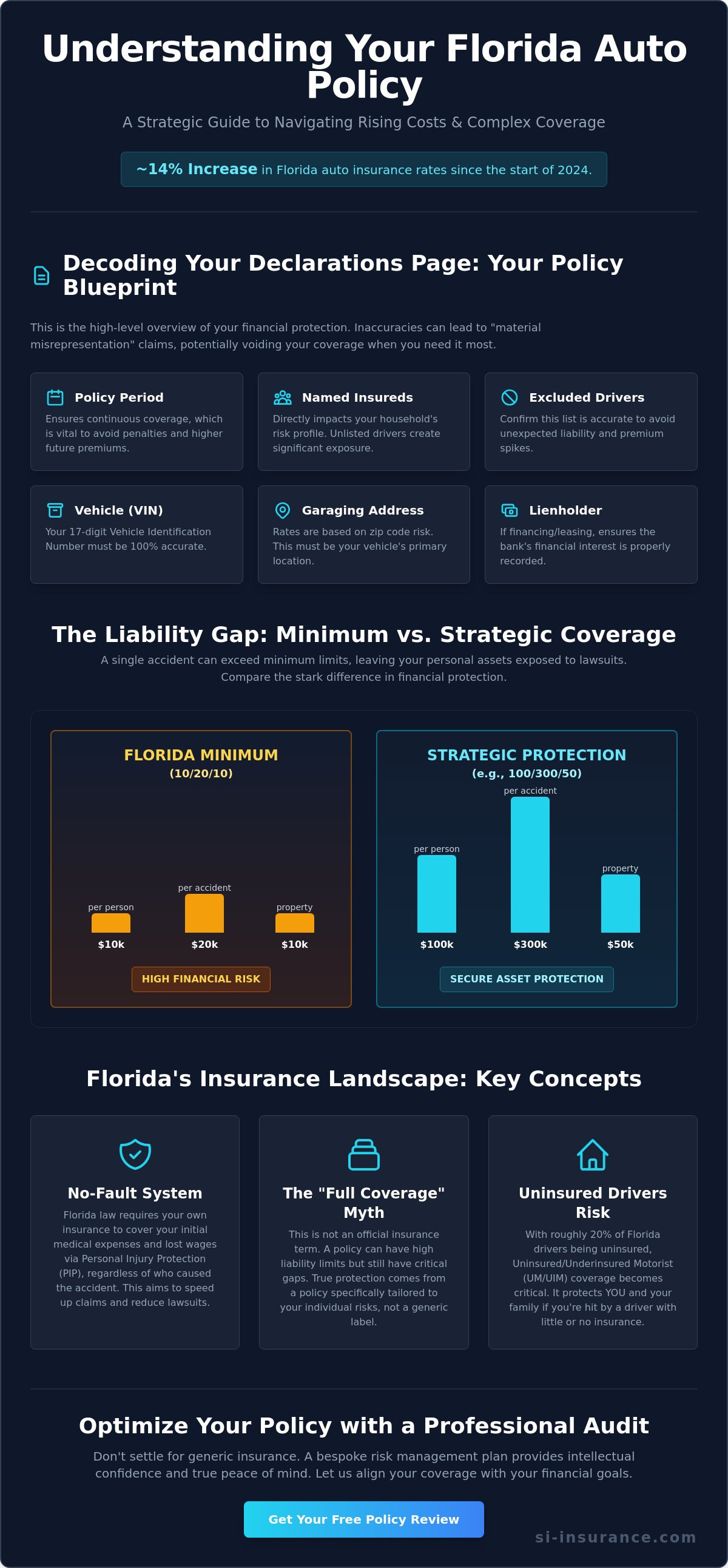

Decoding the Declarations Page: Your Florida Auto Policy Blueprint

The Declarations Page, often called the "Dec Page," serves as the strategic blueprint for your entire insurance contract. It isn't just a summary; it's a high-level overview that defines the scope of your financial protection. When you're focused on understanding my Florida auto policy, this document is your starting point. You'll find the "Policy Period" clearly stated at the top. Maintaining a continuous coverage history is vital in Florida. Statistics from the Insurance Research Council suggest that roughly 20 percent of Florida drivers operate without insurance. Gaps in your history can lead to registration suspension or increased premiums during future underwriting cycles.

To better understand this concept, watch this helpful video:

The Dec Page also lists "Named Insureds" and "Excluded Drivers." This section directly impacts your household's risk profile. If a driver lives in your home but isn't listed, or is explicitly excluded, you face significant exposure. Reviewing the premium breakdown for each vehicle allows you to see exactly where your capital is allocated. This transparency ensures your risk mitigation strategy aligns with your actual driving habits. At SI Insurance, we prioritize this clarity to ensure your assets are protected through precise underwriting excellence and bespoke risk transfer solutions.

The Anatomy of a Policy Header

Accuracy in the header is non-negotiable. You must verify your 17-digit Vehicle Identification Number (VIN) and your specific garaging address. Inaccurate data can lead to "material misrepresentation" claims, which might void your coverage during a total loss event. Your policy number is the primary identifier for all strategic communication with SI Insurance, facilitating efficient account management and rapid claims processing. Look for these key items:

Lienholder: Check this if you're financing or leasing to ensure the bank's interest is properly recorded.

Garaging Address: Rates are calculated based on the specific risk of your zip code, so this must be current.

Excluded Drivers: Confirm that anyone you've intentionally removed from the policy is listed here to avoid premium spikes.

Translating Insurance Shorthand

Deciphering the numerical strings on your policy is essential for true risk management. In Vehicle Insurance in the United States, these figures represent specific financial caps. A "10/20/10" policy provides the bare Florida legal minimums: $10,000 for one person's injuries, $20,000 total per accident, and $10,000 for property damage. For those seeking elite protection, a "100/300/50" structure is a more robust strategic choice. Understanding my Florida auto policy requires knowing that "Per Person" limits apply to each individual claimant, while "Per Occurrence" limits represent the total pool of funds available for all injuries in a single event.

Carriers also use specific symbols to denote coverage tiers. These symbols act as a shorthand for complex captive solutions or standard market offerings. Understanding these codes helps you confirm that your policy meets your expectations for long-term security. It's a steady, methodical way to ensure your financial health remains uncompromised by unforeseen liabilities on the road.

Mandatory vs. Strategic Coverage: Navigating Florida’s Requirements

Florida operates as a no-fault state, a designation that fundamentally dictates the architecture of your insurance claims process. This legal framework requires your own insurance provider to cover your medical expenses and lost wages up to a certain limit, regardless of who caused the collision. While the system aims to reduce the burden on the court system, it creates a complex environment where understanding my Florida auto policy becomes a prerequisite for effective risk mitigation. Relying solely on the state's baseline requirements often leaves sophisticated policyholders exposed to significant financial liabilities that far exceed the mandatory caps.

The legal baseline for maintaining a valid vehicle registration involves two specific components: Personal Injury Protection (PIP) and Property Damage Liability (PDL). While Florida's minimum insurance requirements mandate only $10,000 for each of these coverages, this figure is often a tactical error for those with significant assets to protect. In a landscape where the average cost of a new vehicle in 2024 has surpassed $47,000, a $10,000 limit for property damage is mathematically insufficient to cover even a moderate multi-car accident.

The Truth About Personal Injury Protection (PIP)

PIP is designed to provide immediate liquidity for medical needs, covering 80% of your medical bills and 60% of lost wages resulting from an accident. However, the efficacy of this coverage depends on strict compliance with the 14-day rule. If you don't seek professional medical treatment within exactly 14 days of the incident, your right to claim PIP benefits is entirely forfeited. It's also vital to evaluate how your PIP deductible interacts with your primary health insurance. Choosing a high PIP deductible might lower your premium, but it creates a gap where you're responsible for initial costs before your health insurance or PIP benefits even begin to apply.

Property Damage Liability (PDL) Explained

PDL functions as your primary defense against claims involving damage you cause to other people's vehicles, fences, or buildings. PDL is the shield that protects your assets from third-party lawsuits. Without adequate limits, a single moment of negligence can lead to personal judgments and the seizure of liquid assets. For a more comprehensive look at how these elements fit into a broader financial plan, refer to our Florida Auto Insurance: A Strategic Guide to Coverage in 2026. Achieving true security requires understanding my Florida auto policy not just as a legal checklist, but as a carefully engineered component of your wealth preservation strategy. To ensure your current limits align with your long-term goals, you might consider a consultation regarding bespoke risk transfer solutions tailored to high-value portfolios.

The 'Full Coverage' Trap: Why Minimums May Leave You Vulnerable

Many motorists operate under the dangerous assumption that "full coverage" provides an absolute safety net against financial loss. This term is a marketing colloquialism with no legal standing in the state. In reality, a policy that meets only the state's minimum requirements often excludes the very protections necessary for long-term financial security. Truly understanding my Florida auto policy requires a shift from viewing insurance as a monthly bill to seeing it as a tool for strategic risk mitigation.

If your policy lacks Bodily Injury (BI) liability, you're personally responsible for every dollar of damage you cause beyond the $10,000 Property Damage limit. In 2026, medical costs and vehicle valuations have reached levels where a minor lapse in judgment can lead to a judgment that exceeds your annual income. When insurance limits are exhausted, plaintiffs often seek personal asset seizure to satisfy the balance. This makes matching your coverage limits to your total net worth a fundamental requirement for any professional risk strategy. At SI Insurance, we view this alignment as the baseline for elite financial protection.

The Role of Bodily Injury Liability (BI)

BI coverage is not a legal requirement for most Florida drivers, yet it's the most critical component of a robust policy. It manages the costs associated with the other party's pain, suffering, and ongoing rehabilitation. Beyond paying for damages, BI coverage triggers your insurer's duty to defend. This means the insurance company pays for your legal representation during a lawsuit. The Florida Bar's consumer guide to auto insurance provides an excellent overview of how these legal obligations interact with the state's no-fault laws. Without this protection, you're forced to fund a private legal defense out of pocket, which can cost thousands before a case even reaches trial.

Uninsured Motorist (UM) Coverage

Florida maintains one of the highest rates of uninsured motorists in the country, with figures often hovering around 20% according to recent industry data. UM coverage is designed to protect you when the at-fault driver lacks sufficient insurance or disappears after a hit-and-run. It's a bespoke layer of protection that ensures your recovery isn't dependent on the financial responsibility of a stranger. For multi-vehicle households, the choice between "stacked" and "non-stacked" UM is a critical decision.

Stacked UM: This option combines the limits of all vehicles on your policy. If you have two cars with $100,000 limits, you effectively have $200,000 in protection.

Non-Stacked UM: This limits the payout to the amount specified for the vehicle involved in the accident, which may be insufficient for catastrophic injuries.

For those seeking absolute security, a stacked approach is the preferred method to maximize the available capital during a crisis. It ensures that your family’s health and financial stability aren't compromised by the negligence of an underinsured driver.

Beyond the Minimums: Tailoring Protection for the Sunshine State

Florida’s unique geography dictates a specialized approach to risk management. While the state mandates PIP and PDL, these bare essentials fail to address the environmental volatility inherent in the Sunshine State. Tropical systems and sudden flooding aren't just possibilities; they're statistical certainties in 2026. Truly understanding my Florida auto policy requires a shift from mere compliance to comprehensive risk mitigation. This strategic alignment of coverage is as vital for your vehicle as it is for your residence; you can explore similar protections in our guide to Home Insurance in Florida. Without these layers, a driver remains personally liable for total losses caused by rising water or fallen debris during the Atlantic hurricane season.

Comprehensive and Collision: The Physical Damage Duo

Comprehensive and collision coverages represent the bedrock of physical vehicle protection. Collision coverage manages the financial impact of impacts with other vehicles or stationary objects, regardless of who's at fault. Comprehensive coverage addresses non-collision events like theft, vandalism, and the heavy floods that characterize Florida's coastal regions. A critical step in understanding my Florida auto policy is evaluating the difference between Actual Cash Value (ACV) and Replacement Cost. ACV accounts for depreciation, which often leaves a significant gap in funding a new purchase if your vehicle is totaled. For high-value assets, a bespoke replacement cost policy provides superior underwriting excellence.

Strategic drivers also use deductibles as a lever to control costs. A higher deductible reduces the monthly premium but requires greater liquidity during a claim. It's a calculated trade-off. Additionally, Florida Statute 627.7288 provides a unique benefit: the zero-deductible windshield law. This mandate ensures that glass repair or replacement is covered without out-of-pocket costs, emphasizing safety on the road. This legislative protection is vital for maintaining clear visibility without financial barriers.

Strategic Add-Ons for Modern Drivers

Modern driving in 2026 demands more than basic repair funds. Rental reimbursement ensures your mobility while a vehicle undergoes long-term repairs. This is particularly relevant today, as supply chain complexities can extend shop timelines by 15 percent compared to previous years. Gap insurance is another essential tool, especially for those financing new vehicles where the loan balance exceeds the car's depreciated value. Finally, roadside assistance provides a layer of sophisticated convenience. It manages the logistics of mechanical failures on busy corridors like I-95 or the Florida Turnpike, ensuring that a breakdown doesn't derail your professional schedule. These aren't just extras; they're components of a well-engineered risk transfer strategy.

Optimizing Your Policy with Si Insurance Agency

Managing risk requires more than just paying a premium; it demands a calculated approach to asset protection. At Si Insurance Agency, we function as your strategic consultants rather than mere order-takers. We recognize that understanding my Florida auto policy involves more than skimming a few pages of legal jargon. Gaining a thorough understanding my Florida auto policy requires a deep dive into how specific coverage limits interact with your unique financial profile. Because Florida laws and carrier appetites shift frequently, having a dedicated partner to monitor these changes is vital for your long-term security.

As independent agents, we aren't tethered to a single provider. We leverage our relationships with a broad network of carriers to find the exact alignment for your needs. If your current coverage feels like a generic, one-size-fits-all product, it likely leaves you exposed. We shop the market to ensure your liability limits, deductibles, and endorsements are engineered to protect your specific interests. Whether you're managing personal assets or a commercial fleet, we focus on bespoke risk transfer solutions that prioritize your financial stability.

The SI Insurance Strategic Audit

Our process begins with a meticulous review of your current Declarations Page. We hunt for hidden vulnerabilities, such as insufficient Uninsured Motorist coverage or redundant costs that don't add value to your portfolio. In 2025, Florida saw a 15 percent increase in average litigation costs, making it essential to have airtight liability protection. Our expertise allows us to identify these gaps before a claim occurs. For a deeper look at how different providers stack up, you can explore our Top Auto Insurance Companies in Florida: A Strategic Comparison for 2026.

Securing Your Quote Today

If you suspect your current Florida policy is insufficient, the time to act is now. Transitioning from a basic policy to a bespoke risk management plan is a straightforward process when guided by our professionals. We serve all cities across the State of Florida, providing the local expertise needed to navigate this complex market. Our team provides the clarity and foresight you need to feel confident in your coverage. You can experience the SI Insurance difference with a strategic auto policy review to ensure your assets are fully protected against the unexpected.

Contact our experts for a comprehensive document review and vulnerability assessment.

Identify and eliminate coverage overlaps that lead to unnecessary expenditures.

Secure a quote that reflects your actual risk profile rather than a generic demographic average.

We don't just sell insurance. We provide the intellectual framework for your financial safety. By choosing Si Insurance Agency, you're opting for a partnership rooted in stability and precision. Let's move beyond basic coverage and build a strategy that withstands the complexities of the Florida market in 2026.

Elevate Your Personal Risk Management Strategy for 2026

Navigating the nuances of insurance in the Sunshine State requires more than a cursory glance at a declarations page. A truly robust approach involves understanding my Florida auto policy through the lens of comprehensive asset protection rather than mere regulatory compliance. As we move into 2026, the limitations of Florida's No-Fault laws and standard minimums become increasingly apparent for those with significant wealth to shield. Relying on basic coverage often creates a false sense of security that leaves high-value assets vulnerable to unforeseen litigation and complex liability claims.

SI Insurance Agency functions as a dedicated strategic guardian, utilizing specialized expertise to engineer bespoke risk transfer solutions. By representing an elite selection of top-tier carriers, our independent agency ensures that your protection isn't just a generic product but a meticulously balanced financial instrument. It's essential to move beyond the "full coverage" trap and implement a plan that reflects your unique risk profile. Schedule a strategic review of your Florida auto policy with SI Insurance Agency to secure a level of intellectual confidence that only elite underwriting excellence can provide. We look forward to refining your coverage into a powerful tool for long-term stability.

Frequently Asked Questions

Is Florida a no-fault state and what does that mean for my policy?

Florida remains a no-fault state under Florida Statute 627.736, so your own insurance handles initial medical expenses regardless of who caused the collision. This framework requires you to maintain Personal Injury Protection to ensure immediate risk mitigation for minor injuries. It's a foundational element in understanding my Florida auto policy because it limits the right to sue unless injuries meet a specific legal threshold. SI Insurance views this as a primary layer of your strategic defense.

What is the minimum auto insurance coverage required in Florida for 2026?

For the 2026 calendar year, Florida law mandates a minimum of $10,000 in Personal Injury Protection and $10,000 in Property Damage Liability. While these figures represent the absolute legal floor, they rarely provide sufficient protection for high-value assets or complex liability scenarios. We suggest a more robust strategic alignment of limits to prevent personal financial exposure. Relying solely on state minimums often leaves gaps that sophisticated risk management strategies are designed to close.

Does my Florida auto policy cover me if I drive out of state?

Your policy provides coverage across all fifty U.S. states, U.S. territories, and Canada, ensuring your protection isn't confined by geographic borders. If you're involved in an accident outside of Florida, your policy typically adjusts its limits upward to meet the specific financial responsibility laws of that jurisdiction. This automatic broadening clause is a standard feature in SI Insurance contracts. It ensures your risk transfer mechanism remains functional and effective during interstate travel or temporary relocation.

What happens if I have an accident with an uninsured driver in Florida?

If you encounter an uninsured driver, your Uninsured Motorist coverage becomes the primary vehicle for recovering damages related to bodily injury. Since the Insurance Research Council noted in a 2023 report that roughly 20 percent of Florida motorists lack insurance, this coverage is a critical component of any strategic risk plan. Without it, you might be forced to pursue personal assets through litigation, which is often a fruitless and expensive process for the policyholder.

Can I change my coverage limits in the middle of a policy term?

You're permitted to adjust your coverage limits or add endorsements at any point during your policy term through a formal request. These mid-term modifications are processed as endorsements, and SI Insurance will calculate any premium adjustments on a pro-rata basis for the remaining duration. This flexibility allows for the strategic recalibration of your protection as your lifestyle or asset portfolio evolves. It's an essential part of maintaining an agile and responsive insurance posture.

Why is my Florida auto insurance premium so high compared to other states?

Florida's premiums are elevated due to high litigation rates, frequent severe weather events, and a high density of uninsured motorists. According to 2024 data from the Insurance Information Institute, Florida remains one of the most expensive markets for personal lines. These costs reflect the complex underwriting excellence required to manage such volatile variables. SI Insurance focuses on bespoke risk transfer solutions to help clients navigate these market pressures while maintaining superior levels of institutional security.

What is the difference between stacked and unstacked uninsured motorist coverage?

Stacked coverage allows you to combine the Uninsured Motorist limits of multiple vehicles on a single policy or across different policies. For example, if you have two cars with $50,000 limits, stacking them provides $100,000 in total protection for a single incident. This is a vital nuance in understanding my Florida auto policy for households with multiple drivers. Unstacked coverage is less expensive but limits you to the amount assigned to the specific vehicle involved.

Do I need to list all household members on my Florida auto policy?

You're required to list all licensed household members and any regular operators of your vehicles to ensure accurate risk assessment. Failure to disclose these individuals can lead to a denial of claims or the rescission of the policy due to material misrepresentation. SI Insurance emphasizes full transparency during the underwriting process to maintain the integrity of your strategic protection. It's the only way to ensure that your bespoke coverage remains valid when an accident occurs.

Comments