What Affects Home Insurance Premiums in Florida? A 2026 Strategic Guide

- siinsuranceflorida

- 19 hours ago

- 12 min read

What if the persistent cycle of double-digit rate hikes in the Sunshine State is finally reaching its conclusion? For years, you've likely watched your renewal notices with a sense of dread, wondering exactly what affects home insurance premiums in Florida when you haven't even filed a claim. It's a frustrating position to be in, especially when technical terms like reinsurance and litigation ratios seem to dictate your financial security from behind a curtain. We understand that feeling of powerlessness against state-wide shifts, but the landscape in 2026 is showing signs of a sophisticated stabilization that rewards the informed homeowner.

You've probably noticed that the market feels volatile, and you're right to seek clarity on how your specific property fits into this complex puzzle. This guide provides a strategic roadmap to help you regain control, moving beyond the confusion of technical jargon to offer a clear view of the current market drivers. We'll explore how recent legislative reforms, such as the 2026 roof age protections and the influx of new carriers, are creating opportunities for lower rates. By the end of this analysis, you'll have a precise plan for utilizing home improvements and wind mitigation to secure your coverage at the most competitive price possible.

Table of Contents

Understanding the Landscape of Florida Home Insurance in 2026

Florida's insurance environment has long been characterized by its volatility, but 2026 marks a period of calculated transition. To truly grasp what affects home insurance premiums in Florida, one must first recognize that a premium is simply the cost of transferring significant financial risk from an individual to a carrier. In our state, this transfer is overseen by the Florida Office of Insurance Regulation (OIR), which evaluates rate filings to ensure they're neither excessive nor inadequate. While your individual home profile matters, you're also part of a collective risk pool. When a neighborhood experiences a surge in claims, the financial weight is distributed across the carrier's entire portfolio; this means your bill reflects the broader regional risk as much as your own property's health.

To gain a deeper understanding of these market shifts, watch this helpful summary of current trends:

The State of the Market: Florida vs. The Rest of the US

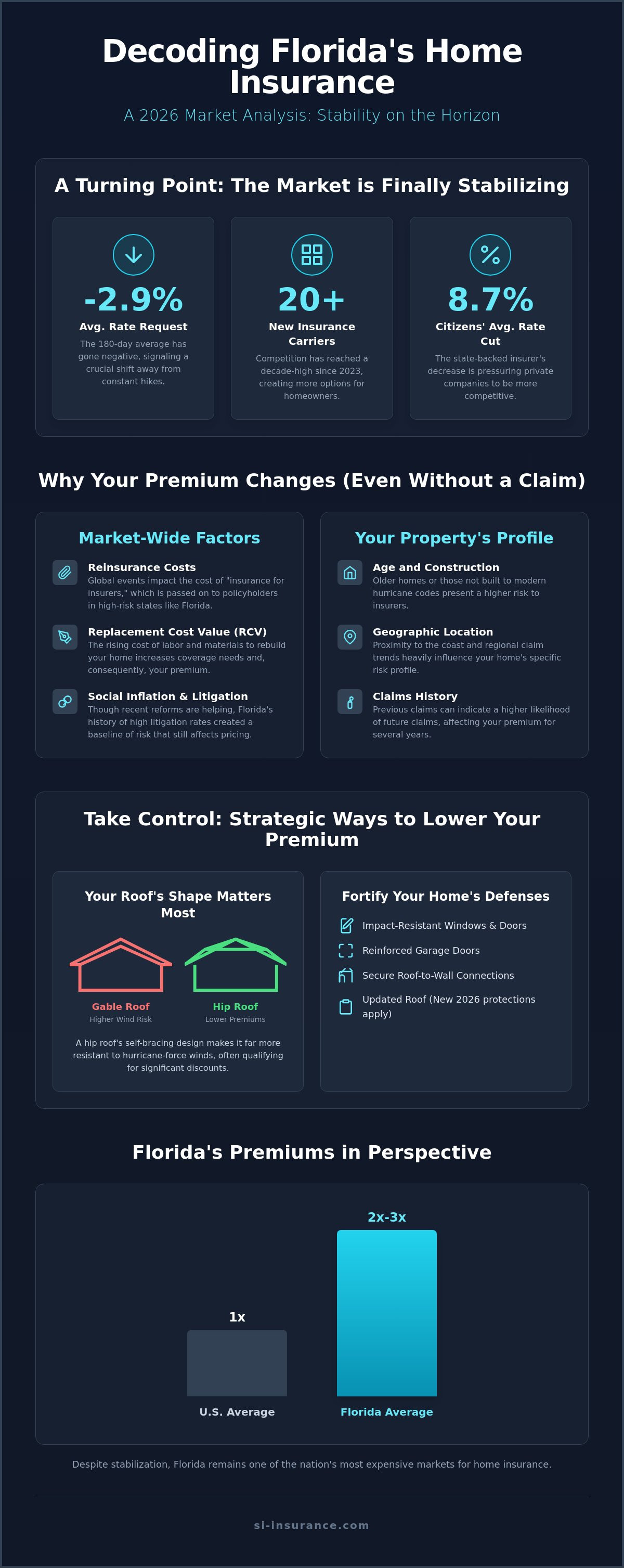

Florida remains an outlier compared to national benchmarks, with average premiums often doubling or tripling those in landlocked states. However, the internal variance is just as striking. A property in Sunrise or Pompano Beach faces different actuarial pressures than one in the Panhandle. Much of this is driven by the Citizens Property Insurance market. As of early 2026, Citizens has implemented a statewide average rate decrease of 8.7%, with Broward and Miami-Dade counties seeing cuts as high as 14%. This downward pressure from the state-backed insurer of last resort is forcing private carriers to refine their pricing to remain competitive, creating a more balanced market for homeowners insurance across the state.

The 2026 Outlook: Stability or Volatility?

The current year represents a pivotal shift toward stability. Recent legislative reforms, specifically those targeting frivolous litigation and fraudulent claims, have finally begun to manifest in lower rate filings. The OIR reports that the 180-day average for property rate requests has dropped to -2.9%, a statistic that would've seemed impossible just three years ago. With 20 new domestic property insurance writers entering the Florida market since 2023, competition is at its highest level in a decade. While inflation still impacts the cost of labor and materials, the structural health of the market suggests that the era of runaway price hikes is being replaced by a more measured, analytical approach to risk management.

Macro-Economic Drivers: Why Rates Rise Without a Claim

It's a common grievance among Florida residents: your home hasn't suffered a scratch, yet your premium continues its upward climb. This phenomenon occurs because what affects home insurance premiums in Florida extends far beyond your personal claims history. Carriers must account for the Replacement Cost Value (RCV), which is the current expense to rebuild your home from the ground up using today's labor and material prices. Even if your property's market value stays flat, the cost of specialized Florida construction labor and high-grade materials often outpaces general inflation, forcing insurers to adjust their coverage limits and pricing accordingly.

Social inflation also plays a significant role in this equation. This term describes the rising costs of insurance claims due to societal trends, such as increased litigation and larger jury awards. While the legislative reforms of 2024 and 2025 have begun to curb the most aggressive litigation practices, carriers still have to account for the historical data of a state that once accounted for the vast majority of the nation's property insurance lawsuits. This collective history creates a baseline of risk that affects every policyholder in the state.

Reinsurance: The Insurance for Insurance Companies

Local carriers don't shoulder the entire burden of Florida's risk alone; they purchase their own coverage from global entities known as reinsurers. This global connection means that a catastrophic earthquake in Japan or a massive wildfire in California can deplete the global capital pool, indirectly raising your local rates. However, there's a silver lining in 2026. Data shows that reinsurance rates for Florida decreased by approximately 25% for June 1 renewals. This relief, combined with the stability provided by the Florida Hurricane Catastrophe Fund (FHCF), is a primary reason we're seeing more competitive filings from domestic carriers this year.

The Hidden Cost of Rebuilding

Modern building codes are another silent driver of escalating costs. If your home was built two decades ago, bringing it up to current 2026 standards after a loss requires significantly more expensive engineering, such as advanced roof-to-wall connections and impact-rated materials. During a "demand surge" following a major storm, the scarcity of qualified contractors can send labor prices skyrocketing overnight. It's vital to remember that your insurance value isn't based on what you could sell your home for on the open market. Instead, it's a technical calculation of what it takes to physically recreate your asset in the current economic climate.

Navigating these macro-economic shifts requires a partner who looks at the data through a local lens. If you're concerned about how these global trends are impacting your specific policy, it might be time to consult with a specialist who can audit your current RCV and ensure your coverage is precisely aligned with today's rebuilding reality.

Property-Specific Variables: How Your Home Profile Dictates Cost

While global reinsurance and litigation trends set the baseline for the state, the physical characteristics of your residence determine where you land on the pricing spectrum. This is the "property DNA" that underwriters scrutinize to assess risk. Understanding what affects home insurance premiums in Florida at this granular level is essential for any homeowner looking to optimize their coverage. From the materials used in your plumbing to the year your foundation was poured, every detail tells a carrier how likely they are to face a future claim.

The Roof: Your First Line of Defense

Your roof's age and shape are arguably the most significant factors in the actuarial equation. As of July 1, 2026, Florida law provides a shield for homeowners through HB 815; insurers can't refuse to renew a policy solely because of roof age if the roof is less than 15 years old. For those with roofs older than that, a determination of at least five years of useful life by an authorized inspector can prevent a non-renewal. Beyond age, geometry matters immensely. A "hip" roof, which slopes downward on all four sides like a pyramid, typically qualifies for higher discounts than a "gable" roof. This is because hip roofs perform better under high wind pressure, while gables can act like a sail, catching the wind and risking structural failure. Additionally, installing secondary water resistance (SWR), a specialized underlayment that protects the decking, is a technical upgrade that carriers reward with premium credits.

Home Systems and Maintenance

Carriers also look beneath the surface at your home's internal systems through a specialized "Four-Point Inspection." If your electrical system still utilizes cloth wiring or outdated panels like Federal Pacific, you'll likely face higher premiums or significantly limited carrier options. These older components are viewed as fire hazards that modern standards simply don't tolerate. Similarly, plumbing materials are a key variable in your risk profile. Modern PEX or copper piping is viewed as a low-risk choice, whereas older polybutylene pipes are often seen as a liability due to their history of failure and water damage. The age of your central heating and cooling system also plays a role; an HVAC system nearing the end of its 20-year lifecycle suggests a higher probability of mechanical failure, which can influence your overall rate.

Finally, your personal history and the home's geographic location round out the profile. Proximity to the coast and the Base Flood Elevation (BFE) play a role in determining your risk for storm surge and water intrusion. Your individual insurance score and your past five years of claims history are also critical components of what affects home insurance premiums in Florida. Even a single prior claim for water damage can shift your risk profile, signaling to carriers that the property might be prone to future issues, even if the repairs were completed to code.

Strategic Mitigation: Proven Methods to Influence Your Premium

While you can't control the global reinsurance market or state-wide litigation trends, you have significant agency over the physical and financial variables of your own property. Understanding what affects home insurance premiums in Florida is the first step toward active cost management. By implementing specific, verifiable structural upgrades, you move from being a passive recipient of rate hikes to an active participant in your risk engineering. This proactive approach doesn't just protect your physical asset; it signals to carriers that your property represents a lower actuarial risk, which is rewarded through mandated credits.

The Wind Mitigation Framework

The Wind Mitigation Inspection is your most potent instrument for premium reduction. It isn't just a cursory glance at your shingles; it's a technical audit of your home’s ability to withstand uplift forces during a tropical event. To maximize these savings, follow this structured progression:

Step 1: Hire a licensed inspector to document your home’s structural integrity through the lens of the Florida Building Code.

Step 2: Focus on "nailing patterns" and "roof-to-wall attachments." Carriers provide significantly higher credits for 8D nails spaced six inches apart and for "clips" or "wraps" that secure the rafters to the wall studs, rather than simple toenailing.

Step 3: Ensure the inspector completes the OIR-B1-1802 form. Submitting this document to your carrier is the only way to trigger the state-mandated mitigation credits that can slash the wind portion of your premium.

Security and Smart Home Discounts

Beyond structural hardening, modern technology offers new avenues for savings. Monitored fire and burglar alarms remain a standard requirement for reducing the "theft and fire" portion of your bill, but 2026 has seen the emergence of water leak detection systems as a significant new discount category. These smart sensors can automatically shut off your main water valve upon detecting an irregular flow, preventing the high-frequency interior water damage claims that carriers find particularly unattractive. Additionally, if your property is located within a gated community with 24-hour manned security, you likely qualify for lower base rates due to the statistically lower probability of theft and vandalism.

Finally, consider the balance between your out-of-pocket risk and your monthly expenses. Adjusting your hurricane deductible from a 2% threshold to a 5% option can yield substantial premium relief, provided you have the liquidity to manage the higher cost in the event of a claim. Bundling your home insurance with your auto or personal umbrella policies also remains a classic, yet highly effective, method for securing multi-line discounts. If you're ready to see how these credits can be applied to your specific profile, request a strategic policy review with our team today to ensure you're not leaving mandated savings on the table.

Navigating the Florida Market with Si Insurance Agency

Understanding the technical nuances of what affects home insurance premiums in Florida is only the first half of the equation; the second half is execution. In a landscape where legislative shifts and reinsurance fluctuations occur with high frequency, the traditional transactional model of insurance is no longer sufficient for high-value assets. Since our founding in 2022, Si Insurance Agency has operated as an independent provider, a structure that offers a distinct advantage over captive agents. We aren't bound to the pricing or underwriting appetites of a single company. Instead, we act as a sophisticated risk manager, utilizing our multi-carrier access to identify the specific insurer whose current portfolio best aligns with your property's unique risk profile.

Why a Local Broward County Agent Matters

A deep familiarity with the local geography of Sunrise and Pompano Beach is essential for accurate risk engineering. We understand that the flood zones and wind requirements in Broward County aren't just data points on a spreadsheet; they're the realities of your daily environment. This local perspective allows us to provide personalized consulting that a generic, national platform simply can't replicate. It's about more than just a quote; it's about Si Insurance Agency's commitment to the Broward community and our role as a protective guardian for your most significant investments. Having a human advocate who knows the local building codes and hurricane deductible nuances ensures that your coverage remains airtight during the complex claims process.

Designing Your 2026 Coverage Strategy

The stabilization we're seeing in 2026 presents a unique opportunity to recalibrate your protection. Our methodology goes beyond basic data entry; we perform a meticulous risk analysis that accounts for the specific engineering of your home, including the secondary water resistance and roof attachments documented in your mitigation reports. We don't believe in "set it and forget it" policies. As market conditions shift and new carriers enter the Florida market, an annual review of your policy becomes a strategic necessity rather than a formality. This measured, step-by-step progression ensures your insurance costs remain competitive without sacrificing the elite level of security your lifestyle demands. You can consult with a Si Insurance specialist today to audit your current premium and begin designing a strategy that prioritizes long-term stability.

Securing Your Financial Future in a Stabilizing Market

The transition into 2026 has brought a welcome shift toward stability in the Sunshine State. By now, it's clear that the combination of legislative reform and a more competitive reinsurance market is creating a rare window for homeowners to recalibrate their expenses. Understanding precisely what affects home insurance premiums in Florida, from your roof's structural geometry to the technical nuances of your wind mitigation credits, is no longer just a benefit; it's a financial necessity. You've learned that while macro-economic forces set the stage, your specific property engineering and your choice of advocate determine your final rate.

At Si Insurance Agency, we combine our elite expertise in Broward County with independent access to Florida’s top-rated carriers to ensure your protection is never generic. We invite you to Request a Strategic Florida Home Insurance Review and experience a level of risk management founded on intellectual confidence and meticulous analysis. It's time to stop feeling powerless against rate hikes and start engineering a policy that reflects the true value of your assets. We look forward to helping you navigate this new landscape with absolute security and confidence.

Frequently Asked Questions

Why did my home insurance go up if I didn’t file a claim?

Your premium reflects the collective risk of the state and the rising cost of labor and materials. Even without a personal loss, your carrier must adjust for the escalating expense of rebuilding homes to modern codes, a factor known as Replacement Cost Value. Additionally, the price of reinsurance, which is the protection carriers buy for themselves, fluctuates based on global disaster trends and indirectly impacts your local bill.

How much can a wind mitigation inspection save me in Florida?

A wind mitigation inspection is often the most effective way to reduce your costs. By documenting features like roof-to-wall clips and secondary water resistance, you trigger state-mandated credits that can lower the wind portion of your premium by a significant percentage. These discounts are applied based on the OIR-B1-1802 form, ensuring your home’s structural integrity is financially rewarded by your carrier.

Does the age of my roof affect my Florida home insurance premium?

Roof age is a primary driver of risk and pricing. Carriers view newer roofs as less likely to fail during a tropical event, whereas older systems often lead to surcharges or limited coverage options. Under 2026 regulations, a roof less than 15 years old cannot be the sole reason for non-renewal, but its age still dictates the technical tier of your premium and determines which carriers are willing to assume the risk.

What is the difference between a hurricane deductible and a standard deductible?

A hurricane deductible is a percentage-based amount, typically 2% to 10% of your home's insured value, that applies only to damage from a named storm. In contrast, your standard deductible is a fixed dollar amount for other losses like fire or theft. Choosing a higher hurricane deductible can be a strategic way to lower your monthly costs if you have the liquidity to manage the out-of-pocket risk after a major event.

Can I get home insurance in Florida with an older roof?

You can secure coverage for an older roof, provided an authorized inspector determines it has at least five years of useful life remaining. While legislation now prevents insurers from non-renewing solely based on age for roofs up to 15 years, an older roof will likely attract higher rates. Carriers often require a Four-Point inspection to verify that the roof remains structurally sound before they'll offer a binding policy.

Is flood insurance required for all homes in Florida?

Flood insurance isn't universally required by state law, but it's often a mandatory condition for homeowners in high-risk zones with a mortgage. Additionally, policies through Citizens Property Insurance Corporation increasingly require flood coverage regardless of your specific flood zone. Given that standard policies exclude rising water, we generally recommend this coverage as a critical layer of your risk management strategy to avoid total loss.

How does my credit score affect my insurance rates in Florida?

Most carriers use a credit-based insurance score to help determine what affects home insurance premiums in Florida for your specific profile. Actuarial data suggests a correlation between financial stability and claim frequency, which means a higher score often leads to more favorable pricing tiers. While it's only one factor among many, maintaining a strong credit history remains a sophisticated tool for managing your overall insurance expenses.

What are the benefits of bundling home and auto insurance in Florida?

Bundling your home and auto insurance with a single carrier provides immediate financial relief through multi-policy discounts. Beyond the savings, it simplifies your risk management by centralizing your coverage under one protective guardian. This strategy often makes you a more attractive client to carriers, which can be particularly beneficial during periods of market volatility when carriers are more selective about the risks they choose to insure.

Comments