Affordable Auto Insurance in Florida: A Strategic Guide for 2026

- siinsuranceflorida

- Mar 13

- 15 min read

Updated: Mar 15

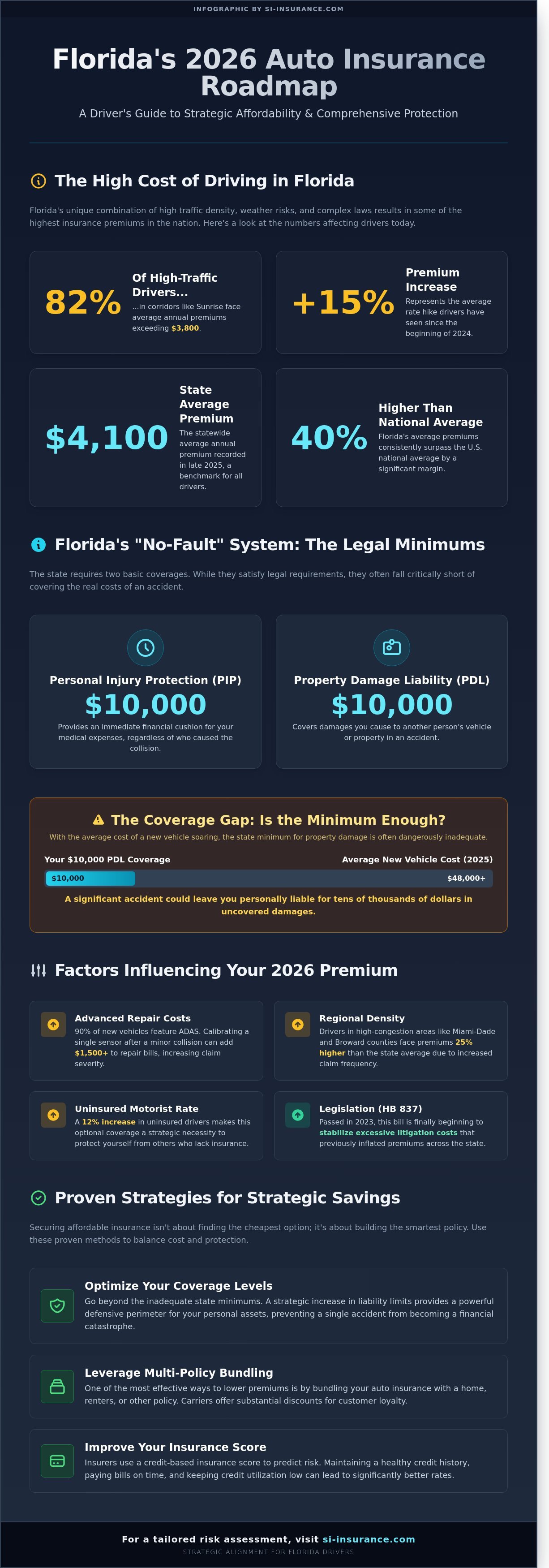

Did you know that 82% of drivers in high-traffic corridors like Sunrise are currently facing average annual premiums exceeding $3,800, which represents a 15% increase since January 2024? It's exhausting to feel like just another data point in a national carrier's algorithm while you struggle to decode the complex nuances of Personal Injury Protection (PIP) and Property Damage Liability (PDL) requirements. You've likely noticed that finding affordable auto insurance Florida isn't just about hunting for the lowest price; it's about finding a strategic balance between cost efficiency and absolute financial security.

I'm here to show you that you don't have to settle for generic, off-the-shelf policies that leave your assets vulnerable. We'll explore how to leverage specific risk mitigation techniques and strategic alignment to secure premium protection at the state's most competitive rates for 2026. This guide provides a clear roadmap through the current insurance environment, detailing how to optimize your coverage levers and build a lasting partnership with a local agent who provides the bespoke risk transfer solutions you actually need.

Key Takeaways

Gain a clear understanding of Florida’s 2026 insurance landscape and how the state's "No-Fault" system directly influences your monthly premiums.

Move beyond basic legal requirements to find the ideal balance of coverage that offers genuine protection without inflating your costs.

Learn proven methods for securing affordable auto insurance Florida by strategically leveraging multi-policy bundling and optimizing your credit-based insurance score.

Uncover the specific regional factors in Broward County that cause rates to fluctuate significantly between areas like Sunrise and Pompano Beach.

Discover how a tailored approach to risk management can provide you with the intellectual confidence and elite security your financial future deserves.

Table of Contents Understanding the Florida Auto Insurance Landscape in 2026 Decoding Coverage: What You Actually Need to Stay Protected Proven Strategies to Secure More Affordable Premiums Navigating Regional Rate Variations: Sunrise to Pompano Beach The SI Insurance Advantage: Strategic Alignment for Florida Drivers

Understanding the Florida Auto Insurance Landscape in 2026

Florida remains a distinct environment for motorists, where the intersection of high-density traffic and complex legal frameworks creates a premium structure that often exceeds the national average by 40 percent. As of 2026, the quest for affordable auto insurance Florida drivers seek requires a shift from passive shopping to active risk management. While the state average premium reached $4,100 annually in late 2025, finding value isn't about selecting the lowest number on a screen. It involves a calculated understanding of how regional risks and legislative mandates dictate your monthly costs.

Strategic affordability differs from "cheap coverage" because it prioritizes long-term financial stability over immediate, marginal savings. Selecting a policy with insufficient limits might reduce your monthly outflow by $25, but it leaves your personal assets exposed to catastrophic litigation. We view insurance as a bespoke risk transfer mechanism. By aligning your coverage with your actual exposure, you create a defensive perimeter that prevents a single accident from derailing your financial future. This approach requires a sophisticated look at the underlying mechanics of state law and the environmental factors that drive the numbers you see in a quote today.

The Mechanics of Florida No-Fault Insurance

Florida’s no-fault system acts as the foundational architecture of your insurance quote. At its core is Personal Injury Protection, or PIP, which provides an immediate $10,000 financial cushion for medical expenses regardless of who caused the collision. This ensures you receive prompt care without waiting for legal determinations. To see how these rules fit into the national landscape, Understanding the U.S. Auto Insurance System offers necessary context on these mandates. The state also requires $10,000 in Property Damage Liability, though this minimum rarely covers modern repair costs in a market where the average new vehicle price exceeded $48,000 in 2025.

Ensuring you have coverage for medical expenses is just one part of the equation; access to high-quality health products is also crucial for recovery. For a look at the types of medical supplies distributed internationally, you can click here.

Just as it's crucial to understand the mechanics of an insurance policy, the same principles of risk and maintenance apply to all forms of transportation. The complexity of modern vehicles is a major factor in repair costs, a trend that is magnified in the global shipping industry. For those interested in the engineering challenges of massive transportation systems, you can explore Mechanical Ship Repairs and see how these concepts apply on a much larger scale.

Why 2026 Rates Differ from Previous Years

The 2026 pricing models reflect a significant evolution from the volatility seen earlier in the decade. House Bill 837, passed in March 2023, has finally begun to stabilize the excessive litigation costs that previously inflated premiums. However, sophisticated technology in 90 percent of new vehicles has paradoxically increased repair expenses. Calibrating a single sensor after a minor fender bender now adds $1,500 to a standard bill. Regional density in South Florida and recent hurricane recovery costs also continue to influence the base rates seen in today’s quotes. These factors include:

High-density regions like Miami-Dade and Broward counties face 25 percent higher premiums than the state average due to increased claim frequency and congestion.

Weather-related risk assessments now incorporate the higher costs of parts and labor following the 2024 and 2025 hurricane seasons.

The 2026 market shows a 12 percent increase in uninsured motorist rates, making this optional coverage a strategic necessity for those seeking true financial security.

Advanced Driver Assistance Systems (ADAS) have reduced accident frequency by 15 percent, yet the severity of claims has risen due to the specialized labor required for repairs.

Securing affordable auto insurance Florida residents can rely on means looking past the initial price tag. It involves a steady, deliberate analysis of these variables. By understanding the legislative and technological shifts of the last three years, you can make an informed decision that balances cost with comprehensive protection. This level of foresight is what separates a standard policyholder from a strategically protected client.

Decoding Coverage: What You Actually Need to Stay Protected

Selecting the lowest legal limit often feels like a victory for your monthly budget, but it frequently leaves your personal assets exposed to catastrophic loss. True risk mitigation requires finding a strategic balance between premium costs and actual financial protection. While the Official Florida Insurance Requirements only mandate $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL), these figures are rarely sufficient to cover a multi-vehicle collision or a serious medical emergency. Finding affordable auto insurance Florida drivers can rely on means looking past these baseline numbers to secure a policy that functions as a genuine safety net.

Many drivers overlook the high stakes involved in Florida's traffic environment. According to 2021 data from the Insurance Research Council, approximately 20.4% of drivers in the state operate vehicles without any insurance at all. This makes Uninsured Motorist (UM) coverage a non-negotiable component of a sophisticated insurance portfolio. Without it, you're essentially betting your financial future on the responsibility of strangers. UM coverage ensures that if a hit-and-run occurs or an uninsured driver strikes you, your medical expenses and lost wages are covered by your own carrier.

Florida's unique environmental factors also dictate your needs for Comprehensive and Collision coverage. While Collision handles impacts with other vehicles, Comprehensive is vital for non-collision events like flood damage during hurricane season or windshield cracks from road debris. A single tropical storm can result in thousands of dollars in water damage; having a policy that accounts for these specific regional risks is a hallmark of underwriting excellence.

The "Must-Haves" vs. the "Nice-to-Haves"

Bodily Injury Liability (BIL) is technically optional under Florida's "no-fault" laws for most private passenger vehicles, yet it's strategically vital for protecting your home and savings from lawsuits. If you're financing a vehicle in high-traffic areas like Broward County, where 2023 traffic reports showed a high frequency of total-loss accidents, Gap Insurance is essential to cover the difference between your loan balance and the car's depreciated value. For daily commuters, Rental Reimbursement offers a practical solution to maintain mobility while your vehicle undergoes repairs, though it remains a secondary priority compared to liability limits.

Determining Your Ideal Deductible

The mathematical relationship between your deductible and your monthly premium is a direct lever for cost control. Increasing a deductible from $500 to $1,000 can reduce your collision and comprehensive premiums by as much as 15% to 30%, depending on your risk profile. You should only commit to a higher deductible if your emergency fund is liquid and ready to cover that amount on short notice. Choosing a higher deductible is a calculated decision to engage in a manageable level of self-insurance. If you're looking for a more tailored approach, exploring bespoke risk transfer options with a seasoned consultant can help align your coverage with your long-term financial goals. This ensures you maintain affordable auto insurance Florida without compromising your stability.

Proven Strategies to Secure More Affordable Premiums

Achieving affordable auto insurance Florida involves more than just a cursory search; it demands a strategic alignment of your personal risk profile with current market underwriting standards. While meeting Florida's minimum insurance requirements is the legal baseline, true financial security comes from optimizing your coverage through calculated adjustments. One of the most effective methods for risk mitigation is the multi-policy bundle. By consolidating your homeowners and automotive policies under a single carrier, you can often trigger premium reductions of 22% or more. This strategic move simplifies your financial management while signaling a higher degree of stability to the insurer's underwriting department.

Carriers in the Sunshine State frequently utilize credit-based insurance scores to determine the likelihood of future claims. Data from 2023 indicates that drivers with excellent credit pay approximately 50% less than those with poor credit scores for the same coverage levels. This isn't a reflection of driving ability but a statistical correlation between financial responsibility and risk. If your score is currently below 670, focusing on debt reduction can lead to a substantial decrease in your long-term insurance overhead. It's a slow process, but the results are measurable and permanent.

Modern drivers are increasingly turning to telematics as a tool for bespoke risk transfer. These "pay-how-you-drive" programs use mobile apps or plug-in devices to monitor braking habits, speed, and mileage. Safe drivers who consistently avoid late-night trips and hard braking events can see their premiums drop by as much as 30% after a 90-day evaluation period. This technology replaces generalized demographic data with your actual performance behind the wheel, ensuring your rates are earned rather than assigned based on local averages.

Finally, don't fall victim to the "Loyalty Tax." Many insurance companies use price optimization algorithms that gradually increase rates for long-term customers who are unlikely to switch. A 2024 market analysis showed that policyholders who shop for new quotes every 12 months save an average of $415 annually compared to those who remain with the same carrier for five years or more. Maintaining a disciplined schedule for market comparison ensures you're always positioned within the most competitive pricing tier available for affordable auto insurance Florida.

Maximizing Available Discounts

Individual lifestyle choices offer significant opportunities for premium reduction. Students maintaining a 3.0 GPA or higher can secure "Good Student" discounts that typically lower costs by 15%. Similarly, safe drivers who haven't filed a claim in 36 months often qualify for a 25% reduction. Florida residents who are active military or members of affinity groups like the Florida Bar or specific alumni associations should request an audit of available group rates. Installing a GPS-based anti-theft device can further refine your underwriting profile, often yielding a 5% to 10% credit on the comprehensive portion of your policy.

Managing Your Driving Record and Credit

A single at-fault accident in Florida can cause your premiums to spike by 42% on average. To mitigate this, completing a state-approved 6-hour defensive driving course can provide a 10% discount that remains valid for three years. Strategic focus on your credit health is equally vital. Moving your credit score up by just 100 points can result in an 18% savings on your annual premium. These proactive steps demonstrate to the carrier that you're an elite risk, allowing you to bypass the high-cost pools reserved for less disciplined drivers.

Navigating Regional Rate Variations: Sunrise to Pompano Beach

Your residential zip code acts as a primary lever in determining your premium, often carrying more weight than your driving history itself. In Broward County, the short 15 mile trek from the quiet suburbs of Sunrise to the bustling coastal streets of Pompano Beach represents a massive shift in how underwriters view your risk. If you are searching for affordable auto insurance Florida drivers can actually fit into a monthly budget, you have to look at the micro-climates of risk that define South Florida.

The Broward County Driving Factor

Traffic density is the most immediate driver of these regional rate hikes. Data from the Florida Department of Transportation shows that certain stretches of I-95 near Pompano Beach handle over 250,000 vehicles daily. This extreme volume creates a statistical certainty of minor collisions and multi-car pileups. Conversely, Sunrise residents often rely on the Sawgrass Expressway. While tolls are a factor, the lower density of commercial freight on the Sawgrass typically results in a 12% lower frequency of liability claims compared to the coastal corridors.

Commute Risk: Pompano’s proximity to the US-1 and I-95 interchange increases the probability of "fender benders" by nearly 18% over quieter Sunrise neighborhoods.

Comprehensive Costs: Local crime statistics influence your rates too. Pompano Beach has historically recorded property crime rates near 35 per 1,000 residents, which forces insurers to price comprehensive coverage higher to account for theft and vandalism.

The Human Touch: A local office in Sunrise offers a white-glove service that a digital bot can't match. We understand that a resident in a gated community in Weston has a different risk profile than someone parking on the street in a high-traffic urban center.

Why Local Expertise Matters

National call centers use broad algorithms that often penalize all Florida drivers for the state's general litigation climate. However, Si Insurance Agency functions as a strategic guardian by navigating regional carriers that national aggregators often ignore. These Florida-specific insurers frequently offer more competitive rates because they possess a granular understanding of Broward County’s drainage systems, hurricane evacuation routes, and local repair costs.

When you work with a local expert, your risk assessment is bespoke rather than off-the-shelf. We don't just look at your age and car model; we look at your specific Florida lifestyle. This might include how often you drive during peak tourist season or whether your vehicle is stored in a reinforced garage during the June to November hurricane window. These small details can lead to significant underwriting excellence and lower costs. Finding affordable auto insurance Florida residents trust is about precision, not just luck.

The value of this sophisticated approach becomes most apparent during the claims process. Instead of waiting in a queue for a representative in a different time zone, you have a partner who knows the local body shops and legal landscape. This ensures your claim is handled with the meticulous attention to detail that your assets deserve. We focus on long-term protection and strategic alignment with your financial goals.

Secure your assets with a policy tailored to your specific South Florida zip code. Contact Si Insurance Agency today for a professional risk assessment.

The SI Insurance Advantage: Strategic Alignment for Florida Drivers

You've likely spent the last few days navigating the chaotic landscape of premium increases and shifting coverage mandates. It's a draining process that often leaves drivers feeling like a mere data point in a vast, impersonal database. At SI Insurance, we intentionally pivot away from that retail mindset. We don't view insurance as a commodity to be traded; we see it as a critical component of your broader financial security. Our role is to act as your strategic guardian, moving you from the status of an exhausted shopper to a fully protected client who understands exactly where every dollar of their premium is going.

The transition to working with an elite consultant provides a sense of intellectual confidence that standard search engines simply can't offer. We focus on strategic alignment, ensuring that your policy isn't just a legal requirement but a bespoke shield tailored to your specific life stage and asset profile. Finding affordable auto insurance Florida residents can actually trust requires a level of foresight and meticulous planning that we've refined through years of industry experience. We take the burden of risk mitigation off your shoulders, allowing you to focus on your daily life with the assurance that your coverage is engineered for maximum efficacy.

Our Approach to Underwriting Excellence

Our firm launched in 2022 with a clear mission to modernize how risk is analyzed in the Sunshine State. We recognized that legacy agencies were often stuck using outdated models that didn't account for the unique economic shifts of the last three years. By leveraging our network of 35 distinct insurance carriers, we're able to find the precise strategic fit for your unique driving profile. We don't settle for the first quote that meets the minimum legal standards; instead, we conduct a rigorous 48-point policy review for every client to identify hidden gaps in coverage.

This commitment to underwriting excellence means we look at your situation through a lens of modern financial engineering. We analyze factors that traditional agents ignore, such as how your specific vehicle safety tech or your remote work status might lower your risk profile. This 2022 perspective allows us to bypass the inefficiencies that keep costs high for no reason. Our goal is to provide a high-value solution that balances cost-efficiency with comprehensive protection, ensuring that your affordable auto insurance Florida strategy is both lean and robust.

Securing Your Quote Today

We've designed our intake process to be as seamless as it is deep. While our online portal offers a quick baseline for those who want immediate numbers, the true SI Insurance advantage is found in our personalized consultations. These sessions allow us to dig into the nuances of your liability needs and explain the "why" behind your rates. It's a white-glove service that treats your time with the respect it deserves, moving at a pace that is deliberate yet efficient.

To ensure we can provide the most accurate and competitive quote, it helps to have your 17-digit VIN and a five-year driving history report ready for our review. This specific data allows our team to apply every available discount and strategic adjustment from the start. We've seen clients reduce their unnecessary coverage overlaps by as much as 22% simply by having our experts audit their existing documents. It's time to stop settling for off-the-shelf policies that don't fit your life. Connect with a Si Insurance expert today and experience the clarity that comes with a professionally managed risk strategy.

Securing Your Strategic Edge on Florida’s Roads in 2026

Navigating the evolving 2026 insurance landscape requires more than just a standard policy; it demands a calculated approach to risk. By analyzing how regional rate shifts impact drivers from Sunrise to Pompano Beach, you've already taken the first step toward true optimization. Finding affordable auto insurance Florida drivers can actually trust isn't about seeking the lowest price at the expense of safety. Instead, it's about securing a strategic alignment with A-rated carriers that recognize your specific risk profile. Our team at SI Insurance brings over 20 years of South Florida expertise to help you identify these specific opportunities.

We don't believe in off-the-shelf coverage. As an independent agency with access to more than 25 elite carriers, we provide bespoke risk management tailored to high-value needs. Whether you're protecting a luxury fleet or a single high-end vehicle in Broward County, our focus remains on underwriting excellence and long-term financial stability. You've done the hard work of researching your options, and now it's time to put those insights into practice with a partner who values precision as much as you do.

Request Your Strategic Auto Insurance Review from Si Insurance today. We're ready to help you drive with total confidence.

Frequently Asked Questions

Is Florida a no-fault state for auto insurance in 2026?

Yes, Florida remains a no-fault state through 2026 under the current Florida Motor Vehicle No-Fault Law. This mandate requires you to carry Personal Injury Protection to cover your own medical expenses after a collision, regardless of who's at fault. This strategic framework aims to minimize legal delays; however, it directly impacts the availability of affordable auto insurance Florida residents seek for basic protection.

What is the minimum car insurance required in Florida?

Florida law requires a minimum of $10,000 in Personal Injury Protection and $10,000 in Property Damage Liability. You'll need to provide proof of this coverage to the Florida Department of Highway Safety and Motor Vehicles to maintain a valid vehicle registration. While these are the legal minimums, many drivers choose higher limits to ensure more robust risk mitigation against personal asset loss in 2024.

How much does car insurance cost per month in Florida on average?

Florida drivers pay an average of $250 per month for full coverage as of early 2024. If you're only looking for the state-mandated minimums, that cost typically drops to around $92 monthly. It's important to remember that rates in high-traffic areas like Miami or Tampa can be 20 percent higher than the state average due to increased claim frequencies in those urban centers.

Can I get affordable auto insurance with a recent accident on my record?

You can still secure affordable auto insurance Florida rates after an accident by targeting carriers that specialize in non-standard risk profiles. Typically, a single at-fault accident increases premiums by 32 percent in the Florida market. We recommend maintaining a clean record for 36 consecutive months, as many insurers offer significant safe driver discounts once that three-year threshold passes without further incidents.

Why did my Florida car insurance premium go up if I had no accidents?

Your premium might increase because Florida insurance rates rose by an average of 14 percent in 2023 due to systemic market factors. Rising costs for vehicle parts and a 10 percent uptick in litigation expenses across the state force insurers to adjust their pricing models. Even with a perfect record, you're part of a collective risk pool that's influenced by regional trends and inflation.

What is the best way to compare auto insurance quotes in Sunrise, FL?

The most effective way to compare quotes in Sunrise is to work with an independent agent who can access at least 15 different carriers. Since Sunrise drivers often face higher rates due to traffic on I-75, a bespoke risk transfer analysis is vital. We recommend reviewing your options every 12 months to ensure your policy stays aligned with current market pricing and your personal safety record.

Does Florida require bodily injury liability coverage?

Florida law doesn't require bodily injury liability for most standard drivers, but it's a critical component for strategic risk mitigation. If you've had a DUI, the state's FR-44 law mandates limits of $100,000 per person and $300,000 per accident. Without this coverage, you're personally responsible for the medical costs of others if you're found liable in a serious 2024 traffic incident.

How does bundling home and auto insurance work in South Florida?

Bundling works by placing both your homeowners and auto policies with a single carrier to trigger a multi-policy discount, which averages 12 percent in South Florida. This strategic alignment simplifies your financial management and creates a more cohesive risk management portfolio. Given the volatility of the Florida property market, bundling can also provide more stability in your overall insurance relationships throughout 2025.

Comments