Car Insurance for Teens in Florida: A Strategic Guide for 2026

- siinsuranceflorida

- 1 day ago

- 12 min read

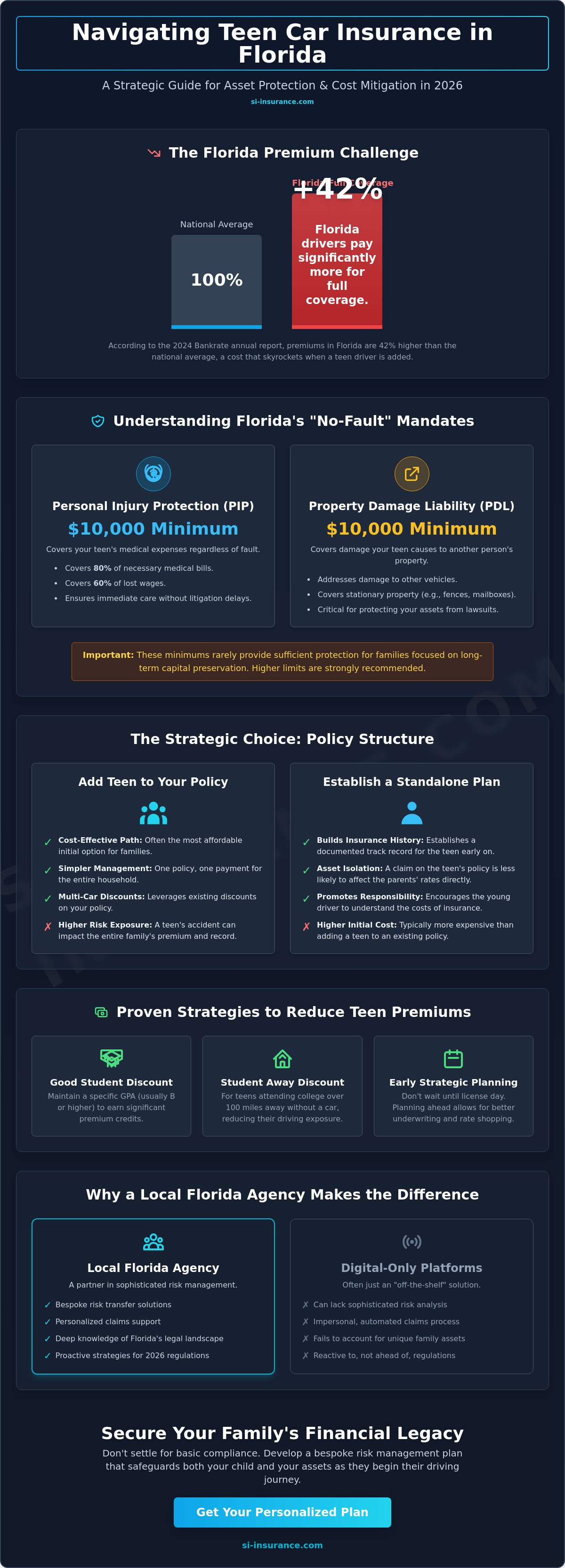

According to the 2024 Bankrate annual report, Florida drivers pay 42% more for full coverage than the national average, a figure that escalates significantly when a young driver enters the household. Securing car insurance for teens in Florida often feels like an exercise in managing inevitable sticker shock while grappling with the intricacies of the state's No-Fault statutes. You're likely concerned that the mandatory Personal Injury Protection (PIP) limits won't offer sufficient protection in a high-risk legal environment. It's a valid anxiety for any parent focused on long-term capital preservation and risk mitigation.

This guide provides a clear roadmap to align your family's risk profile with elite coverage options that don't compromise your broader financial strategy. We'll examine the specific mechanics of Florida's liability requirements and identify the underwriting criteria that lead to maximum premium credits for 2026. You'll gain the intellectual confidence to move beyond basic compliance toward a bespoke risk management plan that safeguards both your child and your assets.

Key Takeaways

Gain a clear understanding of Florida’s mandatory coverage requirements, specifically how Personal Injury Protection (PIP) serves as the critical foundation for your teen's policy.

Compare the long-term financial outcomes of adding a driver to your current policy versus establishing a standalone plan to find the most efficient path for car insurance for teens in Florida.

Identify high-value premium credits, including "Good Student" and "Student Away" discounts, that allow you to mitigate costs while maintaining elite protection standards.

Explore why a local Florida agency offers the sophisticated risk management and personalized claims support that digital-only platforms often lack.

Master a strategic framework for the 2026 regulatory environment that ensures your family’s financial legacy remains secure as your teen begins their driving journey.

Table of Contents Navigating the Complexity of Teen Car Insurance in Florida Understanding Florida’s Unique Insurance Mandates for Young Drivers The Strategic Choice: Adding a Teen to Your Policy vs. a Standalone Plan Proven Strategies to Mitigate the Cost of Florida Teen Premiums Why Partnering with a Local Florida Agency Makes the Difference

Navigating the Complexity of Teen Car Insurance in Florida

Securing car insurance for teens in Florida isn't a simple administrative task; it's a sophisticated exercise in high-stakes asset protection. Florida consistently ranks as one of the most expensive regions for motorists in the country. In 2024, data from industry reports indicated that Florida premiums were nearly 50% higher than the national average. As we approach the 2026 regulatory cycle, the landscape has become increasingly intricate. This environment demands that parents evolve from being the primary operator to acting as a strategic guardian of a new motorist. Relying on an "off-the-shelf" policy often fails because these products don't account for the specific risk variables found on Florida's congested corridors. Navigating the Complexity of Teen Car Insurance requires a deep understanding of how state-specific mandates interact with the higher frequency of claims associated with young drivers.

To better understand how these costs are managed and how you can reduce your financial exposure, please review the following analysis:

The "No-Fault" Factor: How Florida Law Impacts Teens

Florida’s no-fault status fundamentally alters the liability landscape for inexperienced drivers. Under this system, each party's insurance covers their own medical expenses regardless of who caused the accident. Personal Injury Protection (PIP) serves as the primary mechanism for initial medical coverage, ensuring immediate care without the delays of litigation. For a young driver, this means their medical costs are addressed quickly, but it also places a heavy burden on the family policy. Within the Florida household, the $10,000 PIP limit provides mandatory medical and disability benefits to all resident relatives, including teen drivers, after a motor vehicle incident.

Why Early Strategic Planning Saves Thousands

Procrastination in this area usually leads to significant capital leakage. Waiting until the moment a teen receives their license to modify a policy removes the opportunity for proper underwriting excellence. Establishing a documented insurance track record for your teen functions as a long-term wealth strategy. It builds a profile of reliability that generates measurable savings as they age. SI Insurance focuses on bespoke risk transfer solutions that treat the young adult as a distinct risk entity rather than a simple policy addition. This methodical approach ensures that car insurance for teens in Florida becomes a stable, well-managed component of your family’s broader financial protection plan. By aligning coverage with the actual risk profile of the teen, parents can mitigate the volatility of annual premium hikes.

Understanding Florida’s Unique Insurance Mandates for Young Drivers

Securing car insurance for teens in Florida requires a sophisticated understanding of the state’s rigorous and often counterintuitive regulatory framework. Unlike many other jurisdictions, Florida operates under a no-fault system, which places the primary financial burden of initial medical recovery on the policyholder’s own insurer. To maintain compliance with Florida’s Unique Insurance Mandates, every driver must carry a minimum of $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL). While these figures represent the legal baseline, they rarely provide the comprehensive risk mitigation required for high-value households.

PIP serves as the cornerstone of Florida’s insurance philosophy. It's designed to cover 80 percent of necessary medical expenses and 60 percent of lost wages, regardless of who caused the accident. PDL, conversely, addresses the damage your teen might cause to another person’s vehicle or stationary property. While these mandates satisfy the Florida Department of Highway Safety and Motor Vehicles (FLHSMV), they leave a glaring void: Bodily Injury Liability (BIL). Although BIL isn't a universal requirement for all drivers, it's a strategic necessity for families with significant assets, as it protects against lawsuits arising from severe accidents.

Minimum Requirements vs. Strategic Protection

Opting for "state minimums" is a precarious gamble for families in Broward County. A standard 10/20/10 policy, which provides $10,000 for one person’s injuries, $20,000 per accident, and $10,000 for property damage, is often exhausted within minutes of a serious collision. In high-traffic corridors near Sunrise and Pompano Beach, the density of luxury vehicles and the frequency of multi-car incidents make Uninsured Motorist (UM) coverage an essential component of a bespoke risk management plan. Without UM, you're essentially relying on the financial responsibility of other drivers, a variable that's impossible to control.

The Role of the Florida Financial Responsibility Law

The state maintains a digital ledger that links every 11-digit driver license number to an active insurance policy. Under the Florida Financial Responsibility Law, any lapse in coverage triggers an automated notification to the FLHSMV, which can lead to an immediate suspension of driving privileges. For new residents, the requirements are strict. You've got 30 days to register your vehicle and secure Florida-specific coverage after establishing residency or starting employment. This meticulous documentation ensures that your teen’s transition to Florida’s roads remains legally seamless and strategically sound.

The Strategic Choice: Adding a Teen to Your Policy vs. a Standalone Plan

Deciding how to structure car insurance for teens in Florida involves more than just comparing monthly premiums; it's an exercise in long-term risk positioning. You generally face two paths: absorbing the teen into your current household policy or establishing a separate, standalone account. For the vast majority of Florida families in 2026, the household integration remains the superior financial move. This allows you to leverage a multi-car discount that can reduce the teen's portion of the premium by as much as 25% compared to a solo plan. It's a matter of logic and scale. The more vehicles you bring to a single carrier, the more leverage you have in negotiations.

Benefits of the Household Policy Integration

When you add a young driver to your existing framework, you're essentially lending them your insurance reputation. Florida carriers rely heavily on credit-based insurance scores and years of clean driving history to determine rates. By keeping the teen on your policy, you're utilizing your established credit to anchor their high-risk profile. This creates a more stable pricing environment. You can find more details on how these variables interact in our Florida Auto Insurance: A Strategic Guide to Coverage in 2026. Managing a single set of limits and deductibles also simplifies the administrative burden. You can find Proven Strategies to Mitigate the Cost through the Insurance Information Institute, which highlights how bundling remains the most effective tool for families. The choice of vehicle is equally vital. Assigning a teen to a vehicle with a high safety rating, rather than a luxury or performance model, allows the policy to reflect a lower risk tier across the entire household fleet.

When to Consider a Bespoke Standalone Policy

Standalone policies serve as a tactical barrier. High-net-worth families often use this method to create a liability silo. By separating the teen's coverage, you protect your primary assets from being targeted in a lawsuit if the teen is involved in a severe accident. It's a calculated trade-off. You pay more in premiums to gain a higher level of asset protection. In Florida, if the vehicle title is in the teen's name alone, a standalone policy is usually a legal requirement. You should also be wary of the "excluded driver" status. While it might seem like a way to save money on a specific vehicle, it's often a tactical error. This leaves your family exposed to massive out-of-pocket costs if the teen ever operates that car in an emergency. The math is clear. You must align your insurance structure with your actual driving habits and asset protection needs, ensuring that car insurance for teens in Florida serves as a robust shield rather than a financial drain.

Proven Strategies to Mitigate the Cost of Florida Teen Premiums

Managing the financial exposure associated with car insurance for teens in Florida requires a series of deliberate, data-driven decisions. High premiums aren't an inevitability; they're a starting point for optimization. We recommend a framework that prioritizes behavioral incentives and technical policy adjustments to secure the lowest possible risk profile for your household. This approach focuses on the intersection of driver behavior and policy architecture.

Vehicle selection acts as the foundation of this strategy. Insurers in 2026 utilize sophisticated actuarial models that penalize high-performance engines and reward advanced safety suites. Choosing a vehicle with a four-cylinder engine and a Top Safety Pick+ rating from the Insurance Institute for Highway Safety (IIHS) can lower base rates by 12% compared to standard models. Telematics programs have also reached a new level of precision. By opting into "Drive Safe & Save" style initiatives, families allow insurers to monitor real-time metrics like hard braking and cornering speeds, often resulting in immediate 10% enrollment discounts and up to 30% performance-based savings over time.

Academic and Training Incentives

Carriers reward academic discipline because statistical data links classroom performance to lower accident frequency. In Florida, students must typically provide a transcript showing they're in the top 20% of their class or maintain a specific grade average. By maintaining a minimum 3.0 GPA, a student demonstrates the level of responsibility that insurers reward with premium reductions of up to 25%. Beyond grades, completing a certified driver education course through the Florida Safety Council or approved Broward County public school programs provides a permanent credit on the policy. If your teen attends a university more than 100 miles from home without a vehicle, the "Student Away at School" credit can slash premiums by an additional 15% to 20%.

Tactical Deductible and Coverage Adjustments

Adjusting the structure of the policy itself offers immediate cash flow relief. Increasing a collision deductible from $500 to $1,000 can reduce that specific premium component by nearly 30% in high-traffic areas like Miami or Fort Lauderdale. For older "starter" vehicles valued at less than $4,000, it's often mathematically sound to drop collision and comprehensive coverage entirely, as the annual premium plus the deductible may exceed the total payout in a total-loss scenario. Strategic alignment of your insurance portfolio also yields results. You can achieve significant multi-policy discounts by integrating your auto policy with your Home Insurance in Florida, centralizing your risk management under a single, sophisticated umbrella.

Effective risk transfer is about more than just finding a low number; it's about building a sustainable financial shield. To explore a bespoke coverage plan for your family, consult with an SI Insurance advisor today.

Why Partnering with a Local Florida Agency Makes the Difference

Digital-only carriers often prioritize transaction speed over policy substance. While an app might offer a quick interface, it frequently lacks the depth needed to handle the volatility of the Florida insurance market. In a state where litigation and complex "No-Fault" laws create a high-stakes environment, relying on an algorithm to manage car insurance for teens in Florida leaves families exposed to significant financial gaps. Si Insurance Agency functions as a strategic guardian, providing a level of foresight that automated systems cannot replicate. We replace the frustration of automated call centers with a composed, professional partnership focused on long-term risk mitigation.

Our approach centers on "white-glove" service, ensuring that every policy is a product of rigorous analysis rather than a generic template. When a claim occurs, the value of a human advocate becomes undeniable. We provide the intellectual confidence parents need, acting as a calm and calculated intermediary between your family and the carrier. This ensures that your teen's coverage isn't just a monthly expense, but a meticulously engineered shield designed for the 2026 regulatory environment.

Bespoke Solutions for Broward County Residents

Residents in Pompano Beach and Sunrise face unique driving challenges that require localized expertise. Broward County reported 41,378 traffic crashes in 2023 according to FLHSMV data; a statistic that underscores the necessity of a sophisticated risk strategy. We understand the specific traffic patterns of the I-95 corridor and the high-density risks associated with South Florida's urban centers. Our team utilizes a network of carriers that specialize in these Florida-specific risks, offering bespoke solutions that align with your family's high-value assets. Having a partner who understands the local landscape ensures that your strategy is grounded in reality, not just probability.

Securing Your Quote with Intellectual Confidence

The process of obtaining a quote should be an exercise in strategic alignment. Our elite consultants perform a professional risk assessment that goes beyond basic demographic data. We examine your family's total risk profile to ensure that every aspect of the policy serves a specific purpose in your broader financial plan. We meticulously compare rates and coverage terms from top-tier carriers to find the precise balance of protection and value you deserve. This methodical transition from education to execution is what defines our commitment to underwriting excellence. Experience the professional difference with Si Insurance Agency and secure a future defined by stability and strategic protection.

Securing Your Family’s Financial Future on Florida Roads

Managing the nuances of risk mitigation for young drivers requires more than just a basic policy; it demands a calculated approach to Florida Statute 627.736 and the specific Personal Injury Protection mandates that govern our state. We've explored how strategic alignment with an independent agency allows you to compare elite carriers rather than being restricted to a single captive solution. Since 2022, SI Insurance has served the Broward County community by providing this exact level of underwriting excellence. It's about finding that perfect balance between comprehensive protection and fiscal responsibility.

Securing competitive car insurance for teens in Florida is a complex process, but it's manageable with the right foresight. By weighing the benefits of adding a driver to an existing policy against the independence of a bespoke plan, you're protecting your household's long-term assets. Our team leverages deep technical mastery of the 2026 insurance landscape to ensure your coverage is as rigorous as it is reliable. You don't have to navigate these intricate mandates alone.

You've got the tools to make an informed choice that keeps your teen safe and your budget intact.

Frequently Asked Questions

Is it mandatory to add my teenager to my Florida car insurance policy as soon as they get their permit?

Most Florida insurers don't require you to formally add a teenager to your policy until they receive their provisional driver's license. While they hold a learner's permit, they're typically covered under your existing liability limits at no extra cost. You should still notify your agent to ensure strategic alignment with your carrier's specific underwriting guidelines, as 15 percent of Florida carriers have unique reporting requirements.

How much does the average car insurance premium increase when adding a teen in Florida?

Adding a 16-year-old driver to a Florida policy results in an average premium increase of 152 percent according to 2024 Quadrant Information Services data. This surge reflects the heightened risk profile associated with inexperienced operators in high-traffic corridors like Miami or Orlando. Implementing strategic risk mitigation through high-deductible plans can help manage these elevated costs while maintaining comprehensive asset protection for your family's wealth.

What happens if my teen driver is involved in an accident and I haven’t added them to my policy?

If an unlisted teen driver causes an accident, your insurer will likely deny the claim and may rescind the policy for material misrepresentation. This creates a massive financial liability, as Florida's No-Fault laws require immediate Personal Injury Protection coverage. Failing to disclose a licensed household resident is a breach of the insurance contract that 90 percent of Florida carriers treat as a non-disclosed risk that voids coverage.

Can my teen get their own insurance policy in Florida if they are under 18?

Minors under age 18 can't legally enter into a binding insurance contract in Florida without a parent or guardian as a co-signer. It's rarely a strategic choice because standalone policies for young drivers often cost 25 percent more than remaining on a family plan. Maintaining a unified policy allows for better risk transfer and access to multi-car discounts that individual policies lack, providing a more stable financial foundation.

Does Florida offer any specific state-sponsored discounts for young drivers who complete safety programs?

Florida doesn't offer a direct state-funded discount, but Florida Statute 627.06501 requires insurers to provide premium credits for students who complete an approved driver improvement course. Completing a 4-hour Traffic Law and Substance Abuse Education program is a baseline requirement. Strategic families also utilize the Florida Smart Driver initiative to secure an additional 10 to 15 percent reduction in annual premiums through verified safety education.

What is the most cost-effective car for a teenager to drive in Florida from an insurance perspective?

The most cost-effective vehicles for car insurance for teens in Florida are typically mid-sized sedans like the Honda Accord or Toyota Camry from the 2018 to 2022 model years. These vehicles feature high Insurance Institute for Highway Safety ratings, which lowers the underwriting risk significantly. Avoiding high-performance engines or luxury badges is a critical component of a bespoke risk management strategy to keep your annual premiums manageable.

How long does a teen driver have to stay on their parents’ insurance policy?

There's no legal age limit for how long a child can stay on your policy as long as their primary residence remains your household. Many Florida residents keep their adult children on the family plan through age 26 to capitalize on loyalty discounts and bundled rates. This approach ensures a consistent risk mitigation framework until the driver establishes their own independent household and a mature financial profile.

Will my Florida insurance rates go down automatically once my teen turns 25?

Rates don't drop automatically on a driver's 25th birthday, though most Florida insurers re-evaluate the risk tier during the next renewal cycle. Data from the National Association of Insurance Commissioners shows that premiums for car insurance for teens in Florida begin to stabilize significantly after 9 years of clean driving history. You'll need to proactively contact your advisor to ensure your policy reflects this strategic shift in the risk profile.