Full Coverage Car Insurance Cost in Florida: A Strategic Analysis for 2026

- siinsuranceflorida

- 2 days ago

- 12 min read

Did you know that according to a 2024 MarketWatch analysis, Florida drivers pay roughly 55% more for auto insurance than the national average? You’ve likely noticed your own premiums climbing year after year, and it’s frustrating to feel like you’re paying more for less clarity. In a no-fault state like ours, the term "full coverage" often creates more confusion than security, especially when you’re trying to protect high-value assets in a litigious environment. Finding the right balance between cost and comprehensive protection requires a more sophisticated approach than a standard off-the-shelf policy.

This strategic analysis clarifies the full coverage car insurance cost Florida residents can expect as we move toward 2026. We’ll show you how to structure your policy for maximum efficiency and absolute security. By the end of this guide, you’ll understand the specific market drivers and the bespoke risk mitigation strategies that ensure your protection remains airtight without any unnecessary financial fluff. We’re going to examine the precise factors that influence your rates so you can move forward with total intellectual confidence in your coverage.

Key Takeaways

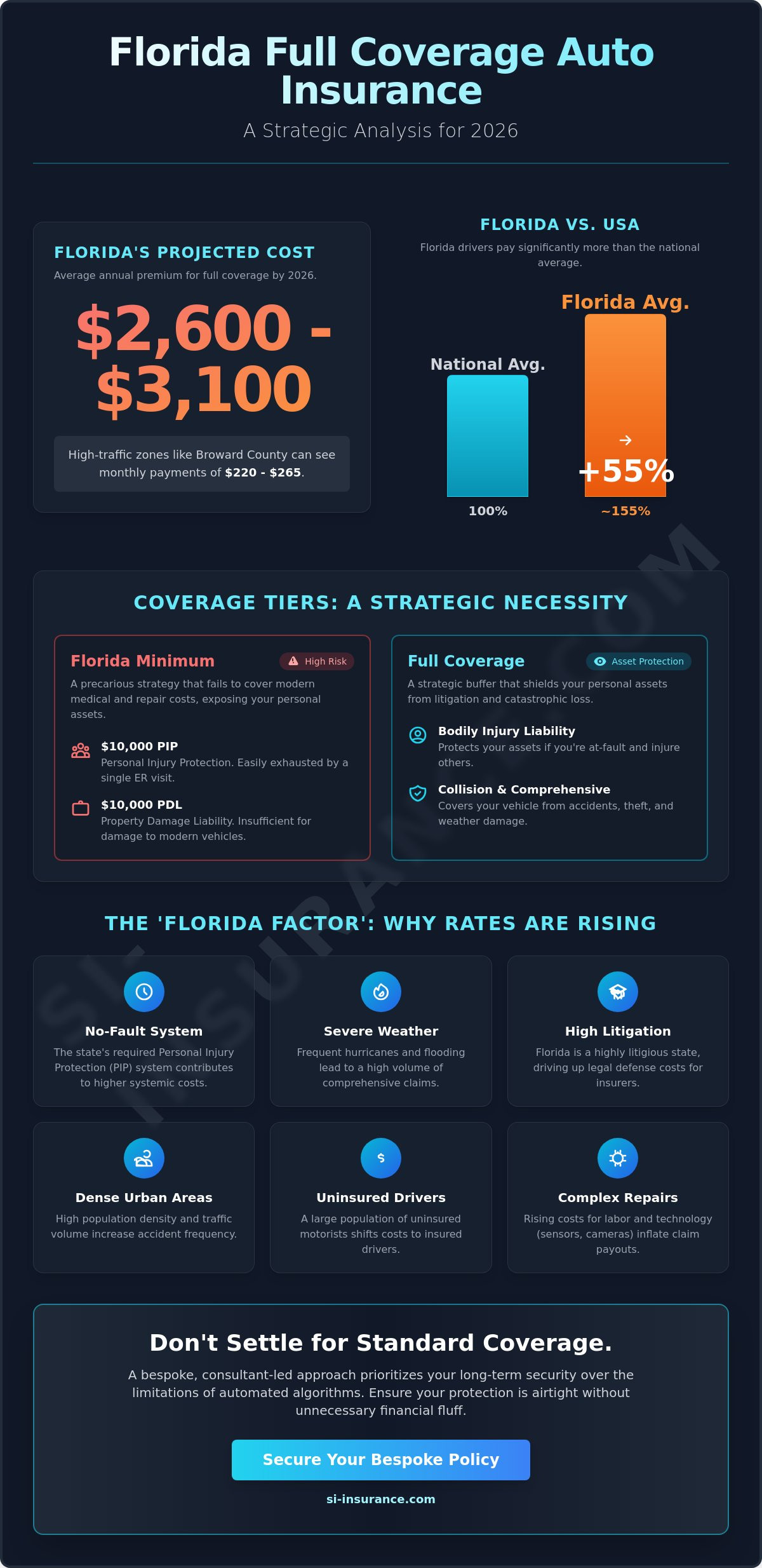

Gain clarity on the current market landscape where the average full coverage car insurance cost Florida drivers encounter is projected to reach $2,600 to $3,100 by 2026.

Identify the specific regional drivers, including the state’s unique no-fault system and climate-related risks, that are fundamentally reshaping premium structures.

Evaluate how critical personal variables, such as credit-based insurance scores and vehicle repair complexity, directly impact your strategic risk profile.

Discover actionable methods to mitigate rising costs through calculated deductible adjustments and the strategic advantages of multi-policy bundling.

Explore the benefits of a bespoke, consultant-led approach that prioritizes long-term security over the limitations of standard automated insurance algorithms.

Table of Contents Understanding the Average Cost of Full Coverage in Florida for 2026 Deconstructing the 'Florida Factor': Why Rates Are Rising Critical Variables Influencing Your Strategic Insurance Premiums Proven Strategies for Risk Mitigation and Premium Reduction Why a Bespoke Approach with SI Insurance Agency Secures Your Future

Understanding the Average Cost of Full Coverage in Florida for 2026

Florida's insurance environment in 2026 requires a high level of financial foresight. When we discuss the full coverage car insurance cost Florida drivers face, we're looking at a comprehensive suite of protections including liability, collision, and comprehensive coverage. For the 2026 fiscal year, actuarial data indicates the average annual premium has stabilized between $2,600 and $3,100. This figure reflects the state’s unique risk profile, which is characterized by high litigation rates and frequent severe weather events. Understanding vehicle insurance is the first step in recognizing why these costs are significantly higher than the national average. Florida consistently ranks as a top three most expensive state for automotive protection because of the convergence of high-density urban areas and a large population of uninsured motorists.

To better understand how these costs are structured and why the cheapest options might fail you, watch this helpful video:

The Monthly Breakdown: What to Expect

Drivers in high-traffic zones like Broward County can expect monthly payments between $220 and $265 for clean records. These figures have increased by 8% since 2025 due to a 12% rise in specialized labor costs for modern vehicle sensors and safety tech. We define the average monthly cost as a direct reflection of localized risk and administrative overhead. At SI Insurance, we view these premiums as a necessary allocation for risk mitigation rather than a simple monthly bill. The complexity of 2026 vehicle repairs means that even minor fender benders now involve expensive recalibrations of onboard computers.

Full Coverage vs. Florida Minimum Requirements

Relying on Florida's legal minimums is a precarious strategy. The state only mandates $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL). This $10,000 threshold hasn't kept pace with medical inflation; a single emergency room visit in 2026 can easily exceed this limit. While the full coverage car insurance cost Florida residents pay is higher, it offers a strategic benchmark that includes:

Bodily Injury Liability: Protects your assets if you're found at fault in an accident that injures others.

Collision Coverage: Pays for damage to your own vehicle regardless of fault.

Comprehensive Coverage: Shields you from non-collision events like hurricane damage or theft.

We recommend balancing the higher premium cost against the catastrophic risk of personal litigation. Choosing full coverage provides a strategic buffer that protects personal assets from being seized in the event of a high-value claim. It's a calculated move that prioritizes long-term stability over short-term savings.

Deconstructing the 'Florida Factor': Why Rates Are Rising

Florida's insurance environment is defined by a convergence of statutory mandates and volatile geographic realities. Understanding why the full coverage car insurance cost Florida residents face is consistently among the highest in the country requires an analysis of the state's unique regulatory architecture. While national trends play a role, the local landscape is shaped by specific legal frameworks and environmental hazards that demand a more sophisticated approach to risk management. It's not just about the volume of drivers; it's about the systemic costs baked into every policy issued in the Sunshine State.

The No-Fault System and PIP Complexity

Florida operates under a no-fault insurance model, requiring all drivers to carry $10,000 in Personal Injury Protection (PIP). This coverage acts as the first line of defense, intended to provide immediate medical relief regardless of who caused the accident. However, this system often leads to higher premium structures because it doesn't effectively prevent litigation once medical costs exceed the PIP threshold. Strategic policyholders recognize that PIP alone is insufficient for true security. In a state where approximately 20% of motorists operate without any insurance, adding Uninsured Motorist (UM) coverage is a strategic necessity for long-term asset protection. For a deeper dive into these requirements, consult our Florida Auto Insurance: A Strategic Guide to Coverage in 2026.

Environmental and Geographical Risks

Geography dictates premium outcomes with clinical precision. Coastal municipalities like Pompano Beach and Sunrise experience elevated comprehensive rates due to their inherent vulnerability to storm surges and high-velocity wind events. The Insurance Information Institute highlights several factors influencing insurance premiums, including the high frequency of flood-related total loss claims in these specific regions. Beyond weather, the extreme vehicle density in South Florida creates a higher statistical probability of multi-car collisions. SI Insurance Agency utilizes granular zip code data to evaluate these micro-risks, ensuring that full coverage car insurance cost Florida calculations reflect actual exposure rather than broad regional averages.

Legal and litigation trends also exert heavy upward pressure on premiums. Florida has historically seen high volumes of "bad faith" litigation and glass replacement fraud, which forces carriers to adjust their underwriting excellence standards to maintain solvency. These systemic costs are distributed across the entire pool of policyholders, regardless of individual driving records. By working with a consultant to implement bespoke risk transfer strategies, you can better manage these rising costs while maintaining an elite level of protection for your vehicles and personal liability.

Critical Variables Influencing Your Strategic Insurance Premiums

Florida's insurance market operates on a foundation of predictive analytics. Carriers don't just look at your car; they look at your financial footprint. Your credit-based insurance score serves as a vital metric in this calculation. In Florida, the spread between a "poor" and "excellent" credit rating can result in a premium difference of nearly $1,500 annually. This isn't an arbitrary penalty. Actuarial data consistently demonstrates that individuals who manage their credit with precision are statistically less likely to file high-value claims. By maintaining a high score, you signal a level of risk mitigation that underwriters reward with more favorable terms.

Your driving history is perhaps the most direct influence on your financial profile. A single at-fault incident in Florida isn't a temporary setback. It's a multi-year financial commitment. Industry reports indicate that a single accident can inflate your full coverage car insurance cost Florida by 42% or more for a period of three to five years. This makes defensive driving a fiscal strategy as much as a safety measure. For seasoned professionals, this history acts as a protective shield, but for those with recent infractions, the path to premium recovery requires time and documented stability.

Vehicle Type and Technology Costs

Modern automotive engineering presents a paradox for insurance premiums. While Advanced Driver Assistance Systems (ADAS) reduce accident frequency, the cost to recalibrate sensors after a minor collision often exceeds $3,000. Electric vehicles and high-performance models require specialized labor and components, which drives up loss reserves for insurers. If you're managing a fleet of high-value assets, understanding Specialty Vehicle Insurance in Florida is essential for maintaining proper valuation and strategic coverage.

Demographics and Credit Scores

Underwriting excellence relies on granular demographic data. Statistics show that married drivers and homeowners often secure rates that are 10% lower because they're viewed as more stable risks. For younger professionals, the lack of a long-term driving history results in higher initial outlays. In 2026, the full coverage car insurance cost Florida for younger drivers remains elevated due to the high frequency of distracted driving incidents reported in state-wide traffic data. Strategic alignment with a firm like SI Insurance allows you to optimize these variables through meticulous profile management and proactive risk transfer strategies.

Proven Strategies for Risk Mitigation and Premium Reduction

Controlling the full coverage car insurance cost Florida residents encounter requires a shift from passive purchasing to active risk engineering. As we approach 2026, the complexity of the Florida market demands a calculated approach that balances immediate liquidity with long-term protection. You aren't simply buying a policy; you're constructing a bespoke safety net that must remain resilient against both environmental and economic volatility.

Strategic risk transfer often involves looking beyond the auto policy itself. By leveraging professional affinity discounts, many Florida executives and specialists can access preferred underwriting tiers. Organizations like the Florida Bar or various medical associations often have established relationships with carriers that recognize the lower risk profile of their members. These discounts aren't just minor perks; they represent a significant recalibration of your premium based on actuarial data that favors stable professional backgrounds.

Telematics and usage-based insurance (UBI) have moved from a niche offering to a primary tool for cost containment. By 2026, industry analysts expect over 65% of major carriers to offer some form of data-driven pricing. While the data privacy trade-off is a valid concern, the financial upside is undeniable. High-value clients who maintain low annual mileage or exhibit exemplary driving habits can see premium reductions of up to 30%. This turns your driving behavior into a tangible asset that directly offsets the rising full coverage car insurance cost Florida drivers face.

The Power of Multi-Policy Bundling

Combining your auto and Home Insurance in Florida creates a loyalty discount that acts as a powerful buffer against inflation. Carriers prefer a holistic relationship with their clients, often rewarding the consolidation of personal lines with premium credits ranging from 12% to 18%. Beyond the mathematical savings, bundling offers the administrative ease of managing a single strategic relationship. This centralized approach ensures there are no gaps in your liability coverage across different assets, providing a more cohesive defense against litigation.

Tactical Deductible Management

Adjusting your deductible is one of the most direct ways to assume tactical risk in exchange for lower monthly outflows. When you move a collision deductible from $500 to $1,000, you're essentially betting on your own risk management. If the premium savings allow you to recover that extra $500 in exposure within a 24-month period, the move is mathematically sound. A deductible is a form of self-insurance that should align with your liquid cash reserves. It's often strategic to maintain a lower deductible for comprehensive coverage, given Florida's high frequency of non-collision events like flood damage or windshield claims, while taking on more risk on the collision side.

Ready to optimize your portfolio?Contact SI Insurance to discuss a personalized risk assessment for your Florida assets.

Why a Bespoke Approach with SI Insurance Agency Secures Your Future

Most drivers begin their search by entering data into a cold, digital interface that returns a generic number. This algorithm-driven approach often ignores the structural complexities of the 2026 market. At SI Insurance Agency, we replace these automated guesses with a consultant-led risk assessment. We don't just find a price; we build a shield for your assets. While the average full coverage car insurance cost Florida residents encounter is influenced by broad market trends, your specific premium should reflect a meticulously engineered strategy rather than a software-generated estimate.

Our firm acts as a strategic guardian for Florida families and business owners who require more than a basic policy. We understand that your vehicle is often a significant component of a broader wealth management or business operations plan. By moving away from off-the-shelf products, you gain access to a level of foresight that protects against the volatile financial landscape expected in the coming years. We've seen how generic policies fail during complex litigation or catastrophic loss events; our goal is to ensure you never face those gaps.

Personalized Underwriting Excellence

Our agents advocate for you directly during the underwriting process to identify the most competitive carriers for your unique profile. This white-glove service model ensures that every detail of your history is leveraged to your advantage. You can expect a seamless experience where your risk manager handles the complexities of carrier negotiations. If you're ready to move beyond generic coverage, you should consult with a strategic risk manager at SI Insurance Agency to begin your assessment.

Our Commitment to the Broward County Community

Local expertise is an essential asset when filing a claim after a South Florida storm. Our physical presence in Broward County means we're here when the environment becomes unpredictable. We provide the stability and intellectual confidence you need to know your lifestyle is protected. We focus on delivering results through rigorous analysis and a deep commitment to long-term security. Choosing a plan is about more than the full coverage car insurance cost Florida providers list; it's about the peace of mind that comes from absolute financial certainty.

Consultant-led risk assessments that outperform basic algorithms.

Direct advocacy during the underwriting phase to secure elite carriers.

Deep-rooted South Florida expertise for rapid, local claim support.

Strategic alignment between your insurance portfolio and long-term financial goals.

Securing Your Financial Future in a Shifting 2026 Market

Navigating the complexities of the upcoming year requires more than just a standard policy. As the landscape evolves, the full coverage car insurance cost Florida drivers encounter will be shaped by localized environmental factors and shifting underwriting standards. You've seen how personalized risk mitigation and a thorough understanding of the "Florida Factor" can transform your financial outlook. By focusing on strategic alignment and long-term protection, you aren't just buying a policy; you're securing your stability.

SI Insurance Agency was founded in 2022 to bridge the gap between traditional coverage and sophisticated risk transfer. Our team brings deep expertise in both personal and commercial lines, operating as an independent agency to give you access to a vast network of top-tier carriers. We believe that every client deserves a meticulously engineered plan that reflects their unique circumstances. Don't leave your assets to chance in an unpredictable market. Secure your bespoke Florida auto insurance quote today and gain the intellectual confidence that comes with elite protection. We're ready to help you navigate these challenges with precision.

Frequently Asked Questions

What is considered "full coverage" for car insurance in Florida?

Full coverage in Florida isn't a single policy but a strategic combination of required Personal Injury Protection (PIP) and Property Damage Liability (PDL), alongside optional collision and comprehensive protections. While the state mandates $10,000 in PIP and PDL, a robust risk mitigation strategy usually includes bodily injury liability to protect personal assets. Most lenders for the 1.5 million financed vehicles in Florida require these additional layers to secure the physical asset against theft or accidents.

How much does full coverage car insurance cost per month in Florida on average?

The average full coverage car insurance cost Florida drivers encounter is approximately $291 per month, based on 2024 data from Bankrate. This figure represents a 40% increase over the national average, reflecting the unique risk profile of the state. Your specific premium depends on underwriting variables such as your ZIP code and driving history, which SI Insurance analyzes to ensure your coverage aligns with current market valuations.

Why is car insurance so expensive in Florida compared to other states?

High premiums result from a combination of dense urban populations and a high rate of litigation within the state's legal system. Florida also faces a 20.4% uninsured motorist rate according to the Insurance Research Council, which forces insured drivers to absorb higher systemic costs. Additionally, the 2023 hurricane season contributed to rising reinsurance rates, which carriers pass down to policyholders to maintain their solvency margins and underwriting excellence.

Can I lower my Florida car insurance cost without sacrificing essential protection?

You can lower your full coverage car insurance cost Florida premiums by strategically adjusting your deductibles or utilizing telematics programs that reward safe driving behavior. Increasing a collision deductible from $500 to $1,000 often yields a 15% to 30% reduction in the premium cost according to the Insurance Information Institute. We recommend maintaining high liability limits while seeking professional credits for advanced safety features or low annual mileage to ensure bespoke risk transfer.

Does my credit score affect my car insurance rates in Florida?

Your credit based insurance score significantly impacts your rates because carriers use this data to predict future claim frequency. In Florida, drivers with lower credit scores pay 141% more than those with excellent credit according to 2024 reports from WalletHub. It's a critical component of the underwriting process that reflects your overall financial stability. Maintaining a high score is a vital part of your long term strategic alignment with top tier insurers.

Is it worth getting uninsured motorist coverage in Florida?

Investing in uninsured motorist coverage is essential in Florida because roughly 1 in 5 drivers on the road lacks any insurance. This coverage acts as a bespoke risk transfer mechanism, ensuring you're compensated for medical expenses and lost wages if an at fault party is underinsured. Without it, you're personally liable for costs that exceed your PIP limits. It's a calculated move to prevent significant financial exposure in a high risk landscape.

How does a hurricane or flood affect my Florida auto insurance premiums?

Hurricanes and floods directly influence premiums through the comprehensive portion of your policy and the broader reinsurance market. Hurricane Ian in 2022 resulted in over $10 billion in insured vehicle losses, which led to a statewide adjustment in risk assessment models. While your individual premium might not spike immediately after a storm, the collective loss data forces carriers to recalibrate rates. This ensures the firm's internal processes remain stable during catastrophic events.

Should I bundle my auto and home insurance in Florida?

Bundling your auto and home insurance is a proven strategy for risk consolidation that typically results in a multi policy discount. Forbes Advisor reports that this strategic alignment can reduce total premiums by 10% to 25% depending on the carrier's appetite for risk. It also simplifies your administrative oversight by centralizing your asset protection under a single professional entity. This creates a sense of absolute security and intellectual confidence in your broader financial plan.