Bodily Injury Liability in Florida: A Strategic Guide to Essential Protection (2026)

- siinsuranceflorida

- 4 days ago

- 14 min read

What if the "No-Fault" laws designed to simplify Florida’s roads are actually the greatest threat to your personal financial stability? It's a common frustration among professionals who find that the state’s mandatory $10,000 Personal Injury Protection limit, established decades ago, barely scratches the surface of medical costs in 2026. You've likely felt the weight of confusion when trying to decipher why bodily injury liability Florida remains technically optional for most private motorists despite its role as the primary shield against a devastating civil judgment. We recognize that the complex syntax found in standard industry contracts often obscures the high stakes involved in sophisticated risk mitigation.

In this guide, we'll move beyond basic mandates to show you why Bodily Injury Liability is the most critical component of a strategic insurance portfolio. You'll gain absolute clarity on the fundamental differences between PIP and BI coverage, allowing you to move from a position of uncertainty to one of intellectual confidence. We'll provide a rigorous framework for selecting coverage limits that align precisely with your specific asset profile. By the end of this analysis, you'll possess a bespoke strategy to ensure your wealth remains protected against the volatile nature of the road.

Key Takeaways

Learn why Florida’s "No-Fault" status is often misinterpreted and how relying strictly on PIP coverage can leave your personal assets vulnerable in a serious accident.

Discover how to utilize bodily injury liability Florida coverage as a sophisticated financial shield to mitigate the risks of modern medical costs and litigation.

Identify the hidden dangers of maintaining only the state-mandated minimums and see how these limited policies fail to address the realities of 2026 recovery expenses.

Gain a clear, strategic framework for evaluating your net worth and daily commute to select insurance limits that offer genuine, long-term security.

Understand the value of an elite guardianship approach where meticulous policy design ensures your insurance portfolio is perfectly aligned with your high-value lifestyle.

Table of Contents Understanding Bodily Injury Liability in the Florida "No-Fault" Context The Hidden Risks of the "Florida Minimum" Insurance Strategy Comparing Coverage: PIP, PDL, and Bodily Injury Liability A Strategic Guide to Selecting Your Bodily Injury Limits The SI Insurance Approach: Elite Guardianship for Florida Drivers

Understanding Bodily Injury Liability in the Florida "No-Fault" Context

Bodily injury liability Florida functions as a sophisticated financial firewall, designed to isolate your personal assets from the volatility of post-accident litigation. While many drivers perceive insurance as a mere regulatory hurdle, SI Insurance views it as a cornerstone of bespoke risk transfer. In a state where high-value real estate and diverse business holdings are common, failing to secure adequate limits isn't just a lapse in coverage; it's a breakdown in strategic alignment. This coverage doesn't pay for your own injuries, but rather serves as your legal defense and settlement fund when you're held responsible for the physical harm of another person. Without it, your home equity, savings accounts, and future earnings remain vulnerable to court-ordered judgments.

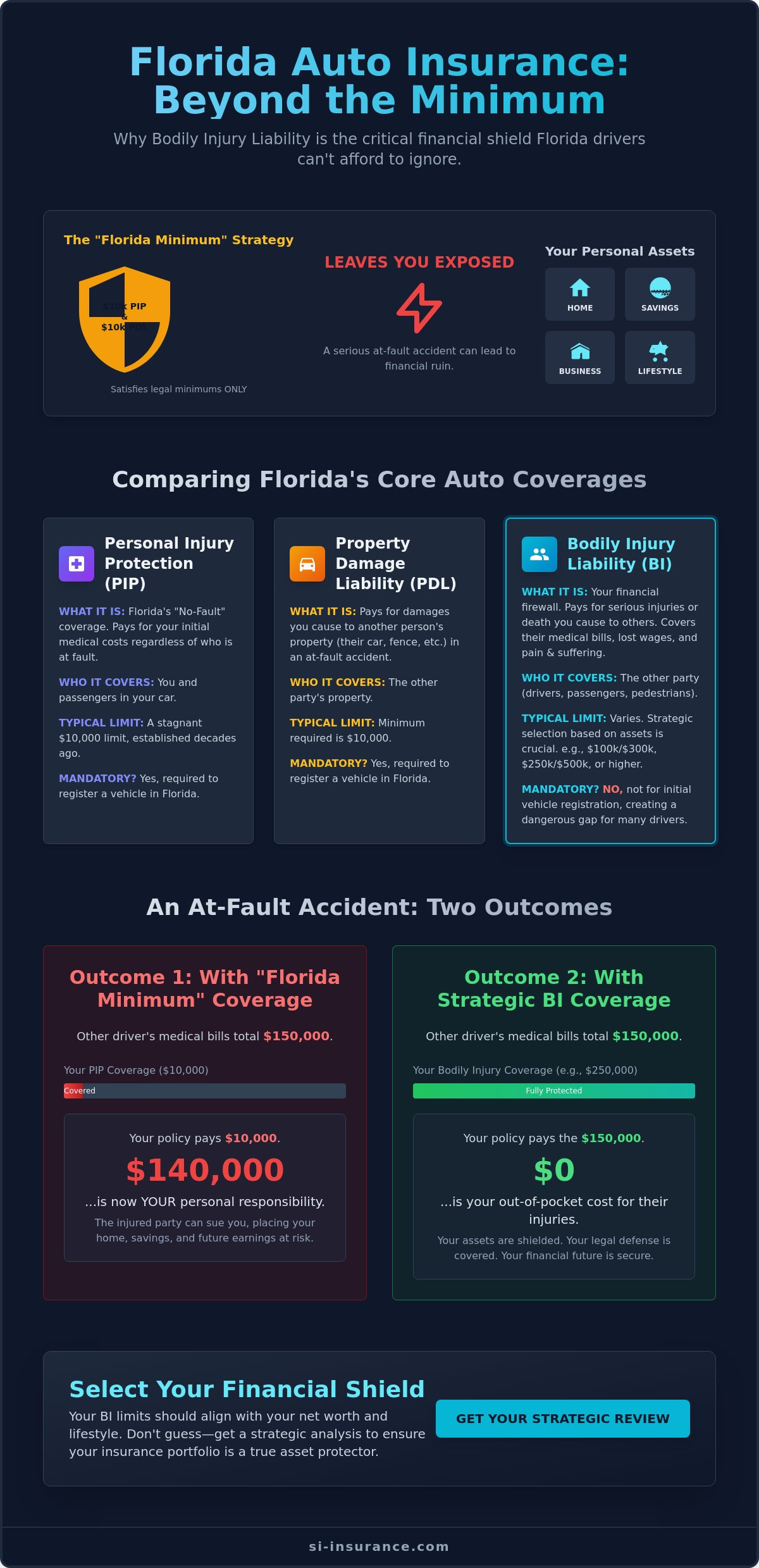

The common misconception regarding Florida’s "no-fault" status often leads to catastrophic financial exposure. Florida’s Motor Vehicle No-Fault Law, established in 1971, requires Personal Injury Protection (PIP) to ensure immediate medical attention regardless of who caused the crash. However, PIP is capped at a stagnant $10,000 limit, a figure that hasn't kept pace with the rising costs of modern healthcare. The broader landscape of Vehicle insurance in the United States demonstrates that liability coverage is the standard for protecting the public, yet Florida's unique statutes allow drivers to register vehicles without it. This creates a dangerous gap where a serious accident quickly exhausts PIP benefits, leaving the at-fault driver personally liable for the remaining balance of medical bills and non-economic damages.

To gain a deeper perspective on how these coverage layers function, watch this expert analysis:

The Legal Framework: PIP vs. Bodily Injury Liability

PIP acts as a first-party benefit, meaning it's paid by your own carrier to cover 80% of your medical expenses and 60% of lost wages. In contrast, bodily injury liability Florida is a third-party protection that triggers when an injured party meets the "permanent injury threshold." Under Florida Statute 627.737, if an accident causes significant scarring, permanent loss of a bodily function, or death, the "no-fault" immunity is pierced. At this juncture, the injured party can sue for full pain and suffering damages, making BIL coverage your only defense against a total loss of personal wealth.

Why Florida is Unique: The Financial Responsibility Law

Florida is one of the few states that doesn't require BIL for initial vehicle registration, but the Financial Responsibility Law of 1955 mandates it immediately following an at-fault accident or certain traffic convictions. If you cause a collision and don't have bodily injury liability Florida coverage, the state can suspend your driving privileges and vehicle registrations. To reinstate them, you're often forced into high-risk filings like the SR-22 or the even more stringent FR-44, which requires significantly higher liability limits for a period of three years. For our clients at SI Insurance, we emphasize that maintaining continuous BIL isn't just about legal compliance; it's about maintaining the intellectual confidence that your lifestyle won't be derailed by a single moment of negligence on the road.

The Hidden Risks of the "Florida Minimum" Insurance Strategy

Choosing to operate a vehicle with only Personal Injury Protection (PIP) and Property Damage (PD) coverage represents a significant strategic vulnerability. While these components satisfy the state's baseline legal mandate, they offer zero protection against claims for injuries you cause to others. In the high-stakes environment of 2026, relying on a $10,000 PIP limit is a gamble that rarely pays off. Data from Florida healthcare cost registries indicates that a standard emergency room evaluation for a moderate collision can exceed $12,500 within the first hour. Once that $10,000 limit is exhausted, the financial responsibility for the remaining medical bills falls directly on the at-fault driver.

The most common objection to adding coverage is the fact that it isn't strictly required by law for most drivers. However, the absence of a mandate doesn't equal an absence of liability. If you're found responsible for an accident, the injured party has the legal right to pursue your personal wealth to cover their losses. Without bodily injury liability Florida coverage, you're essentially self-insuring against a risk that can easily reach six or seven figures.

The Escalation of Medical Expenses and Legal Fees

Emergency care costs in Florida hospitals have risen by approximately 14% since 2023, making the old minimums obsolete. A single surgical procedure for a fractured limb or a disc herniation can quickly surpass $75,000. When you carry a robust policy, your insurer doesn't just pay the damages; they also fund your legal defense. Professional legal representation in a liability suit often costs upwards of $350 per hour, a cost that can drain a savings account before a case even reaches trial. To understand the legal nuances of these requirements, The Florida Bar's guide to auto insurance provides a comprehensive look at how state statutes govern these disputes. Florida law defines the permanent injury threshold as a physical impairment that consists of significant and permanent loss of a bodily function, permanent injury within a reasonable degree of medical probability, or significant and permanent scarring.

Asset Vulnerability: What is at Stake in Broward County?

For residents in high-value areas like Fort Lauderdale or Weston, the risks to personal wealth are particularly acute. While Florida's homestead exemption protects your primary residence, other vital assets remain entirely exposed to a court-ordered judgment. This includes:

Secondary vacation homes or rental properties

Business equity and commercial interests

Liquid savings in non-qualified brokerage accounts

Future wages, which can be garnished at a rate of up to 25% of your disposable earnings

The process of a judgment against an underinsured driver is relentless. Creditors can attach liens to your property, making it nearly impossible to sell or refinance assets until the debt is satisfied. Beyond the financial impact, the psychological weight of an unresolved liability claim can create years of stress and uncertainty. Developing a strategic risk mitigation plan ensures that your private wealth remains insulated from the volatility of the Florida courtroom, allowing you to maintain your lifestyle even in the face of an unforeseen accident.

Comparing Coverage: PIP, PDL, and Bodily Injury Liability

Florida's insurance framework requires a precise understanding of how different coverages interact to form a comprehensive safety net. Personal Injury Protection (PIP) functions as your immediate financial resource, covering 80% of your medical expenses and 60% of lost wages up to $10,000, regardless of who caused the accident. Property Damage Liability (PDL) is the second state-mandated component, which pays for damage you cause to another person's vehicle or property. However, bodily injury liability Florida coverage is the strategic element that protects your personal assets when you're held responsible for another person's physical injuries or death.

While PIP is designed to protect you, BI is designed to protect your balance sheet from third-party claims. These coverages work in tandem during a claim to address different silos of risk. A common vulnerability in many Florida policies is the absence of Uninsured Motorist (UM) coverage. Since 20% of Florida drivers are estimated to be uninsured, UM acts as a vital complement to BI. It provides you with the same level of protection you've extended to others, ensuring that if an underinsured driver hits you, your own policy fills the financial void.

Bespoke Coverage Frameworks

We align BI limits with your household's total economic exposure. A 10/20 split limit, providing $10,000 per person and $20,000 per accident, is often insufficient for anyone with home equity or significant savings. A 25/50 structure offers a mid-tier buffer, while a 100/300 split is the professional standard for established households. For business owners, a Combined Single Limit (CSL) is often the superior choice. Unlike split limits, a CSL provides a single, larger pool of funds, such as $300,000, that can be flexibly applied to any combination of bodily injury or property damage claims arising from a single event.

The Relationship Between BI and Umbrella Insurance

High BI limits aren't just a preference; they're the mandatory prerequisite for a Personal Umbrella policy. Most elite carriers require a minimum of 250/500 or 300/300 in primary BI coverage before they'll issue excess liability. This structure ensures there's no coverage gap between your auto policy and your umbrella policy. This integration is a cornerstone of a strategic guide to home insurance and comprehensive asset protection. If your primary bodily injury liability Florida limits are set too low, you're personally responsible for the financial "gap" before your umbrella policy activates, leaving your investments and property vulnerable to seizure or liens.

A Strategic Guide to Selecting Your Bodily Injury Limits

Securing the right level of bodily injury liability Florida coverage requires more than a cursory glance at state minimums. It's a deliberate exercise in asset preservation. You aren't just buying a policy; you're constructing a financial fortress. To ensure your protection aligns with your actual exposure, follow this five-step strategic framework.

Step 1: Conduct a comprehensive audit of your current net worth. Total your liquid assets, real estate equity, and projected future earnings. In a litigious environment, these are the targets of a judgment that exceeds your policy limits.

Step 2: Evaluate your daily risk exposure. Consider the 25-mile daily commute on I-95 versus a local five-minute drive. Heavier vehicles, such as a 6,000-pound luxury SUV, carry higher kinetic energy and greater potential for catastrophic damage than a compact sedan.

Step 3: Consult with a sophisticated advisor to model potential loss scenarios. A seasoned partner can simulate the financial impact of a multi-car accident or a long-term disability claim filed against you.

Step 4: Balance premium costs with the peace of mind of high-limit protection. The incremental cost of moving from a $100,000 limit to a $500,000 limit is often surprisingly low when compared to the 400% increase in coverage.

Step 5: Review and adjust limits annually as your financial landscape evolves. A promotion, a business acquisition, or an inheritance shifts your risk profile and necessitates a recalibration of your bodily injury liability Florida strategy.

Determining Your "Risk Profile"

Your risk profile isn't static. It's influenced by the number of drivers in your household and the specific machinery you operate. Adding a 16-year-old driver to your policy increases the statistical probability of a high-value claim by nearly 300% based on historical actuarial data. The "sweet spot" in coverage isn't found in the cheapest premium, but where your limits comfortably exceed your total attachable assets. This ensures that even a worst-case scenario doesn't derail your long-term financial objectives.

Navigating the Quote Process with SI Insurance

Working with an independent agency provides a distinct advantage through access to elite carriers that don't participate in the mass-market retail space. You can utilize Florida auto insurance quotes online for initial benchmarking, but the true value lies in bespoke underwriting. We focus on underwriting excellence, rewarding responsible drivers with rates that reflect their lower risk. Our team acts as a strategic guardian, ensuring that your risk transfer mechanisms are technically sound and meticulously structured.

Protect your legacy with a policy engineered for your specific needs. Request a sophisticated risk assessment from SI Insurance today.

The SI Insurance Approach: Elite Guardianship for Florida Drivers

Choosing an insurance policy shouldn't be treated as a simple retail transaction. At SI Insurance, we view it as the inception of a long-term strategic alliance designed to protect your legacy. Our firm functions as a dedicated partner in risk management; we prioritize intellectual precision over quick sales. We provide a white-glove service that focuses on bespoke risk transfer solutions tailored to the high-stakes environment of 2026. This approach ensures that your coverage isn't just a document in a glove box, but a calculated component of your broader financial strategy.

Our methodology moves away from the transactional nature of the industry. We focus on strategic alignment, ensuring that your limits reflect your actual exposure rather than a generic state minimum. By treating insurance as a sophisticated financial instrument, we help our clients maintain a position of quiet power. You aren't just buying a policy; you're securing a seasoned consultant who acts as an elite guardian for your assets.

Why a Local Florida Agency is Your Best Asset

Florida’s legal landscape presents unique challenges that require more than just a general understanding of insurance. In regions like Broward County and Sunrise, the intersection of high traffic volume and aggressive litigation makes specialized knowledge indispensable. Our team acts as a calm, steady hand during the volatility of a claim. We understand the local courts, the regional medical networks, and the specific underwriting excellence required to navigate this territory. Because we maintain offices across all cities in the State of Florida, we provide a localized presence that national firms lack. This proximity allows us to manage bodily injury liability Florida claims with a level of detail that protects your interests from the first report to the final settlement.

Securing Your Future Today

The core of any sound financial plan is foresight. As we’ve discussed throughout this guide, bodily injury liability Florida coverage serves as the primary foundation for your personal and professional security. It’s the barrier that keeps a single moment of road-side misfortune from escalating into a catastrophic loss of assets. We don't believe in off-the-shelf products for clients who have much to lose. Instead, we offer a meticulous review process that aligns your policy with your specific risk tolerance and long-term goals.

Strategic alignment of policy limits with total net worth to prevent asset seizure.

Continuous monitoring of Florida legislative changes that affect liability thresholds.

Direct access to senior risk consultants for proactive claim mitigation and support.

Customized underwriting that accounts for the specific driving conditions in Sunrise and Broward County.

Don't leave your financial stability to chance or an automated algorithm. We invite you to schedule a comprehensive policy review with our advisors to ensure your current protections are actually sufficient for the 2026 market. For a deeper look at how we structure these protections, please refer to our strategic guide to Florida auto insurance. Our commitment is to provide the stability and elite expertise you need to drive with absolute confidence.

Securing Your Financial Legacy on Florida’s Roadways

Navigating the evolving complexities of the 2026 insurance landscape requires more than just meeting the state's bare minimums. You've now seen how relying solely on basic Personal Injury Protection leaves your personal assets vulnerable to high-value litigation. A carefully structured bodily injury liability Florida policy serves as the cornerstone of a sophisticated risk management strategy, providing the defense you need when accidents lead to substantial legal claims. It's about moving beyond simple compliance toward a state of total financial security.

SI Insurance Agency operates as an independent firm founded on elite expertise, specifically focused on risk mitigation within Broward County. We don't offer generic products; instead, we provide access to a premium network of Florida-licensed carriers to deliver bespoke risk transfer solutions. Our team acts as a strategic guardian, ensuring your coverage limits align with your actual exposure. It's a methodical approach designed to instill absolute confidence in your protection. Request a bespoke strategic insurance review from SI Insurance Agency today to begin your journey toward intellectual and financial peace of mind. You've worked hard to build your future, and we're here to help you defend it with precision.

Frequently Asked Questions

Is Bodily Injury Liability mandatory for all drivers in Florida?

No, bodily injury liability Florida coverage isn't legally required for most private passenger vehicles under Florida Statute 627.736. While the law only mandates Personal Injury Protection and Property Damage Liability, omitting BI leaves your personal assets exposed to aggressive litigation. SI Insurance views this omission as a critical gap in a robust risk mitigation strategy, especially since state law requires proof of financial ability to pay for damages after an accident occurs.

What is the difference between Personal Injury Protection (PIP) and Bodily Injury (BI)?

PIP functions as first-party coverage that pays for your own medical expenses regardless of fault, whereas BI is third-party coverage that protects your assets when you're liable for another person's injuries. Under the current no-fault system, PIP covers 80 percent of your medical bills up to a 10,000 dollar limit. In contrast, BI provides a strategic buffer against lawsuits that arise from severe accidents where damages exceed the statutory thresholds defined in Section 627.737.

What happens if I cause an accident and I do not have Bodily Injury coverage?

You become personally responsible for all legal fees and settlement costs, which often leads to the seizure of your liquid assets or the garnishment of your wages. If a judgment is entered against you, the Florida Department of Highway Safety and Motor Vehicles can suspend your driving privileges and vehicle registrations. This creates a significant disruption to your professional mobility and necessitates a complex, costly process to reinstate your legal standing under the Financial Responsibility Law.

How much Bodily Injury Liability coverage should a Florida resident carry?

A sophisticated risk management profile typically requires at least 100,000 per person and 300,000 per accident to protect substantial personal holdings. While 2024 industry data suggests many drivers opt for lower limits, these often prove insufficient in high-velocity collisions involving multiple parties. Your coverage should align with your total net worth to ensure that a single catastrophic event doesn't compromise your long-term financial stability or your family's legacy.

Can I be sued in Florida if I have PIP insurance?

Yes, you can be sued if the claimant's injuries meet the permanent injury threshold established by Florida Statute 627.737. This legal standard includes permanent loss of a bodily function, significant scarring, or death. When these criteria are met, the no-fault immunity provided by PIP is waived. This allows the injured party to seek full compensation for pain and suffering, making your bodily injury liability Florida policy a vital component of your defensive legal posture.

Does Bodily Injury Liability cover my own medical bills after an accident?

No, BI is strictly designed to indemnify third parties for injuries you cause; it doesn't provide any direct financial benefit to the policyholder for their own recovery. To secure protection for your own medical expenses beyond the 10,000 dollar PIP limit, you should consider Medical Payments coverage or robust health insurance. Relying solely on BI for personal protection is a fundamental misunderstanding of strategic risk transfer and leaves your own healthcare costs unaddressed.

Will my insurance rates go up if I increase my Bodily Injury limits?

Premium adjustments are inevitable when you elevate your coverage limits, yet the incremental cost is often negligible compared to the catastrophic loss of personal wealth. Actuarial data indicates that doubling your BI limits doesn't result in a doubling of the premium. Instead, it offers a more favorable cost-to-risk ratio. SI Insurance recommends viewing this as a strategic investment in underwriting excellence rather than a simple recurring expense that lacks long-term value.

How does the Florida Financial Responsibility Law affect my need for BI?

The law mandates that any driver involved in an accident resulting in bodily injury must prove they can pay for damages through a BI policy or a high-value surety bond. If you're at fault and lack this coverage, you must satisfy the financial judgment before your driving privileges are restored. This 1955 statute effectively turns a voluntary coverage into a functional necessity for anyone who wishes to maintain their lifestyle and professional reputation after a collision.

Comments