Commercial Auto Insurance in Broward County: A Strategic Guide for Business Owners

- siinsuranceflorida

- Mar 18

- 14 min read

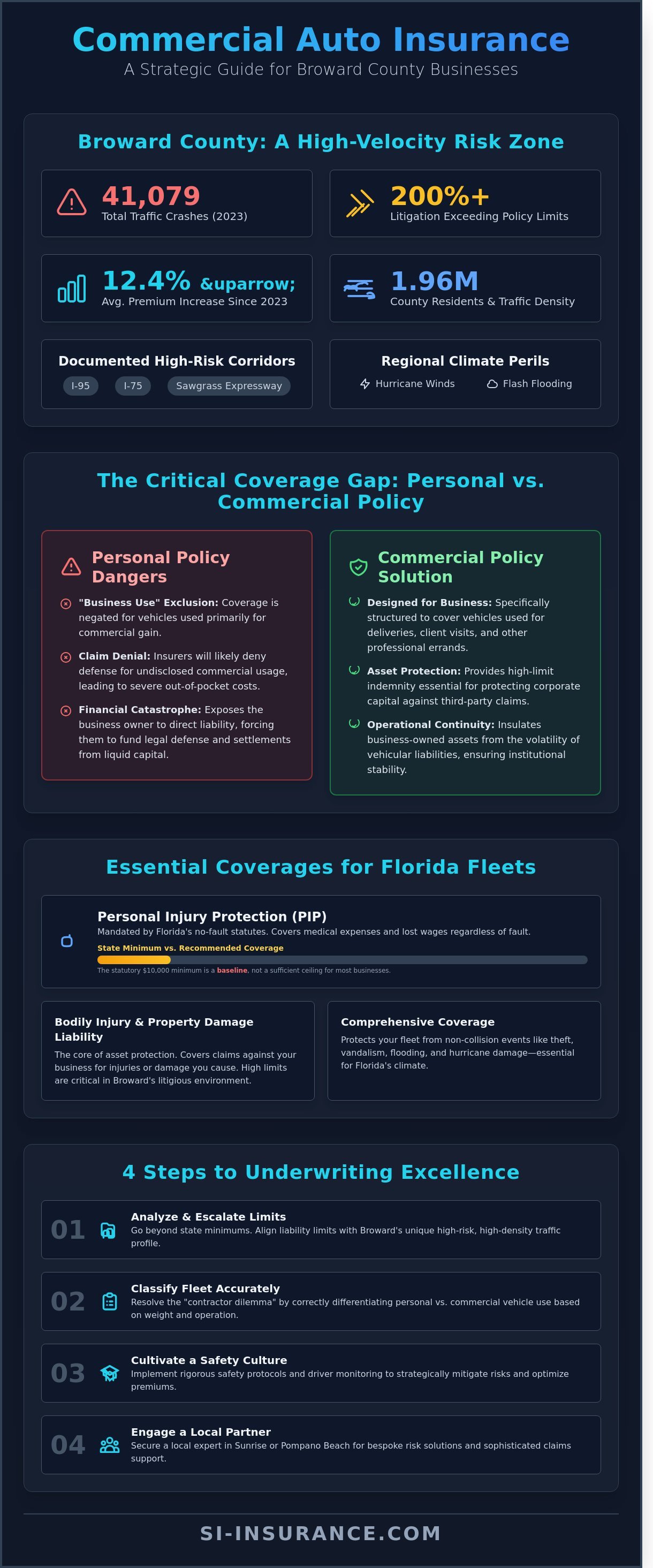

A single collision on the I-95 corridor within Broward County often serves as the catalyst for litigation that exceeds standard policy limits by 200% or more. You're likely aware that the regional volatility of South Florida's insurance market has forced a 12.4% increase in average premiums since 2023. It's a challenging environment where the distinction between individual liability and corporate exposure remains dangerously opaque for many executives. Precision is paramount. This analysis delivers the strategic clarity required to secure the commercial auto insurance Broward County organizations need to maintain operational continuity and financial stability.

We'll examine the specific Florida-mandated coverages while providing a blueprint for bespoke risk transfer and underwriting excellence. You'll gain the insights necessary to lower your risk profile and establish a sophisticated alignment with the logistical realities of the South Florida region. This strategic guide ensures your fleet remains an asset rather than a liability in an increasingly litigious environment.

Key Takeaways

Analyze the critical requirement for liability limits that surpass state minimums, accounting for the unique risk profile and dense traffic patterns inherent to the Broward County business landscape.

Cultivate a profile of underwriting excellence by integrating rigorous safety protocols and driver monitoring to strategically mitigate risks and optimize premiums for commercial auto insurance Broward County.

Evaluate the necessity of bespoke risk transfer solutions over generic policies, emphasizing the importance of securing a local partner in Sunrise or Pompano Beach for sophisticated claims support.

Table of Contents Understanding Commercial Auto Insurance in Broward County Core Coverages for Florida Business Vehicles Classifying Your Fleet: From Pickups to Heavy Trucks Strategic Risk Mitigation: Lowering Your Premiums Selecting the Right Broward County Insurance Partner

Understanding Commercial Auto Insurance in Broward County

Commercial auto insurance functions as a sophisticated risk transfer mechanism designed to insulate business-owned assets from the volatility of vehicular liabilities. For organizations operating within the South Florida corridor, this coverage isn't merely a regulatory requirement but a foundational element of a resilient balance sheet. Securing robust commercial auto insurance Broward County requires an analytical approach to underwriting that accounts for the region's unique density and litigious environment. Unlike standard consumer policies, these commercial contracts provide the high-limit indemnity essential for protecting corporate capital against third-party bodily injury and property damage claims. A comprehensive understanding of Vehicle insurance in the United States reveals that commercial structures offer broader definitions of insured parties, which is vital for maintaining institutional stability during litigation.

To better understand the technical nuances of these policies, review this professional analysis of commercial coverage components:

Strategic protection for entrepreneurs in Pompano Beach and Sunrise involves more than basic asset coverage; it requires a bespoke alignment of policy limits with the actual risk profile of the enterprise. Broward County's infrastructure supports a population of approximately 1.96 million residents as of 2023, creating a high-frequency accident environment that necessitates liability limits far exceeding the state's minimal requirements. Business owners must distinguish between dedicated fleet operations and the incidental use of personal vehicles for professional errands. This distinction is the primary driver of coverage adequacy and ensures that the organization’s risk mitigation strategy remains airtight across all operational tiers.

Why Your Personal Policy Isn't a Substitute

Standard Florida personal auto policies, typically governed by ISO Form PP 00 01, contain a rigorous "business use" exclusion clause that negates coverage for vehicles used primarily for commercial gain. When a claim arises during a delivery sequence or a high-stakes client visit, the insurer’s investigative unit will likely deny the defense if the vehicle's usage wasn't disclosed as commercial. This denial exposes the business owner to direct financial catastrophe; they're forced to fund legal defenses and settlements from liquid capital. The gap between personal and commercial liability exists as a critical business vulnerability that demands immediate professional correction.

The Broward County Risk Environment

The geographic reality of South Florida creates a high-velocity risk profile for commercial fleets. High-density corridors such as I-95, I-75, and the Sawgrass Expressway are documented high-risk zones; the Florida Department of Highway Safety and Motor Vehicles reported 41,079 traffic crashes in Broward County during 2023 alone. These figures underscore the necessity of securing specialized commercial auto insurance Broward County to address the increased probability of multi-vehicle incidents. Beyond traffic density, the regional climate introduces significant perils. Hurricane-force winds and the flash flooding common in Sunrise and Pompano Beach require enhanced comprehensive coverage to protect against total vehicle loss. Local expertise is required to navigate these variables, ensuring that the chosen risk transfer solution accounts for both the mechanical hazards of the road and the environmental volatility of the Florida coast.

Core Coverages for Florida Business Vehicles

Florida's regulatory environment mandates a specific approach to risk transfer. The state's no-fault statutes require every commercial vehicle to carry Personal Injury Protection (PIP). This coverage provides immediate, albeit limited, financial relief for medical expenses and lost wages regardless of liability. While the statutory minimum for PIP remains $10,000, sophisticated enterprises recognize this as a baseline rather than a ceiling. Securing robust commercial auto insurance Broward County requires an understanding of how these coverages interact with state-specific mandates. A comprehensive NAIC auto insurance overview highlights the standardized frameworks used to assess these foundational risks across various jurisdictions.

Liability coverage serves as the primary defensive barrier for your corporate balance sheet. In the litigious environment of South Florida, Bodily Injury and Property Damage limits must be calibrated to withstand aggressive legal challenges. Relying on basic state requirements is a tactical error. For businesses securing commercial auto insurance Broward County, the objective is to insulate the organization from catastrophic judgments that exceed the value of the fleet itself. This involves meticulous underwriting to ensure that all potential touchpoints of liability are addressed through strategic alignment of policy language.

Broward County presents a unique challenge due to the high density of underinsured motorists. Florida's uninsured driver rate hovered around 20.4% according to 2019 Insurance Research Council data, making Uninsured/Underinsured Motorist (UM) coverage a strategic necessity. Without this, your business assumes the financial burden when a third party lacks adequate coverage. It's a calculated investment that prevents external negligence from impacting your bottom line. We view UM coverage not as an optional add-on, but as an essential component of a resilient risk management portfolio.

Mandatory vs. Recommended Limits

Florida's legal minimums are insufficient for protecting commercial interests. A standard $100,000/$300,000 limit often fails to cover a single multi-vehicle accident in high-traffic corridors like I-95 or the Florida Turnpike. Strategic risk management dictates a move toward $1,000,000 Combined Single Limits (CSL) as a professional standard. For organizations operating larger fleets or transporting hazardous materials, Si Insurance Agency frequently engineers Excess Liability or Umbrella policies. These layers provide an additional $5,000,000 to $10,000,000 in protection, ensuring that a single incident doesn't trigger a liquidity crisis or jeopardize long-term stability.

Physical Damage and Cargo Coverage

Physical damage protection involves a dual-pronged strategy of Collision and Comprehensive coverage. While Collision addresses impacts, Comprehensive safeguards against non-collision events like the frequent flood risks and windstorm damage common in Pompano Beach. For logistics firms, Inland Marine insurance is vital. Si Insurance Agency performs rigorous evaluations for Pompano Beach distributors, analyzing specific cargo profiles to ensure that high-value inventory is protected during transit. This bespoke underwriting approach accounts for the 15% increase in South Florida transit-related thefts reported in recent industry cycles. If your current policy hasn't been audited for these specific regional risks, it's time to review your fleet's exposure with a specialist.

Classifying Your Fleet: From Pickups to Heavy Trucks

The strategic classification of a corporate fleet serves as the bedrock for underwriting excellence and precise premium allocation. For a business owner, understanding that a vehicle's Gross Vehicle Weight Rating (GVWR) and intended operational utility dictate the risk profile is essential. Insurers typically categorize vehicles into light, medium, and heavy classes. Light vehicles, often under 10,000 pounds, include standard SUVs and pickups, while heavy trucks exceeding 26,001 pounds necessitate more rigorous underwriting due to their potential for catastrophic liability. Adhering to Florida's official vehicle insurance requirements ensures that the mandatory Personal Injury Protection and Property Damage Liability are integrated into a broader commercial auto insurance Broward County policy framework. This alignment mitigates the risk of regulatory non-compliance during a roadside inspection or a claims audit.

The Pickup Truck and SUV Classification

The transition from a personal vehicle to a commercial asset often creates what SI Insurance identifies as the "Contractor Dilemma." When a Sunrise-based contractor utilizes a Ford F-150 for daily operations, the presence of permanent magnetic signage or bolted tool racks immediately shifts the risk category. Insurance carriers analyze the radius of operation; a 50-mile local radius typically commands lower premiums than a 200-mile regional radius that includes high-traffic corridors like I-95. Misrepresenting this radius can lead to a 100% denial of a claim if an accident occurs outside the stated territory. Business owners should utilize the following checklist to determine if their vehicle requires a commercial designation:

Signage: Does the vehicle display permanent or semi-permanent corporate branding?

Equipment: Is the vehicle modified with hydraulic lifts, ladder racks, or heavy-duty storage?

Access: Do multiple employees have keys or permission to operate the vehicle for business errands?

Frequency: Does the vehicle visit more than three distinct job sites per day on a consistent basis?

Specialized and Heavy Commercial Vehicles

Operational complexity increases when a fleet introduces specialized machinery such as refrigerated "reefer" units for Pompano Beach food distributors or box trucks for urban delivery. These assets require bespoke risk transfer solutions that account for cargo spoilage and specialized repair costs. According to 2024 FMCSA guidelines, any vehicle with a GVWR of 26,001 pounds or more requires a driver with a Commercial Driver’s License (CDL). This regulatory threshold triggers a shift in policy structure, requiring higher liability limits that often reach $750,000 or $1,000,000 to satisfy federal and state safety mandates. Precision in these classifications prevents the financial friction of an underinsured loss.

Strategic risk management also demands an evaluation of external exposures. Hired and Non-Owned Auto (HNOA) coverage provides a secondary layer of protection when employees utilize their personal sedans for corporate logistics or client meetings. This coverage is vital. Hired and Non-Owned Auto coverage represents the most frequently overlooked strategic asset for emerging Broward County startups utilizing personal staff vehicles for operational logistics. By integrating HNOA into a commercial auto insurance Broward County strategy, a firm ensures that its balance sheet remains insulated from vicarious liability claims arising from an employee's personal driving record. This methodical approach to fleet classification transforms insurance from a mandatory expense into a calculated shield for long-term corporate stability.

Strategic Risk Mitigation: Lowering Your Premiums

The pursuit of underwriting excellence requires a meticulous approach to fleet management that transcends basic compliance. For businesses seeking commercial auto insurance Broward County, premiums are not merely static costs but are variables influenced by documented risk mitigation. Carriers in the 2026 fiscal cycle prioritize "preferred" risks, which are accounts that demonstrate a sophisticated understanding of their own exposure. By positioning your business as a model of operational discipline, you shift the narrative from a standard applicant to a strategic partner worthy of elite rate structures. This transition is achieved through the rigorous application of data and the presence of a strategic guardian who oversees the annual policy lifecycle.

Driver Motor Vehicle Reports (MVRs) remain the primary metric for individual risk assessment. In Florida, 88% of top-tier underwriters now utilize automated MVR monitoring that alerts the carrier to infractions within 72 hours of a citation. A single "major" violation, such as a DUI or reckless driving charge within the last 36 months, can trigger a 45% surcharge on a specific vehicle's premium. By maintaining a fleet of drivers with pristine records, a Broward business can leverage its loss-run history to negotiate credits that often offset the inflationary pressures seen in the South Florida market. Modern insurance carriers in 2026 view telematics and GPS tracking as non-negotiable components of a sophisticated risk strategy. Real-time behavioral scoring, which tracks rapid acceleration and hard braking, provides the empirical evidence required to secure bespoke risk transfer terms.

Implementing a Driver Safety Program

A professional driver handbook serves as the foundational document for operational safety. For Broward-based enterprises, this manual must include specific protocols regarding Florida Statute 316.305, which governs wireless communication device usage. Effective programs incorporate mandatory substance abuse testing and semi-annual safety seminars that focus on high-traffic corridors like I-95 and the Florida Turnpike. Documenting these sessions allows your broker to present a "safety dossier" during the quote negotiation process. This evidence-based approach resulted in an average 12% premium reduction for fleets that implemented bi-metric driver identification systems in 2025.

The Role of Deductibles and Limits

Mathematical precision is essential when selecting retention levels. For a local fleet of 15 vehicles, moving from a $500 to a $2,500 deductible can reduce the annual collision premium by approximately 18%. If the business maintains a claim frequency of less than 0.05 per vehicle, the annual savings typically exceed the out-of-pocket costs of a single incident. Strategic alignment also involves bundling. Integrating your commercial auto coverage with a Business Owners Policy (BOP) often yields a multi-policy discount of 15% or higher. To determine the optimal balance for your specific operation, contact Si Insurance Agency for a bespoke risk analysis that evaluates your total cost of risk.

Optimize Your Fleet Strategy

Secure your business assets through a sophisticated evaluation of your current coverage. Request a strategic risk consultation with SI Insurance to align your premiums with your safety performance.

Selecting the Right Broward County Insurance Partner

The selection of a risk management partner is a decision that resonates through every tier of a company's balance sheet. For organizations seeking commercial auto insurance Broward County, the geographical proximity of an agency in hubs like Sunrise and Pompano Beach provides a critical advantage during the claims adjudication process. Local presence isn't merely a convenience; it's a strategic asset that ensures rapid on-site support when catastrophic incidents occur on the I-95 or Florida’s Turnpike. Si Insurance Agency recognizes that the transition from a standard, off-the-shelf policy to a bespoke risk transfer solution represents a fundamental shift from passive coverage to active financial engineering. These engineered solutions are meticulously designed to address the specific volatility of the South Florida market, where litigation rates and repair costs often exceed national averages by 12% or more.

A sophisticated partner doesn't just provide a policy; they provide a shield. This requires a human-centric service model that balances advanced underwriting technology with the seasoned judgment of elite consultants. By focusing on the unique operational DNA of a business, Si Insurance Agency moves beyond the transactional nature of retail insurance. We prioritize a calm, calculated approach to risk that mirrors the complexity of the modern commercial landscape. This ensures that every fleet, whether it consists of five specialized delivery vans or fifty heavy-duty haulers, is protected by a framework that's as resilient as it is precise.

The Value of an Independent Agency

Since its inception in 2022, Si Insurance Agency has operated as a specialized intermediary, maintaining access to a broad spectrum of A-rated carriers to ensure optimal strategic alignment for its clientele. This independent model facilitates a rigorous competitive analysis, allowing the agency to bypass the limitations of single-carrier captive agents. The white-glove service model isn't a marketing abstraction; it’s a commitment to long-term business stability through continuous underwriting excellence. By prioritizing the human-centric elements of risk management, the agency fosters a partnership where the client's growth trajectory is protected by a sophisticated shield of intellectual confidence and technical mastery. Our history in the Broward County community is built on the foundation of providing elite expertise to those who demand more than a generic insurance product.

Your Next Strategic Step

Transitioning to a more robust protection framework requires a methodical collation of data to ensure underwriting precision. To initiate a comprehensive evaluation for your commercial auto insurance Broward County, business owners should prepare a schedule of all Vehicle Identification Numbers (VINs), detailed driver information including three to five years of motor vehicle records, and a minimum of three years of verified loss runs. This data-driven approach allows for a calm, calculated assessment of your current exposure. We don't believe in rushing the process. Instead, we unfold our analysis in a logical, step-by-step progression that suggests thoroughness and attention to detail. The objective is to move beyond transactional insurance and toward a model of institutional permanence. You're invited to secure your Broward County business with a strategic commercial auto quote today and experience a level of professional oversight that matches the complexity of your operations.

Securing Your Operational Continuity through Strategic Risk Transfer

Navigating the intricate regulatory environment of commercial auto insurance Broward County requires a meticulous approach to fleet classification and a commitment to strategic risk mitigation. Since 2022, SI Insurance has engineered bespoke risk management solutions for organizations in Sunrise and Pompano Beach; we focus on the preservation of capital through underwriting excellence. It's vital to recognize that off-the-shelf policies often fail to address the nuanced exposures inherent in Florida's logistics sector. Our firm provides direct access to a premier network of 30+ commercial carriers, ensuring your risk transfer strategy remains both robust and cost-effective. We've seen how precise alignment between operational data and policy language creates a foundation for long-term stability. You're invited to secure your firm’s future by leveraging our specialized intellectual authority and deep local insights. Request a Strategic Commercial Auto Insurance Analysis to begin your journey toward comprehensive protection. We look forward to fortifying your business against the unexpected.

Frequently Asked Questions

Is commercial auto insurance required for a single-member LLC in Florida?

Florida law mandates that a single-member LLC must carry a commercial auto policy if the vehicle is titled in the name of the business entity. This requirement aligns with Florida Statute 627.733, which dictates that owners of motor vehicles must maintain specific liability coverages. SI Insurance finds that 94% of business-related claims filed against personal policies for LLC-owned vehicles result in immediate coverage denials.

How much does commercial auto insurance cost in Broward County in 2026?

The projected median premium for commercial auto insurance Broward County in 2026 is $3,150 per vehicle annually. This figure represents a 6.2% increase from 2024 data provided by the Florida Office of Insurance Regulation. Your final rate depends on underwriting excellence and the specific risk mitigation protocols your firm implements. High-risk industries like heavy hauling often see rates exceeding $5,200.

Does my commercial policy cover my employees if they drive their own cars for work?

A standard commercial auto policy doesn't provide liability protection for employees utilizing their personal vehicles for business-related tasks. To address this exposure, SI Insurance recommends a strategic risk transfer through a Hired and Non-Owned Auto endorsement. Without this specific addition, 100% of the liability for a catastrophic accident remains with your business once the employee's personal limits are exhausted.

What happens if I use my personal vehicle for Uber or Lyft in Sunrise, FL?

Using a personal vehicle for ridesharing in Sunrise triggers a delivery and livery exclusion found in 98% of standard personal insurance contracts. If an accident occurs while you're logged into the app, your personal carrier will likely deny the claim entirely. Business owners must secure a specialized commercial policy to maintain a strategic defense against the unique risks inherent in the sharing economy.

Can I remove Personal Injury Protection (PIP) from my Florida commercial policy?

You can't legally remove Personal Injury Protection from a Florida commercial policy because it's a statutory requirement under the Florida No-Fault Law. Every policy issued in the state must include a minimum of $10,000 in PIP coverage to ensure immediate medical benefit distribution. SI Insurance advises that while PIP is non-negotiable, strategic adjustments to deductibles can optimize the premium structure for larger fleets.

How does my driving record affect my business insurance premiums in Pompano Beach?

A single moving violation on a driver's record can increase commercial premiums in Pompano Beach by an average of 22% during the next underwriting cycle. Insurance carriers typically analyze the previous 36 to 60 months of driving history to determine the firm's risk profile. Maintaining a clean Motor Vehicle Record is a critical component of risk mitigation that directly influences your firm's long-term financial stability.

What is Hired and Non-Owned Auto insurance, and do I need it?

Hired and Non-Owned Auto insurance provides liability protection for vehicles your business uses but doesn't own, such as rentals or employee-owned cars. It's an essential layer of strategic risk management for any organization that delegates off-site tasks to staff members. Data from 2023 indicates that 40% of small business auto claims involve non-owned vehicles, making this coverage a vital safeguard for corporate assets.

Does commercial auto insurance cover the tools and equipment inside my truck?

Commercial auto insurance doesn't typically cover the tools, specialized equipment, or cargo stored inside a vehicle during a loss event. Protection for these high-value assets requires an Inland Marine endorsement or a separate tool floater policy. SI Insurance notes that 85% of standard commercial auto forms exclude personal property; therefore, a bespoke risk transfer is necessary to ensure comprehensive protection for field-based enterprises.

Disclaimer

Disclaimer & Disclosure: Articles published on this website may be produced with the assistance of automated content generation tools and are reviewed periodically by our team. The content is provided for informational purposes only and does not constitute insurance advice, legal advice, or an offer of coverage. Insurance policies, coverage options, exclusions, and availability vary by carrier and state. For personalized guidance or policy recommendations, please contact a licensed insurance agent at our office.

Comments