Condo Insurance vs. HOA Policy in Florida: A Strategic Guide to Coverage Gaps (2026)

- siinsuranceflorida

- 7 days ago

- 14 min read

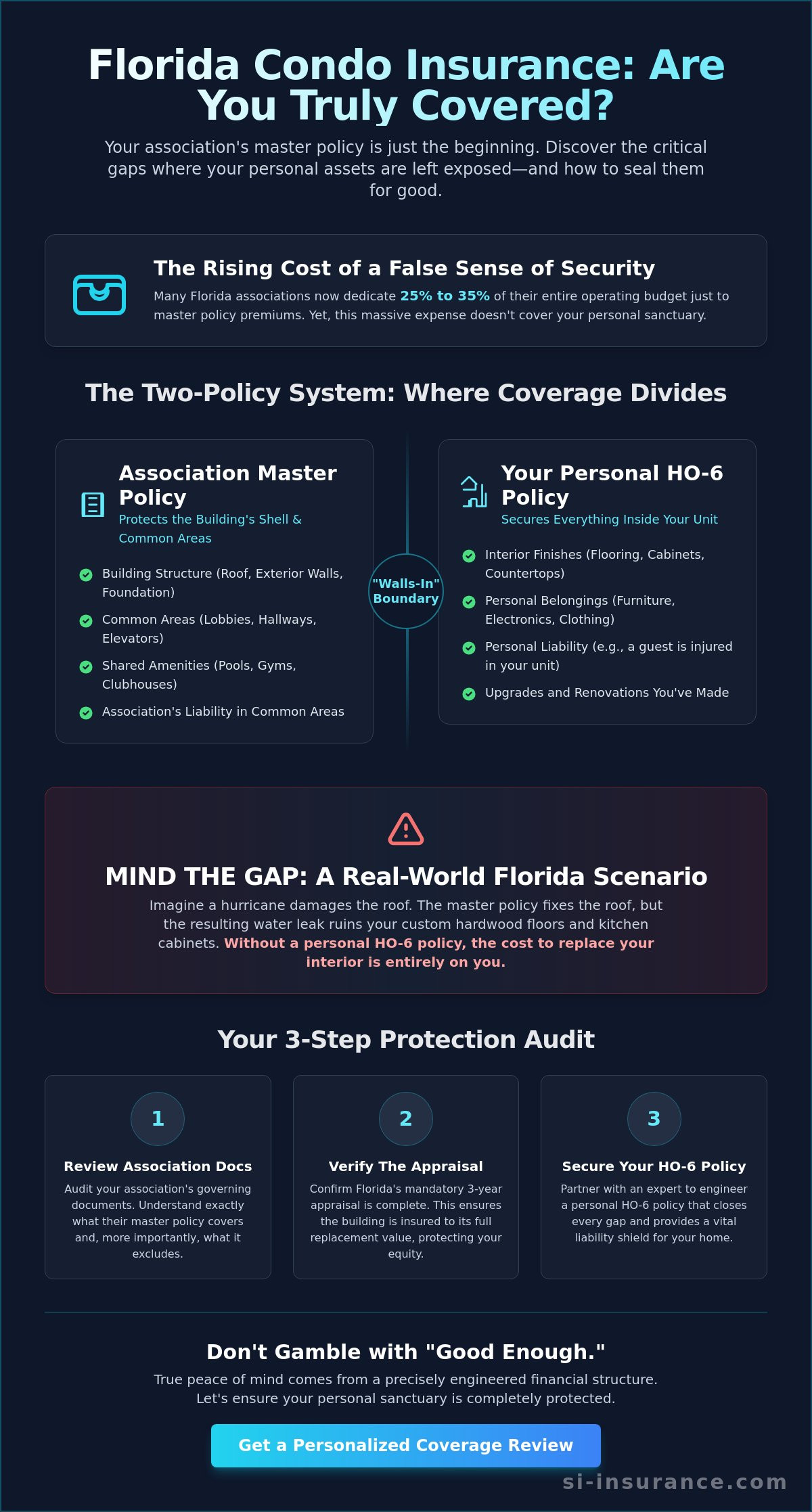

What if the "all-in" coverage your association promises actually leaves your most valuable interior assets completely exposed to the next major storm? When evaluating the technical complexities of condo insurance vs HOA policy Florida, many residents mistakenly assume their monthly fees provide a comprehensive safety net for their homes. You likely feel the weight of these rising costs already; many Florida associations now dedicate between 25% and 35% of their entire operating budgets just to maintain master policy premiums.

We understand the concern that comes with navigating these high-stakes financial landscapes and the desire for absolute security in your personal sanctuary. This guide will clarify the exact boundary where your association's responsibility ends and your personal coverage must take over to ensure your assets are fully protected. We will explore the critical differences between "bare walls" and "all-in" policies, the implications of recent 2026 legislative updates such as the mandatory three year appraisal cycles, and the strategic steps required to identify and close dangerous coverage gaps before they become a liability.

Key Takeaways

You'll learn how Florida Chapter 718 mandates specific building protections, giving you a clear starting point for your own risk management strategy.

Clarifying the line between condo insurance vs HOA policy Florida helps you protect personal upgrades and interior finishes that the master policy often excludes.

We'll show you how to audit your association's governing documents to find hidden gaps before they lead to unexpected out of pocket costs.

Discover how a personal HO-6 policy secures your private assets and provides a vital liability shield against incidents occurring inside your home.

You'll gain the technical insight to verify that your building's mandatory three year appraisal requirements are met, ensuring your investment stays properly valued.

Table of Contents

Navigating the Florida Condo Insurance Ecosystem in 2026

Living in a Florida condominium involves a sophisticated financial partnership between the individual unit owner and the association. You've likely noticed your monthly assessments climbing as the insurance market adjusts to new realities. Currently, many Florida condo associations allocate between 25% and 35% of their annual operating budgets solely to insurance premiums. This financial pressure makes it vital to understand the technical divide between your condo insurance vs HOA policy Florida. It's not just about paying the bill; it's about verifying that the statutory requirements of Chapter 718 are being met to protect your equity.

Florida law, specifically Statute 718.111, mandates that associations obtain independent appraisals every three years to ensure the building is insured to its full replacement value. These regulations act as a safeguard for the building's structural integrity, which is a critical component in a state where hurricane risk is a permanent factor. To truly secure your assets, you need a foundational understanding of condominium insurance and how it complements the master policy. This knowledge allows you to move past the anxiety of rising costs and toward a position of intellectual confidence in your coverage.

To better understand this concept, watch this helpful video:

The Two-Policy System: A Protective Guardian

The relationship between your personal HO-6 policy and the association’s master policy is designed to be symbiotic rather than redundant. The primary dividing line is the "Walls-in" concept. This boundary dictates that the association is responsible for the building's exterior shell and common areas, while you are responsible for everything from the primer on the walls inward. This structure is intended to prevent the double-billing of premiums, ensuring you aren't paying twice for the same coverage. Recent building safety reforms, such as the mandatory milestone inspections required for older buildings, have significantly influenced premium structures in 2026. These reforms provide a clearer picture of a building's risk profile, which can lead to more accurate, if sometimes higher, insurance costs. Understanding the interplay of your condo insurance vs HOA policy Florida ensures that your personal liability and property interests remain distinct and fully protected.

Why "Good Enough" is a Risky Strategy in Florida

Relying on a generic policy is a dangerous gamble in a state prone to severe weather and water damage. True protection requires a calculated approach where every potential gap is sealed. For example, if a hurricane damages the roof and causes water to leak into your unit, the master policy might cover the roof, but it won't touch your custom flooring or high-end cabinetry. This is where the expertise of an independent agent at SI Insurance becomes invaluable. They act as a protective guardian, helping you audit the master policy and the association's governing documents to ensure your personal assets aren't left exposed during a catastrophic event. By treating insurance as a precisely engineered financial structure, you can maintain stability even in a volatile market.

The Association Master Policy: Protecting the Shell and Common Elements

The association’s master policy acts as the primary defense for the physical structure of your building. This policy is designed to cover what are known as "Common Elements." Think of the roof above your head, the elevators that carry you to your floor, and the sophisticated lobbies that define your building’s aesthetic. These are shared assets that belong to the community as a whole. While your monthly HOA fees contribute to these premiums, it’s important to remember that this policy is built to protect the association’s interests first. It ensures that the "shell" of the building can be rebuilt after a catastrophic event, keeping the community viable.

In Florida, the Florida Office of Insurance Regulation oversees the carriers that provide these massive policies. For 2026, mid-sized coastal properties are seeing premiums between $75,000 and $250,000, while large high-rises can face costs exceeding $2 million. However, a common point of confusion in the condo insurance vs HOA policy Florida debate is where this protection stops. The master policy generally ignores your personal belongings, furniture, and any high-end upgrades you’ve made to your unit. If a pipe bursts and ruins your custom hardwood flooring, the association’s policy likely won't provide a cent for the repair. You are essentially responsible for the "airspace" you inhabit.

Bare Walls vs. All-In: Understanding the Foundation

The level of interior coverage depends entirely on whether your association maintains a "Bare Walls" or "All-In" policy. A Bare Walls policy is the most common choice in the current Florida market because it helps keep association premiums manageable. It covers the building from the exterior up to the drywall or studs, leaving everything inside to you. Conversely, an All-In policy includes original fixtures like appliances and standard flooring. Because Florida associations are facing steep premium hikes, most choose Bare Walls to manage their annual budgets, shifting more responsibility to the individual owner's policy.

Liability and Shared Asset Protection

Beyond physical damage, the master policy includes General Liability coverage. This protects the association if a guest slips in the lobby or is injured at the community pool. It also typically includes Directors and Officers (D&O) insurance, which shields board members from personal liability regarding their management decisions. It’s a vital layer of security, but it protects the legal entity of the building, not you as a resident. If someone is injured inside your specific unit, the master policy offers no protection for your personal assets.

When a major claim occurs, associations often face high deductibles that aren't always fully funded by reserves. These costs are frequently passed down to owners through special assessments, which can be a significant financial shock. To ensure your personal plan accounts for these potential expenses, it's wise to review your specific risk profile with a professional who understands the nuances of the local landscape. By identifying these gaps early, you can maintain your financial stability regardless of what happens in the common areas.

Condo Insurance (HO-6) vs. HOA Master Policies: Identifying the Gaps

If the association’s master policy is the armor protecting the building’s skeleton, your personal condo insurance, or the HO-6 policy, is the specialized shield for everything contained within your four walls. Many Florida residents operate under the assumption that their monthly HOA fees buy them a comprehensive safety net. However, the reality of the condo insurance vs HOA policy Florida relationship is that the master policy is designed to restore the building, not to replace your Italian leather sofa or reimburse you for a lawsuit following a guest's injury in your kitchen. As of April 2026, an HO-6 policy typically ranges from $600 to $1,600 annually, a relatively small investment to secure assets that the association simply won't cover.

Beyond physical items, your personal policy provides two critical lifelines: Personal Liability and Loss of Use. Liability coverage acts as a financial barrier if you're found responsible for property damage or bodily injury occurring inside your unit. Meanwhile, Loss of Use coverage is vital in the high-risk Florida environment. If a fire or severe storm makes your home uninhabitable, this provision pays for your temporary housing and living expenses while the building is being repaired. Without it, you could be stuck paying a mortgage and a hotel bill simultaneously.

The Critical Role of Loss Assessment Coverage

Loss Assessment coverage is perhaps the most vital component for any Florida condo owner, yet it's frequently misunderstood. Loss Assessment is the bridge between a master policy deductible and your personal finances. When a major claim occurs, such as hurricane damage to common areas, the association's deductible can be massive. If the master policy has a 3% or 5% windstorm deductible, the board often divides that multi-hundred-thousand-dollar cost among all unit owners. While many basic policies offer a $1,000 or $2,000 limit for these assessments, this is often insufficient in 2026. If your building faces a $500,000 deductible and there are only 50 units, your share is $10,000. Ensuring your HO-6 policy has robust Loss Assessment limits is a sophisticated way to prevent a single storm from draining your savings.

Personal Property and Interior Improvements

When selecting coverage, you must choose between "Actual Cash Value" and "Replacement Cost" for your belongings. We strongly recommend Replacement Cost, which pays to buy a new version of your items rather than a depreciated value. This distinction is especially important for interior improvements. If you've installed granite countertops or custom hardwood floors, these upgrades are your responsibility, not the association's. To protect these investments, you should:

Maintain a detailed digital home inventory with photos and receipts.

Specifically schedule high-value items like jewelry or fine art on your policy.

Update your coverage limits immediately following any significant interior renovation.

By treating your HO-6 policy as a precisely engineered component of your overall risk management, you ensure that the gaps left by the association don't become financial pitfalls.

Strategic Steps to Auditing Your Florida Condo Protection

Auditing your coverage is a rigorous necessity for any owner seeking long-term financial stability in the 2026 market. You need a systematic approach to compare your condo insurance vs HOA policy Florida to ensure no technicalities leave you exposed. Start by requesting the Certificate of Insurance (COI) from your association board. This single page provides a high-level summary of the association's carrier, coverage limits, and critical deductible structures. It allows you to see the exact figures you are working against when building your personal defense.

Once you have the COI, your next step involves a deep dive into your Covenants, Conditions, and Restrictions (CC&Rs). This is where the legal "duty to repair" is defined. You must identify the Master Policy deductible amount, which in Florida often ranges from $15,000 for small buildings to millions for coastal high-rises. Your goal is to align your HO-6 Loss Assessment limit with these figures. If the association faces a massive deductible after a storm, your personal policy should be engineered to absorb your portion of that cost. Don't wait for a special assessment notice to arrive in your inbox to find out your coverage is inadequate.

Reading the Fine Print in Your CC&Rs

Look specifically for the "Insurance" section in your association documents. You are searching for keywords like "primary coverage" and "subrogation." These terms dictate which policy pays first during a claim. Understanding the association's duty to repair common elements versus your duty to insure the interior is the only way to prevent expensive overlaps or dangerous voids. You should also verify that the association has completed its mandatory three year appraisal as required by Florida Statute 718.111, which ensures the building is insured to full replacement value.

The Hurricane Factor: Evaluating Windstorm Coverage

Standard fire or theft deductibles are usually flat dollar amounts, but hurricane deductibles in Florida are almost always percentages of the total insured value. This can result in a significant financial gap if you haven't planned for it. Additionally, many owners on higher floors ignore flood insurance, assuming they are safe from rising water. However, flood policies often cover damage that standard HO-6 policies exclude, such as hydrostatic pressure or specific types of wind-driven rain. Proactive risk mitigation before the season begins is your best defense.

Navigating these technical details requires a calm, analytical partner. You should consult with a specialized Florida insurance advisor to verify that your personal policy is perfectly calibrated to the association's master plan and the current regulatory environment.

SI Insurance: Engineering Personalized Security for Florida Homeowners

In a marketplace defined by volatility and shifting regulations, finding a partner who prioritizes precision over generic solutions is essential for your peace of mind. SI Insurance operates as a calm, calculated consultant in the specialized field of Florida risk management. We understand that the technical divide between condo insurance vs HOA policy Florida isn't just a matter of legal compliance; it's the foundation of your financial security. Our elite agents, particularly those serving Broward County and the broader Florida coastline, possess the deep technical expertise required to navigate these high-stakes environments with intellectual confidence. This level of specialization allows us to interpret the nuances of your specific association's coverage with a degree of accuracy that generalist agencies often lack.

We don't believe in one-size-fits-all products. Instead, we focus on the alignment of your personal goals with the specific structural realities of your residence. By meticulously analyzing your association's master policy, we craft a bespoke HO-6 strategy that acts as a protective shield for your interior assets and personal liability. This methodical approach ensures that your coverage is a precisely engineered financial structure rather than a reactionary purchase. We're committed to your long-term stability, providing a sense of absolute security that allows you to focus on the life you've built without the constant fear of a coverage gap.

A Methodical Approach to Florida Risk

Choosing an independent agency provides you with a distinct strategic advantage. We maintain relationships with multiple high-level carriers, allowing us to compare sophisticated financial structures and technical mitigation strategies on your behalf. This process reflects a commitment to corporate elegance, where every recommendation is based on rigorous data and a thorough understanding of the 2026 insurance climate. By leveraging these elite carrier networks, we can identify coverage options that are not publicly advertised but are perfectly suited for high-value condominium units. If you're ready for a more disciplined look at your protection, we invite you to experience a rigorous analysis of your current coverage at SI Insurance. We'll help you identify the subtle gaps that others often overlook.

Protecting Your Lifestyle, Not Just Your Property

Your needs often extend beyond the walls of your condominium. We treat insurance as a holistic financial tool designed to safeguard your entire lifestyle from unforeseen disruptions. Whether you require a sophisticated plan for your primary residence or a comprehensive Florida auto insurance policy, our team ensures that every component of your risk profile is balanced and secure. This elite level of service is engineered for those who demand foresight and stability in a complex world. We're here to act as your seasoned consultants, providing the clarity you need to move forward with absolute security. There is a distinct power in knowing your assets are protected by a methodology that prioritizes long-term resilience over short-term savings. Reach out today for a sophisticated consultation tailored to your high-value needs.

Securing Your Financial Future in the Florida Sun

Achieving absolute security in your home requires moving beyond a surface-level understanding of your association's protections. You've seen how the technical divide between condo insurance vs HOA policy Florida defines your personal liability; it also dictates how effectively you can recover after a major storm. By auditing your governing documents and aligning your personal limits with the association's deductible structure, you can replace confusion with intellectual confidence. Protecting your lifestyle is a collaborative effort between the building's master plan and your own carefully engineered policy.

Our team at Si Insurance Agency is founded on rigorous technical mastery and a commitment to elite risk management. As specialized Florida risk consultants, we offer access to elite carrier networks tailored to the unique demands of the current market. We're here to act as your protective guardian, ensuring no detail is left to chance. Request a meticulous review of your Florida condo coverage with Si Insurance Agency to verify that your assets are fully shielded. You've worked hard for your home, and we're dedicated to helping you keep it secure.

Frequently Asked Questions

Does my Florida condo association insurance cover water damage from a neighbor’s unit?

Your association’s master policy typically restores the building's structural components, but it won't cover your personal belongings or interior upgrades damaged by a neighbor's leak. While the master policy handles the "common elements" like the pipes inside the walls, you're responsible for your own flooring, furniture, and cabinetry. It's often necessary to file a claim through your personal HO-6 policy to ensure your interior finishes are repaired to their previous standard.

What is the difference between a Bare Walls and an All-In master policy in Florida?

A Bare Walls policy limits the association’s responsibility to the building’s collective structure and common areas, whereas an All-In policy extends coverage to include original interior fixtures like standard cabinetry and appliances. In the current market, most Florida associations opt for Bare Walls to manage their rising premiums. This shift makes it vital to understand your condo insurance vs HOA policy Florida requirements so you don't leave your kitchen or bathroom finishes unprotected.

How much Loss Assessment coverage do I really need for a Florida condo?

The ideal amount of Loss Assessment coverage depends entirely on your association’s master policy deductible, which often necessitates limits far higher than the standard $1,000 offerings. If your building has a 3% hurricane deductible on a $20 million valuation, the total deductible is $600,000. If that cost is split among 60 owners, you'd be responsible for $10,000. We recommend matching your coverage to your potential share of the association's highest possible deductible.

Is flood insurance required if I live on a high floor in a Florida condo building?

Flood insurance isn't always federally mandated for units on high floors, but it's a strategic necessity because standard policies don't cover damage from rising water. Even if the water doesn't reach your floor, a flood can devastate the building's lobby, elevators, and electrical systems. When the association's master flood policy is insufficient to cover these repairs, you could face a special assessment that only a personal flood policy would typically cover.

Can my association force me to buy personal condo insurance (HO-6)?

Yes, your association's governing documents or your mortgage lender can absolutely require you to maintain a personal HO-6 policy. Most Florida bylaws now include this mandate to ensure that individual owners can cover their own deductibles and interior repairs after a disaster. This requirement protects the community's overall financial health by preventing abandoned, damaged units that the association cannot afford to fix on its own.

What happens if my association’s master policy deductible is higher than my savings?

If the association’s deductible exceeds your liquid savings, you could face a significant financial burden unless your personal policy includes robust Loss Assessment coverage. When a major claim occurs, the association will likely levy a special assessment against all unit owners to cover that deductible gap. Without the right insurance bridge in place, you'd be personally liable for that payment, which could lead to liens against your property if left unpaid.

Does condo insurance cover my belongings if they are stolen from a common area?

Your personal HO-6 policy generally provides coverage for your belongings even when they're located in common areas like the gym, lobby, or pool deck. This "off-premises" protection is a standard feature of most high-quality policies, though it's often subject to a specific limit, such as 10% of your total personal property coverage. It's a vital safety net for residents who utilize shared amenities frequently.

How do Florida’s recent building safety laws affect my condo insurance rates?

Florida’s recent building safety laws have led to increased premiums as carriers gain a clearer picture of a building’s structural health through mandatory milestone inspections. These regulations, effective as of 2024 and 2025, require associations to be more transparent about their maintenance and reserves. While this data helps stabilize the market long-term, the immediate result is often higher costs for buildings that have deferred maintenance. Understanding the interplay of condo insurance vs HOA policy Florida is now more important than ever as these costs are passed to owners.

Comments