Florida Hurricane Deductible Explained: A Strategic Guide for 2026

- siinsuranceflorida

- 3 days ago

- 13 min read

If your home is insured for $500,000, a standard 5% hurricane deductible means you're personally responsible for the first $25,000 in damages before your policy provides any relief. It's a staggering figure that often catches residents off guard, yet having the Florida hurricane deductible explained through a strategic lens can transform this financial hurdle into a manageable part of your risk portfolio. Most homeowners find the distinction between "All Other Perils" and "Hurricane" deductibles confusing, particularly when facing the reality that out-of-pocket costs can range from 2% to 10% of their home's total value.

We understand that managing high-value assets requires a calculated approach, and you deserve to feel secure in your financial foresight. By reading this guide, you'll master the complexities of these requirements to protect your property and finances with absolute confidence. We'll examine the "Calendar Year" rule that limits your exposure across multiple storms, clarify the 72 hour window that triggers your coverage, and provide a clear framework for choosing a deductible percentage that fits your 2026 financial strategy.

Key Takeaways

Learn to distinguish between standard "All Other Perils" and specific hurricane triggers to ensure your claims are filed under the correct financial terms.

Discover how Coverage A acts as the anchor for your out-of-pocket costs with the Florida hurricane deductible explained as a vital part of your financial protection.

Master the "Calendar Year" rule to understand how Florida law prevents policyholders from paying multiple full deductibles during a single active storm season.

Weigh the benefits of lower premiums against your available cash to decide if a 2%, 5%, or 10% deductible is the right fit for your household.

Find out why a local independent agency is your best ally for accessing diverse carrier options and expert guidance when a major storm hits.

Table of Contents

The Mechanics of the Florida Hurricane Deductible

Understanding the financial architecture of your property protection starts with recognizing that not all wind damage is treated equally under Florida law. While standard Homeowners insurance policies typically utilize a flat dollar amount for most claims, the state mandates a specific percentage-based structure for hurricanes to ensure market stability during catastrophic events. This distinction is vital because the moment a storm receives a formal designation from the National Hurricane Center (NHC), your financial responsibility can shift from a few thousand dollars to a significant portion of your home's total value.

To better understand how these triggers impact your recovery and out-of-pocket costs, watch this helpful breakdown:

When Does the Hurricane Deductible Apply?

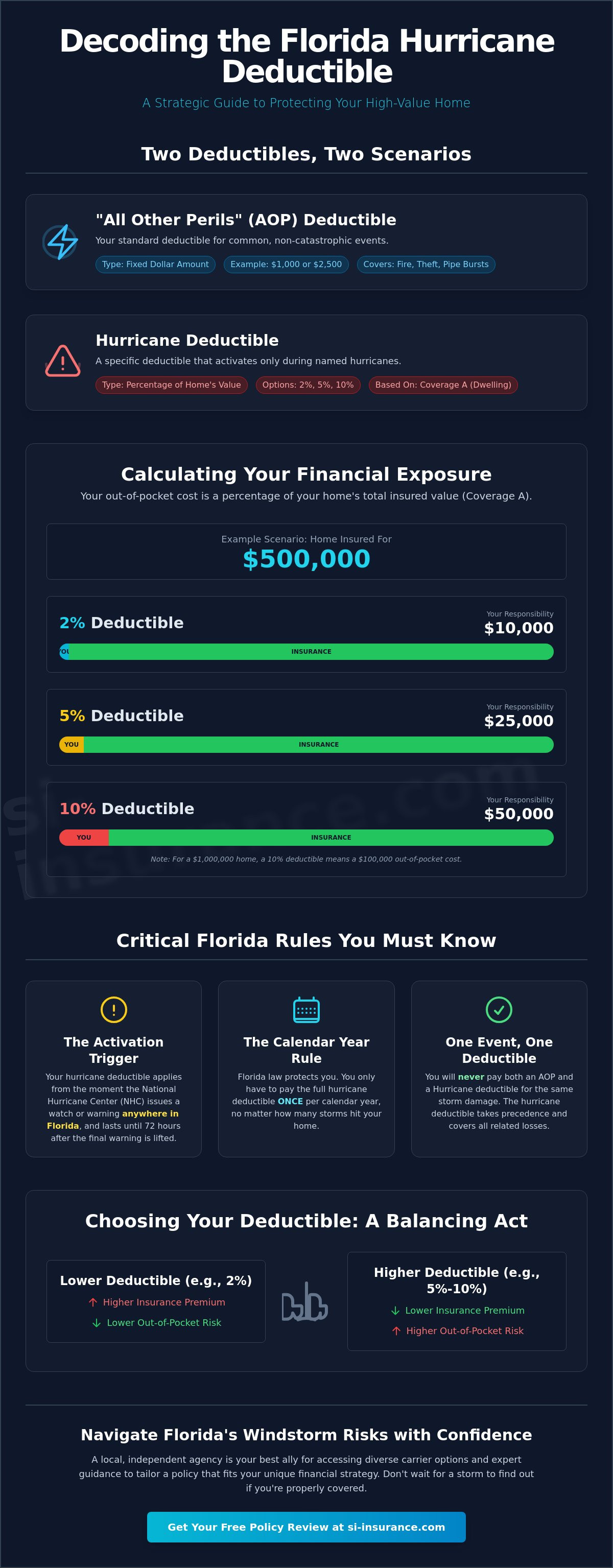

The legal activation of this deductible is tied directly to the National Hurricane Center. The clock starts the moment the NHC issues a hurricane watch or warning for any part of Florida. It's a common misconception that the storm must make landfall near your specific Broward County property for the trigger to occur. In reality, a warning issued for the Panhandle can activate the hurricane provisions for a policyholder in South Florida. This specialized deductible remains in effect through the duration of the storm and for a full 72 hours after the final hurricane watch or warning is lifted anywhere in the state. If a system is classified only as a "Tropical Storm" when it passes your home, your standard deductible usually applies, provided no hurricane warnings were active in Florida at that time.

Hurricane vs. All Other Perils (AOP)

Your policy is essentially divided into two distinct risk categories. The "All Other Perils" (AOP) deductible serves as the primary baseline for non-catastrophic losses. This covers everyday risks such as fire, theft, or a sudden pipe burst. These are usually fixed amounts, like $1,000 or $2,500, which are easier to manage in a household budget. Having the Florida hurricane deductible explained means recognizing that this secondary, percentage-based figure only "wakes up" for major events.

A critical protection for homeowners is the "one deductible" rule. You'll never be forced to pay both an AOP and a hurricane deductible for the same incident. If a major storm causes wind damage that leads to a fire, the higher hurricane deductible typically takes precedence, but it won't be stacked on top of your AOP amount. This hierarchy ensures that while your exposure is higher during a hurricane, it remains capped at a single, predictable percentage of your dwelling coverage.

Calculating the Percentage: What You Really Owe

The transition from traditional flat-dollar deductibles to percentage-based structures represents a fundamental shift in how risk is shared between the homeowner and the carrier. While a standard fire or theft claim might involve a predictable $1,000 or $2,500 cost, having the Florida hurricane deductible explained means looking at your Coverage A, or Dwelling limit, as the primary anchor for all calculations. This figure represents the estimated cost to rebuild your home from the ground up, and it's this total value that determines your out-of-pocket responsibility during a named storm. As property values in areas like Pompano Beach have surged, the corresponding deductible amounts have also climbed, making it essential to understand the math behind your policy's declarations page.

Consider a typical single-family home in Pompano Beach insured for $500,000. Under a standard 2% hurricane deductible, your financial exposure for a single event is $10,000. If you've opted for a 5% deductible to lower your monthly premiums, that responsibility jumps to $25,000. It's a significant sum that requires proactive liquidity planning. For those managing high-value estates insured for $1,000,000 or more, a 10% deductible creates a $100,000 "self-insured" gap that must be bridged before the carrier contributes a single dollar to the reconstruction. Understanding The Mechanics of the Florida Hurricane Deductible is a critical step in ensuring your personal risk management strategy aligns with your actual financial capacity.

Percentage Options and Their Impact

Florida law requires insurers to offer specific options, usually 2%, 5%, and 10%, though a $500 flat option must be available for homes insured for less than $250,000. In high-risk coastal zones, many carriers have moved toward a mandatory 5% minimum to maintain underwriting excellence. This strategic alignment between the carrier and the policyholder ensures that the insurance pool remains solvent even after a catastrophic season. Choosing a higher percentage can significantly reduce your annual premium, but it functions as a form of self-insurance. If you're unsure how these figures align with your current liquid reserves, reviewing your homeowners insurance policy with a professional can provide the clarity you need.

Real-World Math Examples

The way this money changes hands is a common point of confusion. You don't actually write a check to your insurance company when you file a claim; instead, the deductible is subtracted from the final claim payout issued by the carrier. For example, if a $300,000 home with a 2% deductible ($6,000) sustains $50,000 in wind damage, the insurance check will be for $44,000. For HO-6 condo owners, the math is slightly different as the deductible applies only to the "walls-in" coverage and loss assessment, rather than the entire building structure. HO-4 renters are typically exempt from these high percentage-based triggers, as their policies focus on personal property rather than the dwelling itself.

The Florida Calendar Year Hurricane Deductible Rule

One of the most significant legal protections for property owners is the "Calendar Year" provision. This rule prevents a single active season from becoming a compounding financial disaster. Having the Florida hurricane deductible explained means recognizing that you only have to satisfy that high percentage-based amount once between January 1st and December 31st. If your Sunrise, FL property suffers damage from two separate named storms in 2026, you aren't on the hook for two full deductibles. Once you've reached that threshold, any subsequent hurricane claims in the same year are subject only to your standard All Other Perils (AOP) deductible, which is typically a much smaller, flat dollar amount.

This protection creates a strategic advantage for those who track their expenditures meticulously. Even if a storm causes damage that falls below your total deductible limit, reporting the claim is essential. Your carrier will "credit" that amount toward your annual hurricane deductible. For instance, if a $10,000 deductible is in place and the first storm causes $4,000 in covered damage, your remaining responsibility for the next hurricane that year drops to $6,000. Without a formal claim on file, you lose the ability to prove that this initial "burn down" occurred.

Managing Multiple Storms Strategically

Filing a claim for minor damage might feel counterintuitive, but it's a calculated move for long-term risk mitigation. If a late-season storm hits in November, you'll be glad you documented the smaller losses from August. Documentation is your strongest asset here. Keep every receipt, contractor estimate, and photo from the first event to ensure your insurer has an airtight record of your progress. It is also vital to remember that the clock resets every January 1st. A storm on December 31st counts for the current year, while a system arriving in early January starts the deductible requirement from scratch.

The Role of the Carrier Group

The continuity of your coverage is the "glue" that holds this rule together. The calendar year protection only applies if you stay with the same insurance company or a company within the same carrier group. If you switch policies mid-season, you'll likely face a fresh hurricane deductible with your new provider. This makes mid-summer policy changes a high-stakes gamble. If you must move your coverage, do so with a clear understanding of your current "deductible credit" and how a new homeowners insurance policy will reset your financial exposure.

Strategic Risk Management: Choosing Your Deductible Percentage

Deciding on a specific percentage for your windstorm coverage is far more than a simple clerical choice; it's a high-stakes decision in strategic asset management. While a 10% deductible might seem attractive for its ability to lower annual premiums, you must evaluate this against your actual liquid cash reserves. Having the Florida hurricane deductible explained in a financial context means acknowledging that you're essentially choosing how much risk you're willing to self-insure. If a storm causes $50,000 in damage and your deductible is $30,000, you need to be certain that this capital is readily available without disrupting your broader investment portfolio or emergency funds.

SI Insurance acts as a strategic guardian in this process, helping you navigate the "Premium vs. Protection" debate with rigorous analysis. We look at your total risk profile to ensure you aren't over-insured on your monthly premiums while remaining dangerously under-prepared for the actual deductible event. Your emergency fund planning should treat the maximum hurricane deductible as a mandatory, non-negotiable cash reserve. This approach ensures that when a catastrophic event occurs, your focus remains on recovery and reconstruction rather than liquidity crises.

Risk Tolerance vs. Financial Capacity

Your personal risk tolerance must be balanced against the rigid requirements of your financial partners. Most mortgage lenders in Florida impose strict caps on deductible percentages, often refusing to accept anything higher than 5% or 10% to protect their collateral. For high-net-worth individuals with significant property portfolios, bespoke solutions may be required to align multiple policies under a cohesive risk transfer strategy. It's about finding the "sweet spot" where your monthly cash flow is optimized without exposing your estate to an unmanageable financial shock. If you're ready to refine your coverage, consult with our risk managers to find your ideal balance.

Mitigation as a Financial Hedge

Investing in your home's physical resilience is perhaps the most effective way to manage your deductible risk. By installing impact-resistant windows or reinforcing your roof to 2026 building standards, you significantly lower the probability of a claim ever reaching that high hurricane threshold. This creates a powerful strategic link: home hardening allows you to comfortably select a higher deductible, knowing your structure is built to withstand the pressure. For a deeper dive into these protections, explore our Home Insurance in Florida: A Strategic Guide. These upgrades don't just protect your family; they function as a financial hedge that preserves your capital during the most volatile weather events.

Navigating Florida’s Windstorm Risks with SI Insurance

Managing the complexities of windstorm coverage requires more than just a basic policy; it demands a partner who operates with the precision of a seasoned risk manager. Having the Florida hurricane deductible explained is merely the first step toward securing your home against the unpredictable nature of the Atlantic storm season. The true value lies in the meticulous policy analysis and strategic alignment that only an independent agency can provide. At SI Insurance, we don't just offer standard coverage; we provide a bespoke risk transfer approach that ensures your dwelling, personal property, and liability are protected through a lens of underwriting excellence.

Unlike captive agents who are restricted to a single carrier’s appetite, our status as an independent agency allows us to access a diverse range of high-value carriers across the state. This flexibility is essential in a volatile market like Florida's, where underwriting guidelines and capacity can shift overnight. We act as your strategic guardian, scouring the market to find the most favorable terms for your specific deductible needs and risk tolerance. This intellectual confidence allows you to rest easy, knowing that your financial risk is being managed by experts who prioritize long-term stability and elite expertise over off-the-shelf solutions.

Local Expertise in Sunrise and Pompano Beach

Our deep roots in Broward County provide us with an intimate understanding of the specific wind-pool requirements and building codes unique to South Florida. Whether your property is situated in the heart of Sunrise or along the vulnerable coastline in Pompano Beach, we understand the local nuances that impact your premiums and deductible options. We serve as your seasoned consultant throughout the entire lifecycle of your policy, especially during the high-stakes claim process following a major weather event. For those seeking a partner with a permanent local presence, SI Insurance: Your Local Agent in Broward County is ready to provide the professional guidance you require.

Securing Your Strategic Guardian

The complex financial landscape of Florida insurance demands a calculated approach to personal security that moves beyond simple price comparisons. Initiating a comprehensive policy review with our elite team is the most effective way to ensure your current coverage isn't leaving you exposed to unnecessary out-of-pocket costs during a catastrophic season. We invite you to experience a calculated approach to personal security that focuses on rigorous analysis and "white-glove" service. By aligning your deductible strategy with your broader financial goals, we help you achieve a state of absolute security. Reach out to SI Insurance today to begin your bespoke risk assessment and secure your property for the 2026 season and beyond.

Securing Your Financial Future for the 2026 Storm Season

Protecting your home requires a blend of physical resilience and intellectual foresight. We've explored how the calendar year rule limits your exposure and why your choice of a 2% or 10% deductible must align with your actual cash reserves. Having the Florida hurricane deductible explained is just the foundation for a robust risk management plan. Since our founding in 2022, SI Insurance has served as a strategic guardian for residents across Broward County, offering the bespoke risk transfer solutions that only an independent agency can provide.

Our team brings elite expertise to both personal and commercial strategic risk management, ensuring your coverage is never a matter of chance. It's time to replace confusion with a calculated approach to your property's security. Take the next step in securing your legacy and Request a Strategic Policy Review from SI Insurance today. You've worked hard to build your life in the Sunshine State; we're here to help you protect it with absolute confidence.

Essential Insights on Florida Hurricane Deductibles

What is the difference between a named storm and a hurricane for insurance purposes?

A hurricane deductible is specifically triggered by a National Hurricane Center watch or warning, whereas a named storm deductible applies to any system with a name, such as a tropical storm. In Florida, the legal trigger is very precise; it starts when a hurricane watch or warning is issued for any part of the state and ends 72 hours after the final warning is lifted. This distinction ensures your financial responsibility is tied to a specific, catastrophic weather event rather than every summer squall.

Can I choose a flat-dollar deductible instead of a percentage in Florida?

You can only choose a flat $500 deductible if your home is insured for less than $250,000, as Florida law mandates percentage options for most properties. For dwellings valued above that threshold, insurers must offer choices of 2%, 5%, or 10% of your structure's total limit. This percentage-based approach is a core part of the Florida hurricane deductible explained, serving as a strategic risk-sharing tool that keeps the broader insurance market stable during active seasons.

What happens if I have two hurricane claims in the same year?

If you face two separate hurricane claims in 2026, the Florida Calendar Year Hurricane Deductible rule protects you from paying the full percentage twice. Once you've satisfied the hurricane-specific amount during the first storm, any subsequent hurricane damage that same year is subject only to your lower All Other Perils deductible. It's a vital protection that prevents a single active season from becoming a compounding financial burden on your household or business reserves.

Does my mortgage company limit how high my hurricane deductible can be?

Your mortgage lender definitely has a say in your deductible selection, as they need to ensure the property can be repaired quickly to protect their investment. Most lenders in Florida cap hurricane deductibles at 5% or 10% of the dwelling's value, and they won't allow you to go higher even if you want to lower your premium. It's a strategic alignment between you and your bank that ensures you don't take on more out-of-pocket risk than you can actually handle.

Is flood damage covered under my hurricane deductible?

No, flood damage is never covered under your standard hurricane deductible, regardless of how the storm is classified. Standard homeowners policies exclude rising water, storm surge, and overflow from bodies of water. To protect your home from these specific risks, you must secure a separate flood insurance policy. Relying on a windstorm deductible to cover water intrusion from the ground up is a dangerous gap in any risk management strategy.

How do I find my hurricane deductible amount on my policy documents?

You'll find your hurricane deductible clearly listed on your policy's Declarations Page, which is usually the first or second document in your policy packet. Florida law requires insurers to display this amount as both a percentage of your dwelling coverage and as a specific dollar figure. Seeing the exact dollar amount helps you plan your emergency fund with precision, ensuring you aren't guessing about your potential out-of-pocket costs when a storm approaches.

Why is my hurricane deductible so much higher than my standard deductible?

Your hurricane deductible is significantly higher because it's calculated as a percentage of your home's total replacement cost rather than a flat fee. While a standard deductible might be $1,000 for a fire, a 2% hurricane deductible on a $400,000 home is $8,000. This structure allows carriers to offer more affordable annual premiums by shifting a portion of the catastrophic risk to the homeowner, which is a standard practice in high-risk coastal environments.

Can I change my hurricane deductible percentage during hurricane season?

You can request a change to your deductible percentage mid-season, but carriers often place a "binding moratorium" as soon as a storm enters a specific geographic box. It's also important to remember that switching carriers to find a better rate mid-season will reset your calendar year deductible to zero. We recommend a strategic review of your limits well before June 1st to ensure your underwriting excellence is locked in before the weather becomes a factor.

Comments