Does Home Insurance Cover Flood Damage in Florida? A Strategic Guide for 2026

- siinsuranceflorida

- 10 hours ago

- 14 min read

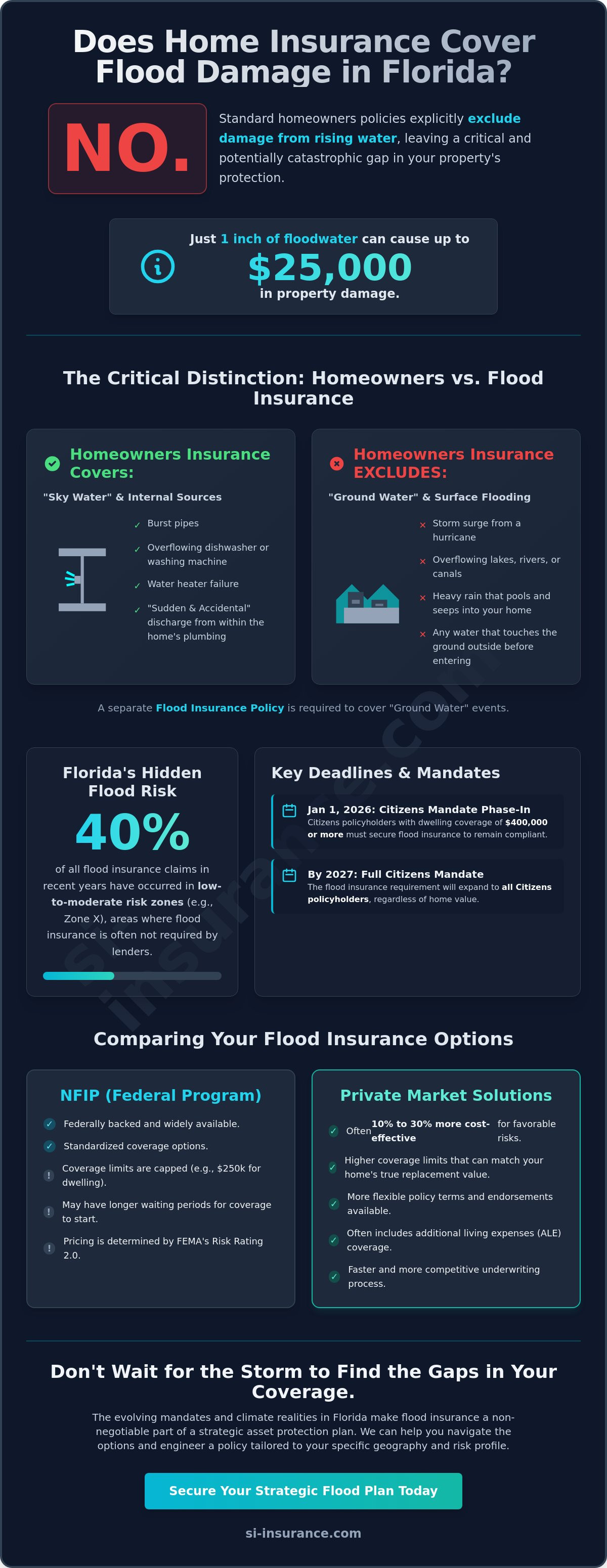

FEMA reports that a single inch of water can cause up to $25,000 in damage to your property, yet many residents remain dangerously exposed because they assume their primary policy provides a safety net. The reality is that the question "does home insurance cover flood damage in Florida" has a definitive, albeit unsettling, answer; it does not. Standard homeowners insurance excludes rising water, leaving a strategic gap in your risk mitigation plan that could lead to catastrophic out-of-pocket expenses during a storm event.

You likely recognize that protecting a Florida asset requires foresight, but the complexity of shifting mandates and private market alternatives can feel overwhelming. At SI Insurance, we believe that intellectual confidence comes from knowing your coverage is meticulously engineered for your specific geography. This guide will provide a clear strategy to meet the January 1, 2026, Citizens flood mandate and help you evaluate whether private market solutions, which are often 10% to 30% more cost-effective for favorable risks, align with your financial goals. We'll examine the evolving landscape of FEMA Risk Rating 2.0 and the October 1, 2025, disclosure laws to ensure your property remains a secure investment.

Key Takeaways

Understand why the answer to the question "does home insurance cover flood damage in Florida" is a firm no; you'll learn how to bridge this gap with a separate, targeted policy.

Master the technical distinction between ground water and sky water so you're never caught off guard by a denied claim after a storm.

Compare the federal NFIP program against the surging private market to find higher coverage limits that actually reflect your home's replacement value.

Identify how the 2026 Citizens mandate affects your specific coverage requirements and what you must do to remain compliant by the January deadline.

Leverage the data from FEMA's Risk Rating 2.0 to build a strategic mitigation plan that protects your equity while lowering your long-term insurance costs.

Table of Contents

The Critical Distinction Between Homeowners Insurance and Flood Coverage in Florida

Many homeowners in the Sunshine State view their insurance policy as a comprehensive shield. However, a significant gap exists that often only becomes visible during a catastrophe. To put it simply, if you're asking "does home insurance cover flood damage in Florida," the answer is a categorical no. Your standard HO-3 or HO-5 policy is designed to address internal malfunctions. This includes a burst pipe in the kitchen or a water heater failure. It stops short the moment water touches the ground outside your home before entering. This distinction isn't just a technicality; it's the legal boundary between a fully funded recovery and financial ruin.

Determining whether does home insurance cover flood damage in Florida requires a look at your policy's fine print, where you'll likely find that "water damage" and "flood" are treated as two entirely different perils. To better understand how these policies diverge in the real world, watch this helpful breakdown:

The 'Rising Water' Exclusion Explained

The insurance industry uses a specific threshold to determine if a claim is a homeowners issue or a flood event. If water originates from the ground up, it's classified as "surface water." This includes an overflowing lake, a storm surge, or heavy rain that can't drain fast enough. This classification triggers the flood exclusion in your primary policy. "Sudden and accidental" discharge refers to water that was already inside your plumbing system. If your dishwasher overflows, you're covered. If the street floods and that water seeps through your front door, your homeowners policy will deny the claim. This surface water rule is the most common reason for denied claims after a Florida hurricane.

Why Florida Homeowners Are Often Underinsured

A dangerous psychological trap persists among residents living in "Zone X" or other areas not traditionally labeled as high-risk. Data reveals that over 40% of flood claims occur in these supposedly safe zones. Relying on federal disaster assistance is a flawed strategy. These funds are often provided as low-interest loans rather than grants. This adds debt to an already stressful situation. The flood disclosure law that took effect on October 1, 2025, now requires sellers to be transparent about water history, but awareness doesn't equal protection. As the National Flood Insurance Program (NFIP) continues to adjust its rates under Risk Rating 2.0, the necessity of a standalone policy becomes clearer.

The 2026 Florida insurance market has shifted toward mandatory coverage for many. For instance, as of January 1, 2026, Citizens Property Insurance Corporation requires all policyholders with dwelling coverage of $400,000 or more to carry flood insurance. This requirement will expand to all policyholders by 2027. At SI Insurance, we view flood coverage as a mandatory companion to your primary asset protection plan. We focus on bespoke risk transfer that accounts for your home's specific elevation and local drainage infrastructure.

Identifying What Counts as 'Flood Damage' Under Florida Statutes

When you're trying to figure out does home insurance cover flood damage in Florida, the legal definition of a "flood" is your most important benchmark. Under the guidelines established by FEMA, a flood is officially recognized as a general and temporary condition of partial or complete inundation of two or more acres of normally dry land area or of two or more properties. This specific "two-property" rule is what insurance adjusters use to distinguish a localized plumbing failure from a statutory flood event. If your home is the only one on the block with water in the foyer, and the street itself is dry, you're likely dealing with a maintenance issue rather than a flood claim.

The distinction between ground water and sky water is where many Florida residents find themselves in a complex legal landscape. Florida courts often rely on the "efficient proximate cause" doctrine to resolve disputes. This doctrine seeks to identify the primary event that set the damage in motion. If a storm surge pushes water into your living room, the source is the ground, and it's a flood. However, if a hurricane winds rip a hole in your roof and rain pours in, the source is the sky. Understanding these nuances is vital when comparing NFIP and private flood insurance options, as different policies may offer varying levels of clarity on these definitions.

Wind-Driven Rain vs. Rising Surge: The Gray Area

The most common conflict in Florida insurance claims involves the "point of entry" for water during a hurricane. Wind-driven rain is a peril typically covered under the windstorm portion of a Florida homeowners policy. This occurs when high-velocity winds force rain through windows, doors, or damaged roofing. Conversely, a storm surge is rising water pushed inland by the same winds, which is strictly a flood event. If your home experiences both, adjusters will meticulously examine the water line to determine which peril caused which specific damage. Documenting the sequence of events is a strategic necessity to ensure your claims are processed accurately.

The Two-Acre Rule and Partial Inundation

Proving that a flood legally occurred requires more than just showing a wet carpet. Adjusters look for a "general condition of flooding" in your immediate area. If the inundation covers at least two acres or affects a neighboring property, the event meets the statutory threshold. For homes with crawlspaces or walk-out basements, partial inundation can be particularly tricky to prove without proper evidence. We recommend using your smartphone to capture time-stamped photos of the street, your yard, and your neighbors' properties during the event. This documentation serves as an objective record that helps our team at SI Insurance advocate for your bespoke risk transfer needs during the underwriting or claims process.

Comparing the National Flood Insurance Program (NFIP) and Private Flood Markets

The choice between federal backing and private innovation represents a critical decision in your risk management strategy. While we've established that the answer to "does home insurance cover flood damage in Florida" is a definitive no, the secondary question is which specific flood vehicle provides the most airtight protection for your assets. Historically, the federal government was the only viable provider. By early 2026, however, the private market has matured significantly, now accounting for approximately 35% of all flood policies in the state. This shift provides homeowners with sophisticated alternatives that often outperform federal standards for high-value properties.

When residents ask does home insurance cover flood damage in Florida, they are often surprised to learn that even if they have the best homeowners policy, they still need to navigate the nuances between these two distinct markets. The National Flood Insurance Program (NFIP) is a standardized system, but its rigid structure may not align with the needs of modern, high-value Florida estates. Choosing between them requires a calculated look at your specific risk profile and the total replacement value of your property.

NFIP: The Federal Safety Net

The NFIP remains a foundational safety net, especially for those in high-risk zones where private carriers might be more selective. These policies are often managed through "Write Your Own" (WYO) companies, which act as administrative intermediaries. While the federal government backs the claim, a private carrier handles the paperwork and distribution. However, the $250,000 building and $100,000 contents caps are often inadequate. It's also vital to remember that home insurance in Florida serves as your primary shield for non-flood perils, such as fire or theft, but it won't bridge the gap if a flood claim exceeds these federal limits. NFIP policies typically use "Actual Cash Value" for contents. This factors in depreciation, potentially leaving you with a significant financial shortfall during the recovery process.

The Growth of Private Flood Carriers in Florida

Private flood insurance has expanded rapidly because it offers bespoke solutions that the federal program cannot match. These carriers use advanced satellite imagery and granular elevation data to price risk with surgical precision, often resulting in premiums that are 10% to 30% lower for properties with favorable risk characteristics. Unlike the NFIP's 30-day waiting period, private options often feature much shorter windows; some policies take effect in as little as 10 to 14 days. For our clients at SI Insurance, the most attractive feature is "Excess Flood" coverage. This allows you to stack additional protection on top of an NFIP policy, ensuring that a multi-million dollar home is fully indemnified rather than being capped at the federal limit. This layer of modern financial engineering is what distinguishes a standard policy from a truly strategic defense.

Determining Your Risk Profile and Mortgage Requirements

Understanding the technical parameters of your property's risk is the first step toward securing a stable financial future. Many residents mistakenly ask "does home insurance cover flood damage in Florida" only when a closing date is imminent or a storm is brewing. By then, the options for strategic risk transfer may be limited by federal waiting periods or lender mandates. Your risk profile isn't just a label on a map; it's a dynamic data point that determines your eligibility for certain private markets and the total cost of your annual premiums.

Lenders for federally backed mortgages are legally obligated by the Flood Disaster Protection Act to require flood insurance for properties located in Special Flood Hazard Areas (SFHA). These high-risk zones, often labeled as "A" or "V" on FEMA maps, carry a mandatory purchase requirement. Even if you don't live in a high-risk zone, the reality that does home insurance cover flood damage in Florida is a firm "no" means that a voluntary policy is often the most prudent move to protect your equity. At SI Insurance, we help you navigate these requirements with a focus on long-term asset security rather than just meeting a minimum checklist.

Understanding FEMA Maps and Risk Rating 2.0

The traditional "100-year flood" terminology has become an outdated metric for modern risk management. FEMA's Risk Rating 2.0 represents a fundamental shift from broad, zone-based pricing to a model that evaluates the specific characteristics of your individual property. This methodology considers your home's proximity to various water sources, the cost to rebuild, and the specific ground elevation of the structure. In 2026, this precision allows for more accurate underwriting, ensuring that homeowners aren't overpaying for generalized risks while providing a clearer picture of their true exposure. It's a move toward underwriting excellence that rewards proactive mitigation.

When Your Lender Mandates Coverage

If your property is remapped into a high-risk zone mid-mortgage, your lender will send a notification requiring you to secure a flood policy immediately. There's a common myth that "grandfathering" protects you from rate increases indefinitely, but under current regulations, those rates will eventually align with the full risk-based premium. Managing these shifting requirements is part of a broader strategy. Just as you might consult our Florida auto insurance guide to streamline your vehicular risks, your property coverage should be viewed as one component of an integrated risk management plan. To lower your costs strategically, consider investing in an elevation certificate or installing FEMA-compliant flood vents. These physical improvements provide tangible data that can lead to significant premium reductions under the current risk-based pricing models.

Are you ready to see how your specific elevation impacts your options? Contact an SI Insurance consultant today for a comprehensive risk assessment tailored to your property's unique data profile.

Securing a Strategic Flood Mitigation Plan with Si Insurance Agency

Navigating the complex waters of Florida's insurance market requires more than just a standard policy; it demands a calculated strategy. Since we've clarified that the answer to "does home insurance cover flood damage in Florida" is a definitive no, your focus must shift toward securing a bespoke risk transfer solution. At SI Insurance, we act as your strategic guardian, ensuring that your property's unique elevation and value are matched with the most robust coverage available in the 2026 market. We don't just provide off-the-shelf products. We engineer solutions that account for the high-stakes nature of coastal and inland property ownership.

Our approach involves a rigorous comparison of the NFIP and multiple private carriers to find the strategic sweet spot for your specific budget and risk profile. By integrating flood protection into your broader portfolio, we provide a sense of absolute security and intellectual confidence. Whether you're managing a single primary residence or a diverse real estate portfolio, our team ensures that your assets are protected against the unpredictability of the Florida climate through meticulous underwriting excellence.

The Benefits of Independent Agency Advocacy

An independent agent is your most powerful advocate because we aren't tethered to a single carrier's limitations. In Florida, this means we can access non-admitted and surplus lines markets that direct writers simply cannot reach. This access is critical for high-value assets that exceed the $250,000 building limit of the NFIP. Our commitment to meticulous policy analysis ensures no gaps exist between your homeowners policy and your flood coverage. This white-glove service model extends from your initial quote to strategic support during the claims process, positioning SI Insurance as a calm and calculated partner in a complex financial landscape.

Next Steps for Florida Residents

Timing is a functional component of risk mitigation. The NFIP's 30-day waiting period means that waiting for a storm to appear on the radar is a tactical error. We recommend that Florida residents act now to avoid being caught in a coverage gap during hurricane season. A comprehensive risk audit of your property can reveal opportunities for lower premiums through better risk assessment and physical mitigation. To begin this process, you should gather your current elevation certificate and any prior loss history reports for our team to review.

Request a comprehensive risk audit to identify specific vulnerabilities in your current coverage.

Compare private market high-limit options against federal caps to ensure full asset replacement.

Secure your policy at least 30 days before peak storm activity to satisfy federal waiting periods.

Protecting your investment requires foresight and elite expertise. Contact Si Insurance Agency for a strategic flood insurance evaluation and ensure your Florida property is shielded by a plan designed for long-term stability.

Strategic Resilience for Your Florida Property

Standard homeowners policies effectively address internal failures, but they stop at the threshold of rising water. Now that you've navigated the technical distinctions between wind-driven rain and statutory flooding, your path forward requires a shift from passive coverage to active risk management. Understanding that the definitive answer to does home insurance cover flood damage in Florida is "no" remains the first step in constructing a durable financial defense. With the private market now representing 35% of Florida's flood landscape, you have sophisticated options to protect high-value assets far beyond federal caps.

SI Insurance provides the underwriting excellence needed to align your home and flood policies into a single, cohesive shield. Our advocacy as an independent agency ensures you have access to top-rated carriers and bespoke risk transfer solutions that match your specific elevation data. You've worked hard to build your life in the Sunshine State, and your protection plan should reflect that same level of dedication and foresight. Secure your Florida home with a bespoke flood insurance strategy from Si Insurance Agency. We're here to help you move forward with absolute security and intellectual confidence.

Common Questions Regarding Florida Flood Coverage

Is flood insurance required by law in Florida for all homeowners?

Florida state law does not mandate flood insurance for every homeowner, but specific requirements from lenders and state-backed insurers create a de facto mandate for many. As of January 1, 2026, all Citizens Property Insurance Corporation policyholders with dwelling coverage of $400,000 or more must maintain a separate flood policy. Additionally, if your property is located in a Special Flood Hazard Area and you have a federally backed mortgage, your lender will require coverage to protect their collateral.

How much does the average flood insurance policy cost in Florida in 2026?

The average annual premium for a National Flood Insurance Program policy in Florida is approximately $1,363 for a single-family home. However, costs vary significantly based on your specific risk profile under FEMA's Risk Rating 2.0. For properties with favorable elevation and modern mitigation features, the private market often provides more competitive rates. We've seen private premiums that are 10% to 30% lower than federal options for homes located outside high-risk zones.

Can I buy flood insurance if I am already in the middle of a hurricane warning?

You can technically purchase a policy at any time, but it will not provide immediate protection for an approaching storm. The NFIP imposes a strict 30-day waiting period before a policy becomes active. While private carriers may offer shorter windows of 10 to 14 days, most insurers stop binding new coverage once a tropical storm or hurricane warning is officially issued for the region. Strategic planning requires securing coverage well before a threat appears on the radar.

Does my Florida condo insurance cover flood damage to my personal belongings?

No, your standard HO-6 condo policy excludes damage caused by rising surface water. While your condo association likely maintains a master policy for the building's structure, it rarely extends to the personal property inside your individual unit. To protect your furniture, electronics, and interior improvements, you must secure a separate flood policy. This is a critical gap for many residents who mistakenly assume "does home insurance cover flood damage in Florida" applies to their condo contents.

What is the difference between an NFIP policy and a private flood insurance policy?

The distinction lies primarily in coverage limits and the flexibility of the underwriting process. An NFIP policy is federally backed and capped at $250,000 for the building and $100,000 for contents. Private flood insurance is provided by corporate carriers and can offer multi-million dollar limits and replacement cost coverage for your belongings. Many homeowners find that the answer to does home insurance cover flood damage in Florida is best addressed through a private policy that offers higher protection than the federal program.

Will FEMA help me if I don't have flood insurance and my home floods?

FEMA disaster assistance is not a substitute for insurance and is often limited to low-interest loans that must be repaid. Grants for home repairs are only available if the President issues a Major Disaster Declaration, and these payouts are typically insufficient for full restoration. Data shows that federal disaster grants often average less than $10,000 per household. This is a fraction of the cost needed to repair the $25,000 in damage that just one inch of water can cause.

How do I know which flood zone my Florida property is located in?

You can determine your specific designation by accessing the FEMA Flood Map Service Center and entering your property address. Zones beginning with the letters A or V are classified as high-risk Special Flood Hazard Areas. If your property is in Zone X, it is considered moderate-to-low risk. It's vital to remember that over 40% of flood claims in Florida originate from properties in these "low-risk" zones, making a professional risk assessment essential regardless of your map color.

Does flood insurance cover mold damage after the water recedes?

Flood insurance typically covers mold remediation only if the mold is a direct result of the flooding and was unavoidable. If a homeowner fails to take reasonable steps to dry out the property once it's safe to enter, the insurance carrier may deny the mold portion of the claim. To protect your investment, you must begin professional water extraction and dehumidification immediately after the water recedes. This proactive mitigation is a strategic requirement for ensuring your claim remains valid under most policy terms.