How Much Homeowners Insurance Do I Need in Florida? (2026 Guide)

- siinsuranceflorida

- 4 days ago

- 12 min read

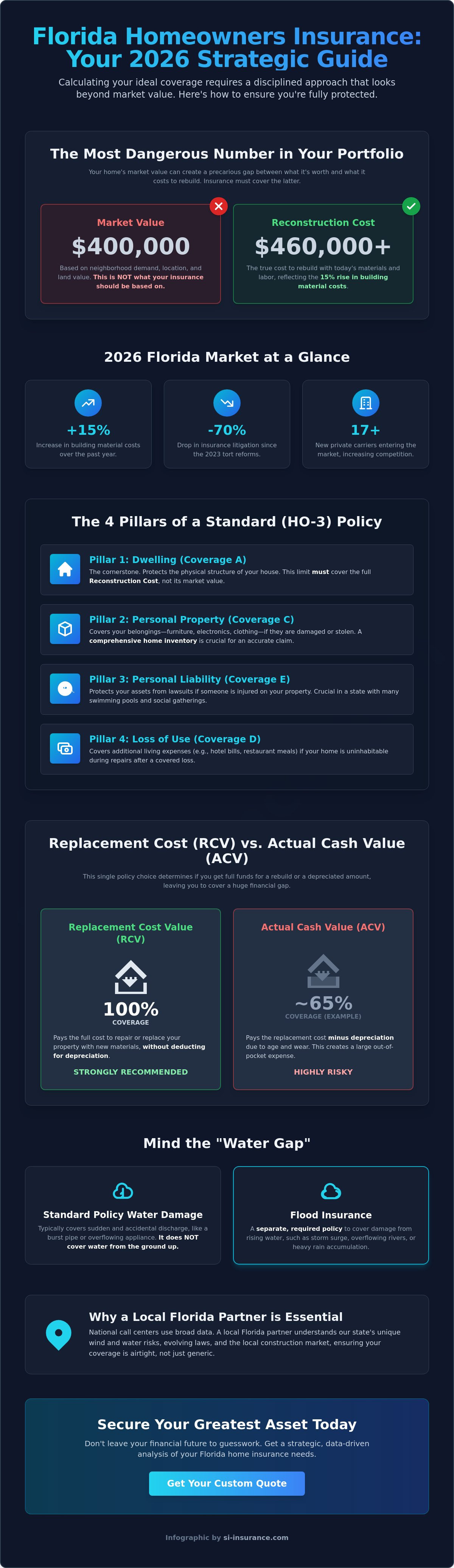

The $400,000 you paid for your home is likely the most dangerous number in your financial portfolio if you use it to determine your policy limits. While market values fluctuate based on neighborhood demand, the actual cost of building materials rose by 15% in the past year alone; this creates a precarious gap between what your home is worth and what it costs to rebuild. Determining how much homeowners insurance do I need in Florida requires a move away from retail guesswork toward a disciplined framework of strategic risk management.

You likely feel the weight of escalating premiums and the frustration of deciphering complex policy exclusions for wind or water. At SI Insurance, we understand that securing your greatest asset should offer absolute security rather than lingering doubt. This guide provides a comprehensive mathematical approach to calculating your ideal limits. We'll explore the impact of 2026 legislative shifts, such as HB 815, and analyze how to align your coverage with the current 8.8% rate adjustments at Citizens to ensure your long-term protection is both airtight and intellectually sound.

Key Takeaways

Learn how to calculate your dwelling coverage by prioritizing local square-foot reconstruction costs over market value to avoid underinsurance during inflationary cycles.

Understand the critical difference between Replacement Cost Value and Actual Cash Value to ensure your policy provides the full funds needed for a total rebuild without depreciation.

Discover a precise mathematical framework to determine exactly how much homeowners insurance do I need in Florida to protect your equity from the state's unique wind and water risks.

Gain clarity on the "Four Pillars" of a standard HO-3 policy and how to strategically align your liability and personal property limits with your specific risk profile.

Identify why a local Florida partner is essential for navigating evolving state laws and securing bespoke coverage that national call centers often overlook.

Table of Contents

Navigating the Florida Home Insurance Landscape in 2026

The Florida insurance market in 2026 presents a landscape where traditional wisdom often falls short. While most national carriers rely on broad actuarial data, the Sunshine State demands a more granular, strategic approach to risk. You might find yourself asking, "how much homeowners insurance do I need in Florida?" only to receive answers that don't account for the localized volatility of our coastal regions. To build a solid foundation, it helps to understand homeowners insurance basics, but your strategy must evolve beyond generalities to address the specific economic pressures of the Gulf and Atlantic coasts.

To help visualize these core concepts, this video breaks down the fundamental math of coverage limits:

The 2026 Market Context for Homeowners

Recent legislative reforms have begun to yield tangible results, providing a sense of stability for Florida entrepreneurs and families who've endured years of unpredictability. The Florida Office of Insurance Regulation (OIR) has taken a more proactive stance in 2026, ensuring that the 17 new private carriers entering the market maintain underwriting excellence while protecting policyholders from unjustified rate hikes. Following the 70% drop in insurance litigation since the 2023 tort reforms, bespoke risk transfer is now the standard for residents seeking to move away from high-cost state options. This shift allows for more sophisticated policy structures that prioritize long-term equity protection over short-term premium savings.

Market Value vs. Reconstruction Cost

One of the most common pitfalls in strategic risk management is the confusion between what a home would sell for and what it would cost to actually rebuild it. Your insurance carrier doesn't care about your school district or the desirability of your neighborhood; they focus exclusively on the physical structure. While your land value might appreciate, it's the 15% rise in building material costs over the past year that dictates your coverage needs. Replacement Cost is the expense to rebuild your home from scratch using current labor and material rates. By aligning your Dwelling (Coverage A) limits with 2026 reconstruction realities, you ensure that a total loss doesn't result in a financial deficit. At SI Insurance, we emphasize this distinction to prevent our clients from being blindsided by the gap between market demand and construction reality.

Evaluating Your Core Coverage Pillars: Dwelling, Property, and Liability

A standard HO-3 policy functions as a financial blueprint for your recovery after a catastrophic event. To truly answer the question, "how much homeowners insurance do I need in Florida," you must view your policy through the lens of four distinct pillars. Coverage A, or Dwelling coverage, serves as the cornerstone. It doesn't reflect what you could sell your house for on a Tuesday afternoon; it reflects the cold reality of construction invoices. You can use tools to calculate your ideal coverage limits, but these should always be adjusted for local Florida labor spikes. Coverage C covers your personal property, which we view as a non-negotiable strategic asset. Without a comprehensive digital inventory, you're essentially guessing at the value of your life's work during a high-stress claim period. Finally, Coverage E addresses personal liability. In a state with a high density of residential swimming pools and frequent social gatherings, this pillar protects your future earnings from litigation that could otherwise lead to insolvency.

The "Water Gap": Flood vs. Sewer Backup

There's a dangerous misconception that a standard homeowners policy handles all types of water intrusion. It doesn't. We emphasize the strategic necessity of separate flood insurance, especially since the 2026 flood disclosure laws now mandate transparency for all property transfers. Even if you reside in a "Zone X," the risk of surface water accumulation during a tropical depression is statistically significant. You should also evaluate whether your risk profile requires a bespoke water backup endorsement. This specific coverage handles internal failures, such as a burst pipe or a backed-up sewer line, which are frequently excluded from both standard home and flood policies. If you're looking for a more tailored approach to these gaps, the consultants at SI Insurance can help you audit your existing endorsements.

Additional Living Expenses (ALE) in a Post-Hurricane Scenario

When a major storm impacts the peninsula, the demand for skilled tradespeople creates a massive bottleneck. Estimating the duration of your reconstruction is vital. In the 2026 labor market, rebuilding a high-value home can easily take 18 to 24 months due to supply chain complexities and contractor availability. Your ALE limit shouldn't be a random flat dollar amount; it must be a strategic guardrail that maintains your current lifestyle while you're displaced. This coverage pays for hotel stays, rental properties, and even the increased cost of meals. If your policy only provides 12 months of ALE, you might find yourself paying out-of-pocket for a luxury rental while your home is still a shell of concrete and studs. We recommend limits that reflect at least two years of potential displacement to ensure your family's stability isn't compromised by the pace of the Florida construction industry.

The Replacement Cost vs. Actual Cash Value Debate

Choosing between valuation methods is arguably the most consequential decision in your risk management strategy. When you're determining how much homeowners insurance do I need in Florida, you'll encounter two primary options: Actual Cash Value (ACV) and Replacement Cost Value (RCV). ACV is defined as the cost to replace your property minus its accumulated depreciation. In our subtropical climate, where salt air and high humidity accelerate the physical decay of building materials, depreciation can strip away a significant portion of your claim's value. RCV allows for a "like-kind and quality" rebuild without out-of-pocket depreciation costs. This distinction is the bedrock of underwriting excellence, as it ensures your financial recovery isn't hampered by the age of your home's components.

The Insurance Information Institute provides detailed guidance on how much homeowners insurance you need to bridge this gap effectively. For a sophisticated homeowner, RCV is the only logical choice for maintaining the integrity of a high-value portfolio. It eliminates the "depreciation tax" that often surprises policyholders after a total loss. By opting for RCV, you're securing a guarantee that your lifestyle and assets will be restored to their original state, regardless of the years that have passed since your last renovation. At SI Insurance, we view RCV as a non-negotiable standard for clients who prioritize absolute security over the false economy of lower premiums.

The "Roof Replacement" Hurdle

Many Florida carriers are aggressively shifting toward ACV for roofs that exceed 10 or 15 years in age, particularly in Broward County. This transition creates a massive liability for homeowners in Sunrise or Pompano Beach who might find themselves responsible for 50% of a roof's cost after a hurricane. To mitigate this risk, Law and Ordinance coverage is a vital strategic alignment. This endorsement ensures that your policy accounts for 2026 building code upgrades, which often require more expensive materials and labor than what was standard when your home was originally constructed. Without this specific protection, you're essentially self-insuring the gap between old standards and modern safety requirements.

Bespoke Endorsements for High-Value Items

Standard personal property limits typically include sub-limits that fail to protect elite collections of jewelry, fine art, or high-end electronics. If you've invested in significant assets, jewelry insurance Florida offers the bespoke risk transfer necessary to protect these items at their full appraised value. Utilizing "Scheduled Personal Property" endorsements provides a strategic advantage by offering broader coverage than a standard policy, often including protection against mysterious disappearance or accidental damage. This white-glove approach to asset protection ensures that your most cherished belongings are managed with the same meticulous detail as your primary dwelling.

A 5-Step Guide to Calculating Your Ideal Coverage Limits

Calculating how much homeowners insurance do I need in Florida isn't a matter of intuition; it's a rigorous exercise in financial engineering. To ensure your greatest asset is strategically protected, you must move beyond the automated estimates provided by retail websites. We recommend a disciplined, five-step approach that prioritizes precision and long-term security. First, determine your local square-foot reconstruction cost based on 2026 Florida averages. Second, conduct a meticulous digital inventory of your high-value assets and strategic belongings. Third, evaluate your total net worth to set appropriate Liability (Coverage E) limits that protect your future earnings. Fourth, analyze your hurricane deductible against your current liquid savings to ensure a 2% or 5% deductible won't cause a cash flow crisis. Finally, consult with a sophisticated local advisor to finalize the strategic alignment of your policy with your specific risk profile.

Doing the Math: The Dwelling Formula

Your base dwelling limit is derived from a simple but vital equation: your home's total square footage multiplied by the current local construction rate. In 2026, we've observed that labor and material costs continue to fluctuate, making it necessary to add a strategic buffer of 10% to 20% above the initial estimate. This ensures that even if a widespread disaster causes a localized spike in building costs, your policy remains solvent. We strongly advocate for "Extended Replacement Cost" endorsements, which act as a vital safety net by providing additional coverage beyond your stated limit if rebuilding costs exceed expectations due to unforeseen market volatility. If you want to ensure your limits are truly airtight, you can schedule a strategic risk assessment with our team today.

Assessing Your Risk Exposure

Beyond the physical structure, you must account for "attractive nuisances" on your property, such as swimming pools or trampolines, which significantly elevate your liability risk. In Florida's litigious environment, a standard $300,000 liability limit is often insufficient for high-net-worth individuals. We recommend evaluating the need for personal umbrella insurance to provide an additional layer of bespoke risk transfer that sits above your primary policy. This is also an opportune time to consider Florida auto insurance bundling strategies. By aligning your home and auto policies, you can often secure higher underlying liability limits and more favorable premium structures, ensuring your entire portfolio is managed with underwriting excellence. This holistic view prevents the fragmented coverage gaps that often plague off-the-shelf insurance products.

Strategic Risk Management: Why a Local Florida Partner Matters

Relying on a national call center for Florida property protection often leads to fragmented coverage that fails during a crisis. These organizations typically utilize broad, automated models that lack the geographic precision necessary for our unique environment. When you're assessing how much homeowners insurance do I need in Florida, you're not just looking for a number on a page; you're seeking a sophisticated risk mitigation strategy. SI Insurance acts as a strategic guardian for your investment, providing a white-glove approach that national platforms simply cannot replicate. We don't just sell policies. We engineer bespoke risk transfer solutions that offer absolute security and intellectual confidence.

The SI Insurance Advantage in Broward County

Our commitment to the Sunrise and Pompano Beach communities is built on years of managing the state's complex regulatory shifts. In 2026, the Florida market has seen 17 new private carriers enter the space, each with different underwriting criteria and risk appetites. Our independent status is a significant advantage for our clients. It allows us to shop for strategic alignment across a diverse range of carriers, ensuring that your policy is tailored to your specific property rather than being a generic, one-size-fits-all product. A meticulous policy review with a local expert can uncover hidden gaps in your ordinance and law coverage or your hurricane deductibles that a distant representative might overlook.

Closing the Protection Gap

The protection gap is a silent threat to your net worth. As we've analyzed, the 15% rise in construction costs over the last year means that a policy written even eighteen months ago might now be dangerously obsolete. Precise limits prevent the financial ruin that follows an underinsured total loss. We recommend an annual strategic review to account for any home improvements or shifts in the local labor market. This ensures your coverage remains a live, responsive document rather than a static expense. When you finalize the math on how much homeowners insurance do I need in Florida, the execution of that plan is where the real value lies. You deserve the peace of mind that comes from knowing your greatest asset is shielded by rigorous analysis and foresight. Secure your strategic home insurance quote today and take the first step toward institutional-grade protection for your home.

Securing Your Legacy with Precision and Foresight

Rebuilding a home in our current economy requires more than just a standard policy; it requires a calculated understanding of 2026 building codes and construction labor realities. We've explored how the 15% surge in material costs has reshaped the answer to how much homeowners insurance do I need in Florida, moving the needle far beyond simple market valuations. By prioritizing replacement cost value and closing the "water gap" with specific endorsements, you're not just buying a product. You're engineering a safety net that respects the true worth of your lifestyle.

Since our founding in 2022, SI Insurance has operated as an independent agency dedicated to the nuances of South Florida risk mitigation. We specialize in bespoke solutions for high-value assets that national call centers often overlook. Don't leave your financial stability to an automated algorithm. Instead, Request a Strategic Home Insurance Review from SI Insurance to ensure your policy reflects the sophisticated protection you deserve. It's time to move forward with the absolute security that only meticulous planning can provide.

Frequently Asked Questions

Is homeowners insurance mandatory in the state of Florida?

While Florida law does not mandate homeowners insurance, mortgage lenders typically require it as a condition of the loan to protect their financial interest. If you own your home outright, you aren't legally forced to carry it, but skipping coverage leaves your equity exposed to the 15% increase in construction costs seen over the past year. Most residents view it as a strategic necessity rather than a legal obligation to avoid total loss.

How much liability insurance should I carry for a home with a pool?

We recommend a minimum of $500,000 in personal liability coverage, often supplemented by a $1 million umbrella policy for homes with "attractive nuisances" like pools. Standard $100,000 limits are insufficient in 2026's litigious environment. Strategic risk management involves layering coverage to protect your net worth from catastrophic legal judgments arising from accidental injuries or submersions on your property.

What is the difference between a hurricane deductible and a standard deductible?

A hurricane deductible is a separate, higher cost that applies specifically to windstorm damage from a named storm, whereas a standard deductible applies to other perils like fire or theft. Hurricane deductibles are typically calculated as a percentage, such as 2% or 5% of the home's total dwelling value. You must ensure your liquid savings can cover these thousands of dollars before your policy provides financial relief.

Does my Florida homeowners policy cover flood damage automatically?

No, standard homeowners policies in Florida exclude damage caused by rising surface water or storm surges. You must secure a separate flood insurance policy to address this specific risk, which is a critical step in answering how much homeowners insurance do I need in Florida. As of 2026, Citizens policyholders with over $400,000 in replacement cost are now legally required to carry flood coverage regardless of their zone.

What happens if my home is underinsured during a total loss?

You are responsible for paying the difference between the policy limit and the actual reconstruction cost, which can lead to significant financial strain. Many policies include a "coinsurance clause" that may penalize you if your coverage is less than 80% of the home's value. This highlights why strategic alignment with current building costs is the only way to ensure absolute security and a complete recovery after a disaster.

How do I know if I need "Law and Ordinance" coverage in Florida?

You need this coverage if your home was built more than 10 or 15 years ago, as building codes have evolved significantly since the 2023 legislative reforms. Law and Ordinance pays for the mandated upgrades required by local authorities during a rebuild. Without it, you must pay out of pocket for modern safety features like impact windows or reinforced roof-to-wall connections required by 2026 standards.

Can I change my coverage limits during hurricane season?

Yes, you can generally adjust your limits at any time, but carriers often implement a "binding moratorium" when a tropical storm is actively approaching the state. It is vital to perform your strategic review well before June 1st to avoid being locked into outdated limits. Waiting until a storm is in the Atlantic prevents you from achieving the underwriting excellence needed for true, bespoke protection.

How often should I update my home insurance limits in Florida?

We advise a comprehensive policy review at least once every 12 months or immediately following any major home renovation. Frequent updates are necessary because Florida's market stabilization and shifting labor costs can render your previous limits obsolete within a single year. This proactive approach is a hallmark of strategic risk management for high-value Florida properties and ensures your coverage stays accurate.

Comments