Understanding Your Florida Hurricane Deductible: A 2026 Strategic Guide for Homeowners

- siinsuranceflorida

- Mar 13

- 14 min read

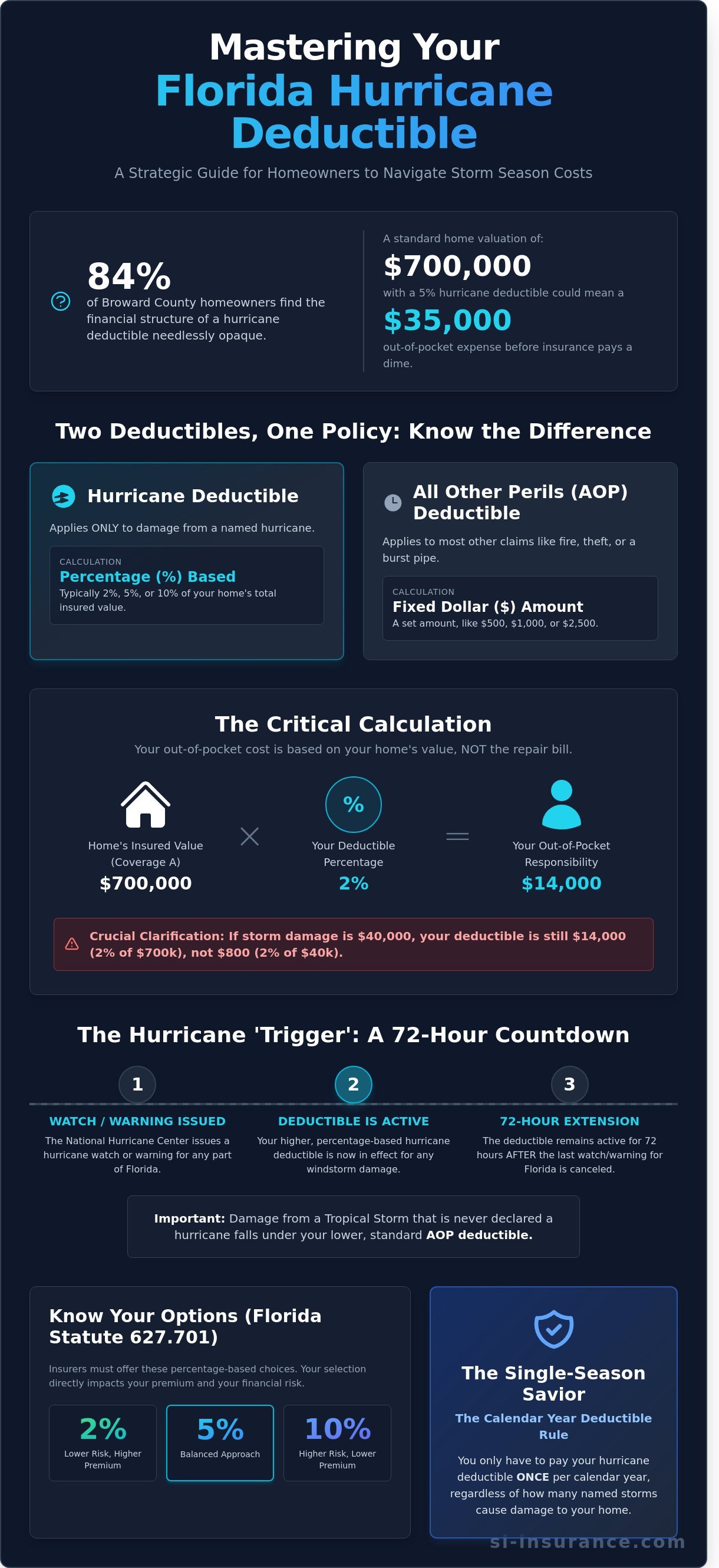

What if the 2% figure listed on your policy declarations page actually translates to a $14,000 out-of-pocket expense before your carrier contributes a single dollar toward storm recovery? At least 84% of homeowners in Broward County find the financial architecture of a florida hurricane deductible to be needlessly opaque. It’s natural to feel a sense of apprehension when you realize that a standard $700,000 home valuation could leave you responsible for the first $35,000 of damage during a catastrophic event. This strategic guide provides the professional clarity you need to master these complex risk management structures. You'll gain the intellectual confidence to select a deductible that aligns with your 2026 financial goals while ensuring your estate remains insulated from unexpected capital calls. We'll examine the specific math of percentage-based triggers, detail the 2023 legislative updates to the calendar year deductible rule, and clarify exactly when the 72 hour hurricane clock begins its countdown.

Key Takeaways

Learn the specific legal timeline known as the "72-hour rule" to understand exactly when your storm coverage begins and ends.

Gain clarity on how a florida hurricane deductible is calculated as a percentage of your home’s total insured value, helping you avoid unexpected out-of-pocket costs.

Evaluate the trade-offs between lower monthly premiums and higher upfront deductibles to create a strategic risk plan that protects your personal savings.

Identify why your specific location in Broward County-from Sunrise to Pompano Beach-dictates a unique approach to managing windstorm risks.

Discover how local, professional insight can help you secure a bespoke insurance solution designed specifically for the complexities of the South Florida climate.

Table of Contents What is a Florida Hurricane Deductible and Why Does it Exist? Calculating the Cost: The Math Behind the Percentage The Hurricane 'Trigger': When Does the Deductible Apply? Strategic Risk Management: Choosing the Right Deductible How Si Insurance Agency Secures Your Florida Home

What is a Florida Hurricane Deductible and Why Does it Exist?

A florida hurricane deductible represents a specific portion of an insurance claim that a homeowner must pay out of pocket before their insurance provider covers the remaining costs associated with windstorm damage. Unlike standard policies in other states, Florida requires this distinct financial layer to address the unique catastrophic risks inherent to our peninsula. To understand the mechanics of these policies, it helps to first define what a deductible is in a broader context. While a typical deductible is often a fixed dollar amount, the hurricane version is almost always calculated as a percentage of the home's total insured value, which can lead to significant financial implications during a disaster.

The necessity for this specialized deductible stems from Florida's volatile weather history. Following the destruction of Hurricane Andrew in 1992, which resulted in approximately $27.3 billion in insured losses, the private insurance market faced a near-total collapse. Carriers realized that a standard $500 or $1,000 deductible was insufficient to offset the billions of dollars in risk accumulated in high-density areas like Broward County. Consequently, the state introduced percentage-based deductibles to distribute the risk more equitably between the insurer and the policyholder. This structure ensures that insurance companies remain solvent even after a massive Category 4 or 5 event.

There's a critical distinction between your "All Other Perils" (AOP) deductible and the hurricane-specific one. Your AOP deductible applies to common claims like a kitchen fire, a burst pipe, or a theft. These are usually set at a manageable flat rate. In contrast, the hurricane deductible only activates when the National Hurricane Center declares a hurricane. Because this deductible is often 2%, 5%, or even 10% of your home's Coverage A limit, the difference in your out-of-pocket costs can be tens of thousands of dollars. Strategic risk management in 2026 requires homeowners to account for this gap well before a storm enters the Atlantic.

The Legal Framework: Florida Statute 627.701

Florida Statute 627.701 dictates the rules for how insurers must offer these deductibles. The law requires that insurance companies provide options for 2%, 5%, or 10% deductibles, and in some cases, a flat $500 option for lower-value properties. The Florida Office of Insurance Regulation (OIR) oversees these standards to prevent predatory pricing and ensure market stability. Your policy's declarations page must explicitly state the exact dollar amount of your percentage deductible. For example, if your home is insured for $600,000, a 2% deductible must be clearly listed as $12,000. This transparency is a legal safeguard for Broward County residents.

Hurricane vs. Tropical Storm: The Distinction

A common misconception is that any heavy wind triggers the higher deductible. This isn't the case. The florida hurricane deductible only applies from the moment the National Hurricane Center issues a hurricane watch or warning for any part of Florida. It remains in effect for 72 hours after the final warning is downgraded or canceled. If a tropical storm brings 65 mph winds but never reaches hurricane status, your lower AOP deductible applies instead. Si Insurance provides the elite expertise needed to interpret these technical triggers. Our team ensures that clients understand exactly when their financial exposure changes based on official meteorological declarations.

Calculating the Cost: The Math Behind the Percentage

Understanding the financial mechanics of a policy is the first step toward effective risk mitigation. Unlike a standard $500 or $1,000 theft or fire deductible, a florida hurricane deductible operates on a percentage basis. This distinction is vital for homeowners in Broward County because it shifts the calculation from a fixed cost to a variable exposure tied directly to the replacement value of the structure. It's not just a number on a page; it's a strategic calculation of your personal risk retention that requires careful foresight.

The most common misconception involves the base figure used for the calculation. Many policyholders mistakenly believe the percentage applies to the total damage sustained after a storm. This is incorrect. The deductible is calculated against the total insured value of the home, known as Coverage A in your policy documents. If a storm causes $40,000 in roof damage, your deductible isn't a percentage of that $40,000. Instead, it's a percentage of your home's total insured limit. To better understand the history and logic behind this system, the Insurance Information Institute provides a detailed look at Hurricane and windstorm deductibles across different coastal states.

Consider a 2,400 square foot residence in Pompano Beach with a Coverage A valuation of $500,000. Under a standard 2% deductible, the homeowner is responsible for the first $10,000 of repairs. If a Category 3 hurricane causes $15,000 in structural damage, the insurance carrier only issues a check for $5,000. This creates a significant out-of-pocket gap that requires immediate liquidity. You're essentially self-insuring the first $10,000 of every hurricane claim within a single calendar year, which can be a heavy burden if you haven't prepared your finances for the season.

Common Percentage Tiers in 2026

In the 2026 insurance market, three primary tiers dominate the landscape. The 2% tier remains the benchmark for most Broward residents, offering a balance between upfront risk and manageable annual costs. As property values in South Florida rose by an average of 7.4% annually through 2025, the florida hurricane deductible you select becomes a more significant factor in your total cost of ownership. Many carriers now suggest 5% or 10% options for high-value estates to keep premiums from escalating. For homes valued under $250,000, some specialty carriers still offer flat-rate deductibles of $500 or $1,000, though these are becoming increasingly rare as risk modeling becomes more granular and precise.

The Impact on Your Monthly Premium

There's an inverse relationship between your deductible and your annual premium. Opting for a 5% deductible instead of 2% can reduce your annual windstorm premium by as much as 18% to 24%, depending on the age of the roof and the presence of impact-resistant windows. This is a strategic financial trade-off. A homeowner might save $1,650 a year in premiums by accepting an additional $15,000 in potential risk. The break-even point in this scenario occurs at approximately 9 years. We recommend establishing a dedicated hurricane fund in a liquid account to bridge this gap. This ensures your bespoke risk transfer strategy remains sound even when the unexpected occurs. Setting aside these premium savings can eventually cover the cost of the deductible itself.

2% Deductible: Best for those who prefer lower out-of-pocket costs after a storm.

5% Deductible: Ideal for homeowners with high liquidity who want to lower annual carry costs.

10% Deductible: Often reserved for high-net-worth individuals managing large-scale property portfolios with higher risk tolerance.

The Hurricane 'Trigger': When Does the Deductible Apply?

Florida law dictates exactly when a standard windstorm claim transforms into a high-stakes hurricane claim. It's a binary switch, not a sliding scale. This activation isn't based on local wind speeds in Sunrise or the severity of rain in Fort Lauderdale. Instead, the trigger is tied directly to the National Hurricane Center (NHC). The moment this body issues a hurricane watch or warning for any part of the state, the florida hurricane deductible becomes the active financial threshold for your policy. This applies even if the storm makes landfall 400 miles away in the Panhandle. If the NHC's declaration is active anywhere in Florida, your risk transfer strategy shifts immediately. SI Insurance maintains constant communication with underwriting partners during these windows to ensure our clients understand their exposure in real-time.

The Clock: Start and End Times

The temporal boundaries of a hurricane event are rigid and leave no room for interpretation. The clock starts when the NHC issues the first watch or warning for any portion of the state. It doesn't stop when the clouds clear over Broward County. By statute, the window remains open for exactly 72 hours after the final hurricane watch or warning is downgraded or lifted for any part of Florida. If a weakened oak tree crashes into your roof 75 hours after that last warning, your insurer will likely apply your All Other Perils (AOP) deductible. This distinction is critical for your financial planning. An AOP deductible is often a fixed amount like $1,000 or $2,500. In contrast, a 2% hurricane deductible on a $750,000 home requires you to cover the first $15,000 of repairs. We help you track these 72-hour windows to ensure your claims are categorized accurately.

The 'Calendar Year' Rule: A Critical Protection

Florida's legislative reforms provide a vital safeguard for homeowners known as the calendar year deductible. You're only responsible for paying your full florida hurricane deductible once between January 1 and December 31. If a second storm strikes Broward County in the same season, your liability is significantly limited. You must document every cent spent on the first event to benefit from this. According to the official Florida hurricane deductible guide, if you didn't fully meet the deductible during the first storm, the remaining balance applies to the next one. After that balance is satisfied, the deductible for any subsequent hurricane claims in that same year drops to the much lower AOP amount.

SI Insurance advises clients to maintain a meticulous digital archive of all repair invoices and material receipts. Even if your first claim doesn't exceed your deductible, those costs act as a credit against future storms in 2026. This strategic approach ensures that multiple landfalls don't result in repetitive, catastrophic out-of-pocket losses. Our team provides the underwriting excellence needed to navigate these aggregate totals. We act as your strategic guardian, ensuring that your insurer recognizes every dollar you've already contributed toward your annual limit. This level of foresight is what separates a standard policy from a bespoke risk management solution.

Watch/Warning Issued: The high deductible is triggered statewide.

72-Hour Post-Storm: The window where the hurricane deductible applies ends.

AOP Transition: Claims outside the 72-hour window revert to standard deductible rates.

Aggregate Tracking: Once the annual hurricane deductible is met, subsequent storms use the AOP rate.

Strategic Risk Management: Choosing the Right Deductible

Selecting your florida hurricane deductible is a high-stakes decision that requires a meticulous balance between immediate cash flow and long-term risk exposure. SI Insurance approaches this choice as a core component of your broader financial architecture. We don't view insurance as a static expense; we treat it as a dynamic tool for wealth preservation. For a Broward County property valued at $1.2 million, the difference between a 2% and a 5% deductible represents a $36,000 swing in potential liability. This isn't a sum to be managed lightly. Our role is to ensure that your deductible choice aligns with your overall fiscal health and risk tolerance.

Evaluating Your Financial Resilience

If a major storm makes landfall in 2026, can your household comfortably absorb a $20,000 or $30,000 assessment without liquidating long-term investments? Choosing a higher deductible often yields a premium reduction of approximately $450 to $800 annually. However, if that modest saving forces you into a $10,000 increase in personal risk, the mathematical logic often fails. We analyze your emergency reserves to ensure your policy remains a safety net, not a source of financial strain. High-value properties in neighborhoods like Rio Vista or Weston require bespoke risk transfer strategies that align with your specific liquidity profile. It's about protecting your lifestyle, not just your roof.

Lender Requirements and Compliance

Your mortgage agreement is often the primary constraint on your deductible flexibility. Approximately 85% of institutional lenders, including national banks like Bank of America and Wells Fargo, prohibit hurricane deductibles that exceed 5% of the total dwelling coverage. This limit exists to protect the bank's collateral. If you attempt to increase your deductible to 10% to lower costs, you risk falling out of compliance with your escrow requirements. SI Insurance acts as an intermediary, coordinating directly with your lender's compliance department to verify that your florida hurricane deductible meets every contractual obligation while still optimizing your premium. We prevent the administrative friction that often accompanies policy changes.

The geographical nuances within Broward County also dictate strategy. A homeowner in Pompano Beach, situated within two miles of the Atlantic coastline, faces a higher probability of wind-driven structural damage than a resident in Sunrise. Those closer to the coast often benefit from lower deductibles because the statistical probability of a claim is higher. Conversely, inland residents might find that the premium savings of a higher deductible outweigh the lower risk of catastrophic structural loss. SI Insurance provides the analytical precision needed to move through these variables with absolute confidence. We act as your strategic guardian, ensuring that your coverage is as sophisticated as the assets it protects.

Strategic risk management also involves maintaining your property's value, a core focus for real estate and property management experts. For homeowners looking for comprehensive asset protection beyond insurance, firms like Morgan Property Solutions Inc. provide valuable real estate services throughout central Florida.

to calibrate your deductible for the 2026 hurricane season.

How Si Insurance Agency Secures Your Florida Home

Securing a high-value property in Broward County requires a level of precision that automated digital algorithms simply cannot replicate. At Si Insurance Agency, we treat risk management as a specialized discipline rather than a commodity transaction. Our commitment to providing bespoke risk transfer solutions means we evaluate every variable of your profile to ensure your assets are insulated against the unpredictable nature of the Atlantic season. We recognize that the florida hurricane deductible often represents the most significant out-of-pocket exposure for homeowners; therefore, we work to align that figure with your specific cash flow requirements and risk tolerance.

Our process relies on underwriting excellence to identify the most competitive rates across a network of over 25 specialized carriers. We don't just provide a quote. Instead, we provide a technical analysis of how different policy structures will perform during a catastrophic event. In 2025, property valuations in South Florida rose by an average of 8.4 percent, making it vital to adjust your coverage limits before the 2026 cycle begins. By leveraging our deep relationships with top-tier insurers, we find the exact point where premium costs and deductible risks meet your long-term financial goals. This methodical approach ensures that your protection is engineered for performance, not just compliance.

Our Local Expertise in Sunrise and Pompano Beach

Living and working in Broward County gives us a distinct advantage. We understand the specific wind-load requirements and flood elevations in areas like Sunrise and Pompano Beach. This isn't just about data points; it's about knowing how a storm surge affects one neighborhood differently than the next. You can explore the history of our firm and our dedication to the community on our Sobre Nosotros page. When a storm hits, you won't be dealing with a call center in another time zone. You'll have a local advocate who understands the local landscape and the urgency of your recovery.

Next Steps for Your 2026 Hurricane Preparedness

The window for meaningful policy adjustment closes quickly as we approach the June 1st start of the hurricane season. We invite you to schedule a strategic alignment meeting to review your current policy limits and ensure your florida hurricane deductible is structured correctly for the year ahead. True preparedness also means having a plan for your physical belongings; if your home requires significant repairs, you may need to move items into a secure facility. For help with these logistics, you can visit All American Moving And Storage. Waiting until a tropical depression is formed is often too late to secure the best terms. Our team is ready to conduct a comprehensive audit of your current coverage to identify any gaps that could lead to financial leakage during a claim. Contact Si Insurance Agency for a professional quote today and experience the difference that elite, white-glove service makes for your peace of mind.

Strategic protection is the result of rigorous analysis and local insight. By choosing a partner that prioritizes intellectual confidence and stability, you ensure that your home remains a secure sanctuary regardless of the weather. We look forward to acting as your strategic guardian for the 2026 season and beyond. Our goal is to provide the clarity you need to make informed decisions about your most valuable assets.

Securing Your Financial Resilience for the 2026 Storm Season

Navigating the nuances of your florida hurricane deductible requires more than just a cursory glance at policy documents; it demands a calculated approach to risk mitigation. You've seen how these deductibles, which often range from 2% to 10% of your total insured value, function differently than standard perils. The specific trigger for these costs remains tied to National Weather Service declarations, making precise timing a critical factor in your financial planning. Since our firm’s inception in 2022, Si Insurance Agency has maintained deep local roots in Broward County to help homeowners decode complex Florida insurance statutes. We don't just offer off-the-shelf policies. We focus on strategic alignment and bespoke risk transfer to protect your most significant assets. Choosing a deductible is a high-stakes decision that impacts your liquidity during a recovery. Our team provides the intellectual confidence you need to manage these variables through rigorous analysis and underwriting excellence. You're not just buying insurance; you're partnering with a strategic guardian for your estate. Schedule a strategic risk assessment with Si Insurance Agency to refine your coverage today. Your peace of mind is our primary objective as we prepare for the years ahead.

Frequently Asked Questions

Is a hurricane deductible different from a windstorm deductible?

Yes, these two deductibles serve distinct roles in your risk mitigation strategy. A hurricane deductible only triggers when the National Hurricane Center declares a named storm, while a windstorm deductible applies to other events like tornadoes or summer gales. Florida Statute 627.701 governs these specific applications. You'll often find that windstorm deductibles are set as flat dollar amounts, whereas hurricane costs are tied to your total dwelling coverage.

Can I change my hurricane deductible in the middle of hurricane season?

You typically can't adjust your deductible once a storm is active or after a moratorium is issued. Most carriers in Broward County restrict policy changes once the National Weather Service issues a tropical watch or warning for any part of Florida. To ensure your strategic alignment is secure, you should finalize all deductible adjustments by May 15. This allows your underwriting to be fully processed before the June 1 start date.

What happens if two hurricanes hit Florida in the same year?

Florida law utilizes a calendar-year deductible that applies to all named storms during a single season. Once you've paid the full amount for the first event, your florida hurricane deductible for any subsequent storms in that same year effectively drops to zero. If the first storm doesn't meet the full deductible, the remaining balance carries over to the next hurricane. This aggregate approach provides a layer of financial stability for homeowners facing multiple threats.

How do I know if my deductible is a flat rate or a percentage?

You can identify your specific deductible type by reviewing the Declarations Page of your insurance policy. Most Florida residential policies utilize percentages such as 2%, 5%, or 10% of your total Coverage A dwelling limit. If your home is insured for $500,000, a 2% deductible means your out-of-pocket responsibility is $10,000. Some high-value bespoke policies offer flat rates, but these are less common in the current 2026 market environment.

Does my hurricane deductible apply to flood damage?

No, your hurricane deductible never covers damage caused by rising water or storm surges. Flood insurance is a separate risk transfer mechanism that requires its own policy and a distinct deductible. Standard homeowners policies specifically exclude flood losses. You must maintain a National Flood Insurance Program policy or a private alternative to protect your assets from the water damage that often accompanies tropical systems.

What is the most common hurricane deductible chosen in Broward County?

The 2% florida hurricane deductible remains the standard choice for approximately 68% of homeowners in the Broward County area. While opting for a 5% or 10% deductible can reduce your annual premium, it significantly increases your financial exposure during a loss. For a property valued at the local 2025 average of $450,000, a 2% deductible requires a $9,000 liquidity reserve. This balance represents a calculated approach to managing immediate costs versus long-term risk.

Are there any Florida programs to help with high deductibles?

The My Safe Florida Home program is the primary state initiative designed to assist homeowners with property hardening. In 2024, the Florida Legislature allocated $200 million to fund this program, providing grants for wind-resistant roof and window upgrades. While these funds don't pay your deductible directly, the resulting improvements trigger mandatory premium credits. These savings help you manage the higher costs of maintaining a more protective, low-percentage deductible.

Comments