Do I Need Flood Insurance in Pompano Beach? A Strategic Assessment for 2026

- siinsuranceflorida

- 2 minutes ago

- 12 min read

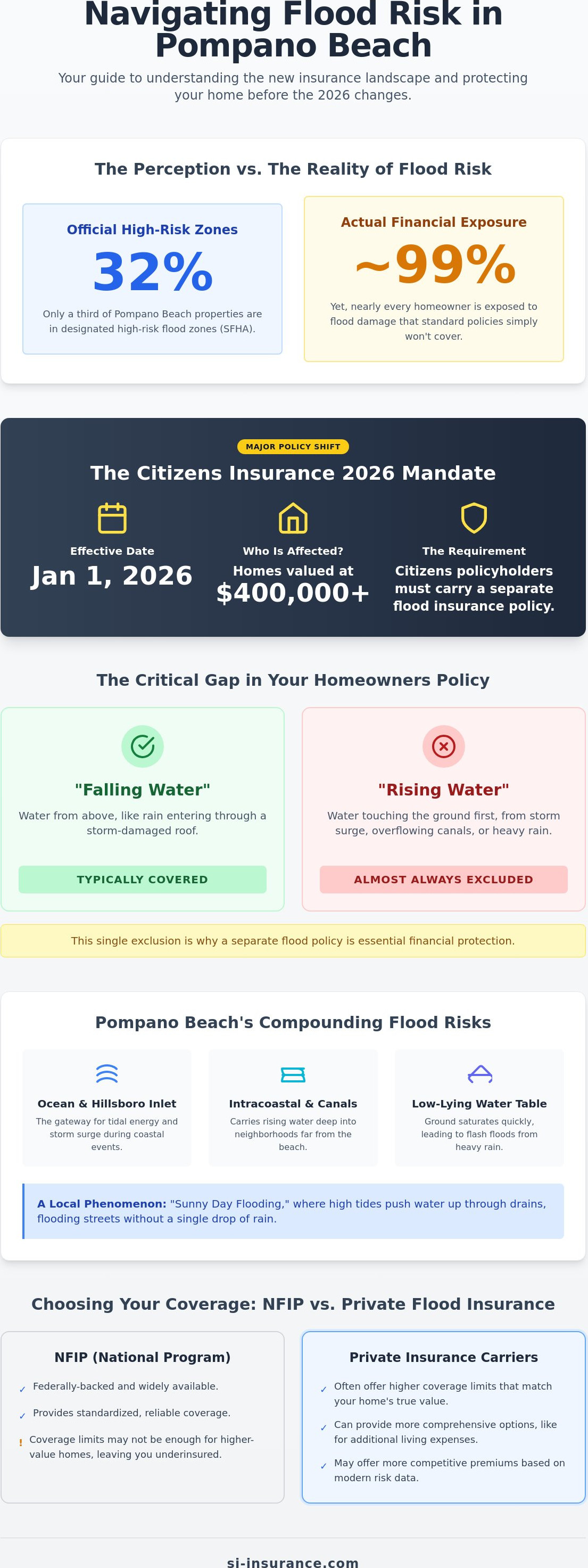

While only 32 percent of Pompano Beach buildings sit in a designated high-risk flood zone, nearly every property owner faces a significant financial exposure that standard homeowners policies simply ignore. If you are asking yourself, "do I need flood insurance in Pompano Beach," the answer is no longer just about meeting a lender's requirement; it's about closing a dangerous gap in your asset protection strategy. As of January 1, 2026, Citizens Property Insurance now requires flood coverage for all homes valued at $400,000 or more, signaling a major shift in how risk is managed across the South Florida coastline.

You likely feel the mounting pressure of rising premiums and the confusion of deciphering complex FEMA maps that seem to change every few years. It's exhausting to manage these shifting regulations while trying to keep your home and family secure. This guide will provide you with a clear roadmap to navigate the 2026 insurance landscape, ensuring you don't leave your greatest investment vulnerable to rising tides. We'll break down the differences between mandatory and recommended coverage, identify the hidden gaps in your current policy, and outline a strategic approach to secure the most competitive rates available in today's market.

Table of Contents

Assessing Your Geographic Risk in Pompano Beach

Understanding your property's vulnerability requires looking beyond the lines on a static map. In Pompano Beach, risk is defined by a complex interaction between the Atlantic Ocean, the Intracoastal Waterway, and a low-lying water table. Many residents mistakenly believe that being outside a high-risk zone equates to being safe. However, flood zones represent a statistical probability of inundation over a century, not a boundary that water refuses to cross. When you ask, "do I need flood insurance in Pompano Beach," you're really asking if you can afford to self-insure against a catastrophic event that doesn't care about your zone's letter grade.

The distinction between falling water and rising water is the most critical concept for Florida property owners. Standard homeowners insurance typically addresses "falling water," such as rain entering through a hole in the roof created by a fallen branch. Conversely, "rising water" describes water that touches the ground before entering your home. This type of damage is almost universally excluded from standard policies. Even during a tropical depression that doesn't reach hurricane strength, the sheer volume of precipitation can overwhelm the ground's ability to absorb moisture, leading to flash flooding that has nothing to do with storm surge or coastal proximity.

Pompano Beach's Coastal Geography

The Hillsboro Inlet acts as a primary gateway for tidal energy, influencing the water levels of the Intracoastal Waterway and its connected canal systems. Neighborhoods like Harbor Village and Garden Isles are particularly susceptible to "sunny day flooding," where high tides push water up through drainage pipes and over seawalls even without a cloud in the sky. While the city maintains an extensive network of pumps and drains, these systems are designed for historical norms, not the extreme rain events that have become more frequent in Broward County. Living near the coast means your risk isn't just about the ocean; it's about the water that surrounds you on three sides through the intricate canal network.

Defining 'Flood' for Insurance Purposes

For insurance purposes, a flood is an inundation of two or more acres or properties. This specific definition is used by the National Flood Insurance Program (NFIP) to determine when a claim is valid. It's vital to distinguish between hurricane wind damage and storm surge, as they are covered under entirely different policy structures. If a storm surge pushes three feet of water into your living room, your homeowners policy won't provide a cent of relief unless you have a separate flood policy in place. At SI Insurance, we often see the heartbreak that occurs when a family realizes their "comprehensive" coverage has a massive hole where flood protection should be. Understanding this gap is the first step in determining if you truly need flood insurance in Pompano Beach to protect your long-term financial stability.

Mandatory vs. Recommended Coverage: Navigating FEMA Maps

Determining your legal obligation starts with a look at your mortgage documents and the current federal map. If your home is situated in a Special Flood Hazard Area (SFHA) and you hold a mortgage backed by a federal entity, the government mandates coverage. When homeowners ask, "do I need flood insurance in Pompano Beach," the initial assessment often centers on Zone AE or Zone AH. These designations indicate a higher probability of inundation, and lenders for FHA, VA, or conventional loans won't close on a property without a policy in place. In Pompano Beach, Zone AE typically indicates areas where base flood elevations have been determined, while Zone AH covers areas where shallow ponding is expected during heavy rain events.

The landscape of pricing has evolved significantly with the implementation of Risk Rating 2.0. This methodology has transitioned the industry from a broad, zone-based approach to a highly individualized risk profile. FEMA now considers the specific distance to water sources and the unique structural integrity of your home to determine premiums. Official guidance on these transitions is available through FloodSmart.gov, which provides a baseline for understanding federal insurance structures. This shift means that two houses in the same zone might have different premiums based on their individual elevation and construction characteristics.

The Lender Requirement Framework

Mortgage providers act as the primary enforcers of flood insurance regulations to protect their underlying assets. If a property is remapped into a higher-risk zone, the lender is legally required to ensure a policy is active. If you ignore these notifications, you may fall into the "forced-place" insurance trap. In this scenario, the lender purchases a policy for you that is frequently more expensive and offers fewer protections than a private or NFIP policy you would choose yourself. It's a reactive situation that rarely benefits the homeowner and can significantly increase your monthly escrow payments.

The Zone X Misconception

The label of "Zone X" often creates a false sense of security for residents. While these areas are technically considered moderate-to-low risk, they aren't "no-risk" zones. Historically, more than 20 percent of all flood claims involve properties located outside of high-risk areas. In our coastal environment, a single afternoon of intense tropical rainfall can easily result in ground-water intrusion that overwhelms local drainage. For residents in these areas, the strategic choice is to secure a Preferred Risk Policy while rates are favorable. If you're questioning "do I need flood insurance in Pompano Beach" while living in Zone X, consider that the cost of a policy is a fraction of the expense required to remediate a flooded home. Speaking with an advisor can help you compare these costs against your actual risk profile.

The Critical Gap: Why Homeowners Insurance Isn't Enough

A common misconception among Pompano Beach residents is that a "comprehensive" homeowners policy serves as an all-encompassing shield against the elements. In reality, the legal architecture of a standard Florida homeowners contract contains a significant void known as the Water Exclusion Clause. This provision explicitly removes any obligation for the insurer to pay for damages resulting from surface water, tidal surges, or the overflow of bodies of water. If you're questioning, "do I need flood insurance in Pompano Beach," you've got to recognize that without it, you're essentially self-insuring against the most common natural disaster in the state.

The financial danger becomes most apparent during a major weather event where wind and water collide. Imagine a scenario where a tropical storm damages your roof, allowing rain to pour in, while simultaneously a storm surge pushes water through your front door. Without a dedicated flood policy, you face a complex burden of proof. You and your adjusters must meticulously determine which specific damage was caused by "falling water" (covered by your home policy) and which resulted from "rising water" (excluded). This creates a friction-filled recovery process that can leave significant portions of your repair costs unpaid.

The Anatomy of a Claim

Professional adjusters use forensic methods to differentiate between wind-driven rain and ground-water intrusion. They look for water lines on drywall and debris patterns to categorize the source of the loss. Hurricane deductibles apply only to wind-related damage, meaning a separate flood deductible must be met before those specific water-related losses are reimbursed. If you don't have that secondary policy, the "storm surge" portion of your loss remains your personal financial responsibility, regardless of how high your homeowners coverage limits are.

Strategic Asset Protection

True security requires a layered approach that accounts for both the structure of your home and the valuable assets within it. While your primary policy focuses on wind and fire, it often leaves personal property vulnerable to water damage in lower levels of the home. Standard federal flood policies don't typically include "loss of use" coverage, which pays for your temporary housing while your home is being remediated. To truly protect your lifestyle, you need a plan that integrates your Home Insurance in Florida with specialized flood protection. This ensures that whether the damage comes from the sky or the sea, your recovery is fully funded. At SI Insurance, we view this as a fundamental component of high-level risk management. It's not just about having a policy; it's about ensuring there are no gaps when you need support the most.

NFIP vs. Private Flood Insurance: Choosing the Right Strategy

Selecting between the National Flood Insurance Program (NFIP) and the rapidly expanding private market is a decision that requires a meticulous analysis of your property's replacement cost and your specific risk tolerance. If you're currently evaluating whether you do I need flood insurance in Pompano Beach, you're likely realizing that a one-size-fits-all solution rarely suffices for South Florida's complex real estate market. The federal government provides a reliable baseline, yet its rigid structure often creates secondary gaps for high-value coastal assets. Navigating these two paths requires an understanding of how each mechanism handles the unique geographical challenges of Broward County.

Federal Program Limitations

The NFIP is a foundational pillar of flood protection, but it operates under strict statutory caps that have not kept pace with Pompano Beach property values. For a residential structure, the maximum building coverage is $250,000, with personal property limited to $100,000. If your home’s reconstruction costs exceed this amount, you are essentially underinsured from day one. Another critical factor is the mandatory 30-day waiting period. You cannot wait for a tropical depression to form in the Atlantic to secure a policy; the federal program is designed for long-term planning, not reactive crisis management. Standard NFIP policies also frequently exclude or severely limit coverage for detached structures, such as guest houses or sophisticated outdoor kitchens, which are common in our local neighborhoods.

The Private Market Advantage

The emergence of the private flood market in 2026 has provided Pompano Beach homeowners with much-needed flexibility and higher indemnity limits. Private carriers often offer "excess" flood insurance, allowing you to protect the full value of a luxury coastal home far beyond the federal $250,000 ceiling. These policies can also be tailored to include specialized equipment that the NFIP typically ignores, such as expensive pool pumps and seawall components. Many private insurers have reduced waiting periods to as little as ten to fifteen days, providing a more agile response to the shifting weather patterns of the hurricane season.

When evaluating private carriers, we prioritize financial stability and claims-paying ability. It's essential to verify that a private insurer is backed by a strong AM Best rating to ensure they can meet their obligations after a widespread regional event. Interestingly, some property owners find that coordinating their flood strategy with other lines, such as their auto insurance in Florida, allows for a more cohesive view of their total household risk. To determine which path offers the best protection for your specific parcel, request a strategic risk assessment from our specialized team today. This comparison is the only way to ensure your coverage is as sophisticated as the investment it protects.

Securing Your Pompano Beach Property with SI Insurance

Protecting a high-value property in Broward County requires more than a standard policy; it demands a partnership with a firm that understands the intricate nuances of our coastal environment. At SI Insurance, we function as a protective guardian for your assets, utilizing a rigorous methodology to evaluate risk at the individual parcel level. While broad FEMA maps provide a starting point, they don't always capture the specific elevation nuances of your lot or the structural integrity of your home's foundation. When you ask, "do I need flood insurance in Pompano Beach," our team provides the analytical clarity needed to make an informed, data-driven decision based on your specific geographical coordinates.

As an independent agency founded in 2022, we aren't tethered to a single carrier's specific appetite for risk. Instead, we have the professional autonomy to scan a broad network of both NFIP and private insurers to find the specific financial structure that aligns with your long-term goals. This flexibility is vital in a market where regulations and pricing models are in a constant state of flux. We believe that true security comes from intellectual confidence, knowing that your coverage has been engineered to withstand the unique pressures of the South Florida climate. Our expertise in the Pompano Beach and Sunrise markets allows us to anticipate local shifts before they impact your bottom line.

The SI Insurance Difference

Our approach is rooted in delivering absolute security through airtight logic and localized expertise. We don't just facilitate transactions; we design comprehensive risk management strategies for high-level decision-makers who view their home as a significant investment. This means looking beyond the premiums to ensure the underlying terms and conditions are robust enough to handle a catastrophic event. We treat every client with a level of personalized service that mirrors the exclusivity of the properties we protect. Our commitment is to provide a composed and reassuring experience, ensuring your financial landscape remains stable regardless of the weather.

Your Path to Absolute Security

The first step in fortifying your position is a thorough review of your existing documentation, including your elevation certificate and current homeowners policy. This data allows us to identify any latent vulnerabilities or coverage gaps before the next storm cycle begins. Given the rapid pace of environmental and regulatory changes in Florida, an annual insurance check-up is no longer optional; it's a fundamental requirement for maintaining your financial health. It's time to move beyond the question of "do I need flood insurance in Pompano Beach" and start building a resilient defense for your estate. Contact us today for a comprehensive Pompano Beach insurance quote and begin the process of securing your legacy with a team that values precision and foresight.

Strategic Resilience for Your Pompano Beach Estate

The evolving regulatory climate of 2026 has transformed flood protection from a discretionary choice into a fundamental requirement for high-value properties. By now, it's clear that relying on standard homeowners policies alone leaves a significant portion of your asset vulnerable to the unique hydrological pressures of our coastline. Whether you're navigating the new Citizens mandates or assessing the specialized benefits of the private market, the decision of do I need flood insurance in Pompano Beach rests on a precise understanding of your home's specific elevation and risk profile.

At Si Insurance Agency, we combine deep local knowledge of Broward County maps with a sophisticated risk management approach to ensure your coverage is airtight. We provide access to both the NFIP and elite private carriers, allowing us to engineer a strategy that matches the stature of your investment. Don't leave your recovery to chance when you can secure it through meticulous planning and expert foresight. Our team is ready to act as your protective guardian in this complex landscape.

Secure your Pompano Beach investment with a tailored flood insurance quote from Si Insurance Agency.

Frequently Asked Questions

Is flood insurance required by law in Pompano Beach?

Flood insurance is not mandated by Florida state law for all residents, but it is required by federal law if you have a federally backed mortgage on a property in a Special Flood Hazard Area (SFHA). Additionally, as of January 1, 2026, Citizens Property Insurance requires all policyholders with homes valued at $400,000 or more to maintain separate flood coverage. This requirement will expand to all Citizens policyholders by 2027, regardless of their specific flood zone.

How much does flood insurance typically cost in Pompano Beach?

While premiums vary based on individual property characteristics under Risk Rating 2.0, the average Florida homeowner pays between $700 and $900 annually for an NFIP policy. Properties in high-risk zones like AE or VE may see rates ranging from $2,000 to over $15,000, while moderate-risk areas typically fall between $400 and $1,200. These figures represent industry averages and do not constitute specific quotes from our agency.

Does my Pompano Beach condo association cover my flood risk?

Your condo association’s master policy generally only protects the building's exterior and common elements, leaving your personal belongings and interior improvements vulnerable. To fully protect your investment, you must secure an individual flood policy that covers your unit's contents and any "walls-in" upgrades. This is a critical consideration when deciding do I need flood insurance in Pompano Beach as a condo owner.

Can I buy flood insurance if a hurricane is already approaching Florida?

You cannot effectively secure coverage once a storm is imminent because carriers typically stop binding new policies when a hurricane enters a specific geographic "box" near Florida. The NFIP also enforces a standard 30-day waiting period before a policy becomes active. While some private insurers offer shorter windows of 10 to 15 days, proactive planning is the only way to ensure your property is protected before a threat develops.

What is an Elevation Certificate and do I need one for a quote?

An Elevation Certificate is a document that records your building's height relative to the estimated flood level, and it remains a vital tool for securing the most accurate insurance rates. While FEMA's Risk Rating 2.0 has reduced the absolute necessity of this certificate for some federal quotes, it is often required by private carriers. Having one on file can sometimes demonstrate that your actual risk is lower than what the general maps suggest.

What is the difference between a flood zone and an evacuation zone in Broward County?

A flood zone is a geographic area defined by FEMA to determine the statistical probability of water inundation for insurance purposes, whereas an evacuation zone is a life-safety designation managed by Broward County. You might live in a low-risk flood zone but still be in a high-priority evacuation zone due to the threat of storm surge during a hurricane. Knowing both designations is essential for comprehensive disaster planning and risk management.

Does flood insurance cover mold damage after a storm?

Flood insurance will cover mold remediation only if the mold is a direct result of a covered flood event and you took reasonable steps to dry the property. If the mold develops due to a lack of maintenance or failure to clear water after the flood recedes, the claim is typically denied. This underscores why homeowners often ask do I need flood insurance in Pompano Beach to handle the secondary damage that follows a storm.

Comments