Flood Insurance Cost in Broward County: A Strategic 2026 Price & Coverage Guide

- siinsuranceflorida

- 1 day ago

- 12 min read

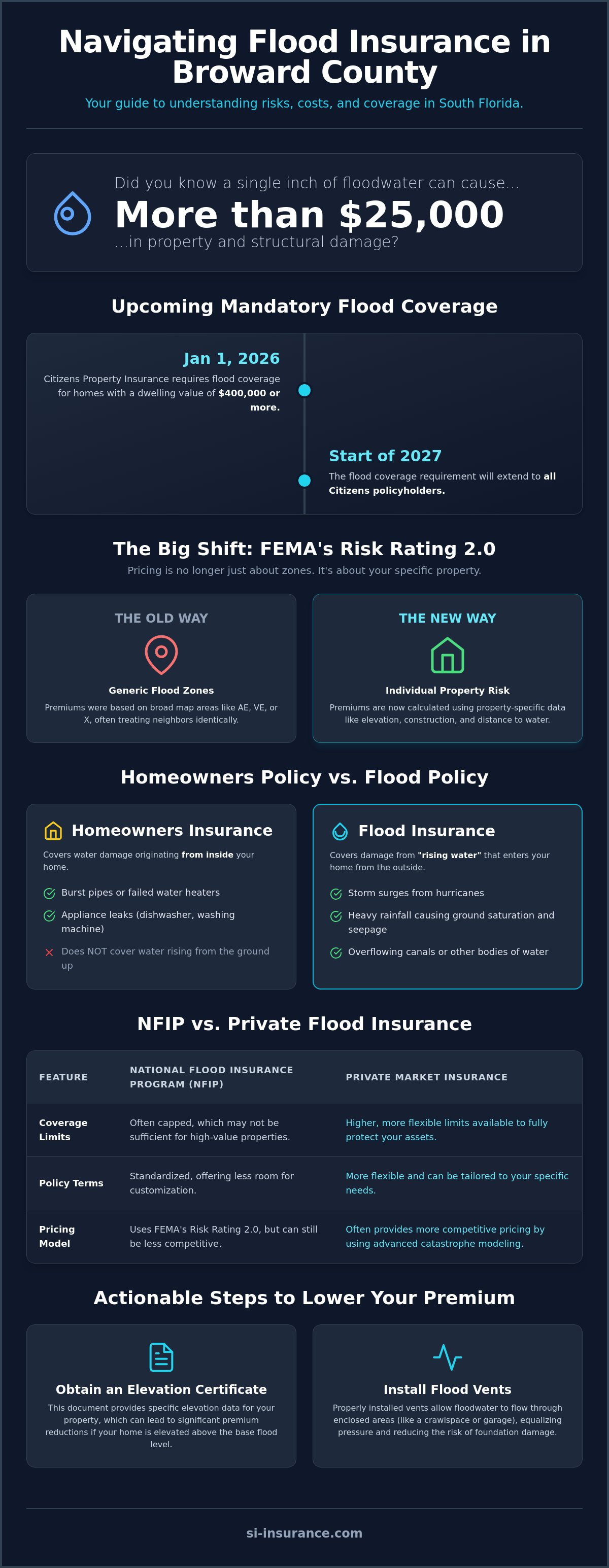

Did you know that a single inch of floodwater can result in more than $25,000 in structural and personal property damage? For residents across South Florida, assessing the flood insurance cost Broward County demands is no longer a secondary concern, but rather a vital component of a disciplined risk management strategy. As of January 1, 2026, Citizens Property Insurance already requires flood coverage for homes with a dwelling value of $400,000 or more, a requirement that will encompass all policyholders by the start of 2027.

It's understandable if you feel a sense of unease as FEMA Risk Rating 2.0 continues to shift the landscape of annual premiums. We'll provide a sophisticated breakdown of the variables driving these costs and identify the strategic opportunities available to mitigate your financial exposure. This guide examines the nuances between the National Flood Insurance Program and private market alternatives, giving you the clarity needed to secure your property with absolute confidence.

Table of Contents

Understanding Flood Risk and Insurance Requirements in Broward County

Broward County is uniquely positioned between the vast Atlantic coastline and the intricate ecosystems of the Everglades. This geography creates a dual threat that few other regions face. On one hand, coastal communities deal with the constant pressure of storm surges during hurricane season. On the other, the "Western" seepage from the Everglades can saturate the ground and cause significant flooding in inland areas like Sunrise and Weston, even without a major tropical system. Many residents are caught off guard when they discover that their standard homeowners insurance doesn't cover these events. Understanding the flood insurance cost Broward County homeowners face starts with a clear grasp of what a flood actually is: water rising from the ground up.

To better understand the risks associated with waiting to secure coverage, watch this analysis from local experts regarding the timing of your policy:

The Distinction Between Homeowners and Flood Insurance

The "rising water" rule is the primary reason claims are denied after a South Florida storm. If a pipe bursts in your kitchen or your water heater fails, that's generally a homeowners claim. However, if six inches of rain falls in two hours and water seeps under your front door from the saturated lawn, that's a flood. Relying on federal disaster assistance is a precarious financial strategy. These funds are often structured as low interest loans that must be repaid, not grants. Plus, they're only available if a federal disaster is officially declared. Most local flooding events in Broward never reach that threshold, leaving uninsured homeowners to pay for repairs out of pocket.

Broward County Flood Zones Explained: AE, VE, and X

The National Flood Insurance Program (NFIP) traditionally categorized properties into zones to determine risk and requirements. If you have a federally backed mortgage and live in a Special Flood Hazard Area (SFHA), such as an AE or VE zone, insurance is a mandatory requirement. Zone AE represents high risk areas, while Zone VE includes coastal areas with additional hazards from wave action.

In 2026, we're seeing a significant shift in behavior. Even homeowners in "Zone X," traditionally labeled as low to moderate risk, are enrolling at higher rates. This is because FEMA's Risk Rating 2.0 has moved away from broad zones toward individual property assessments. You can use the Broward County FEMA Flood Map viewer to see your current designation, but your specific elevation and distance to water now carry more weight than the color of your zone on a map. At Si Insurance Agency, we help clients look beyond these letters to understand the actual risk profile of their specific address.

Analyzing Average Flood Insurance Costs in Broward County for 2026

General insurance guides often cite a single Florida average, frequently quoted around $1,363 for NFIP policies, but these broad figures rarely reflect the reality of our local market. The actual flood insurance cost Broward County homeowners encounter is now dictated by a highly granular, property-specific approach. Since the full implementation of FEMA's Risk Rating 2.0, the era of "one-size-fits-all" pricing based solely on a flood zone map has ended. Instead, federal and private underwriters now utilize advanced catastrophe modeling to evaluate each address on its own merits.

This shift has created distinct cost tiers across the county. Inland communities like Sunrise or Weston generally see different pricing structures than coastal properties in Pompano Beach or Fort Lauderdale. While an inland home might benefit from its distance to the coast, it may still face premiums influenced by its proximity to canals or the Everglades. Conversely, a coastal property's premium is heavily weighted by its "distance to water" and its vulnerability to storm surges. It's no longer just about which side of the street you live on; it's about the precise mathematical risk your specific structure represents.

Premium Drivers: What Determines Your Broward Quote?

Several technical factors now carry more weight in your annual quote than ever before. In South Florida, the foundation type is a critical variable. Most local homes are slab-on-grade, which often faces higher risk profiles than elevated structures because the living space is closer to the potential flood level. Under the current rating methodology, the height of your first floor relative to the base flood elevation is a primary driver of cost. Even a few inches of additional elevation can lead to substantial long-term savings. Many homeowners are also choosing to assume more risk by selecting higher deductibles, which can be an effective way to manage the annual premium as federal rates continue to adjust toward full risk-based pricing.

The Community Rating System (CRS) Advantage

The Community Rating System (CRS) is a voluntary incentive program that recognizes community floodplain management. For residents in municipalities like Pompano Beach or Pembroke Pines, this program offers a significant advantage. When a city invests in better drainage, stricter building codes, or public outreach, FEMA rewards the entire community with a percentage-based discount on NFIP premiums. These discounts are applied automatically based on your city's CRS class. If you're curious about how your specific municipality's efforts impact your bottom line, you can consult with a local agent to verify your city's current standing and ensure all available credits are applied to your policy.

NFIP vs. Private Flood Insurance: Strategic Comparison

Optimizing the flood insurance cost Broward County homeowners encounter requires a side-by-side analysis of the National Flood Insurance Program (NFIP) and the rapidly expanding private market. For decades, the NFIP was the only viable option for most South Florida residents. In 2026, however, the landscape has shifted. A robust private sector now offers competitive alternatives that frequently provide broader protection and higher limits than the federal standard. Choosing between these two paths isn't just about the premium; it's about aligning your coverage with the actual replacement value of your assets.

When to Choose the National Flood Insurance Program (NFIP)

The NFIP remains the benchmark for many federally regulated mortgage lenders. Its primary strength lies in the absolute reliability of federal backing and the potential for grandfathering rates on older structures. However, the program's limitations are significant. Building coverage is capped at $250,000, and contents coverage stops at $100,000. For many modern homes in Sunrise or Pompano Beach, these limits are insufficient to cover a total loss. Additionally, the NFIP imposes a strict 30-day waiting period, which means coverage isn't immediate. It also lacks "loss of use" benefits, leaving you to pay for temporary housing out of pocket if your home is damaged.

The Benefits of Private Flood Carriers in Broward

Private carriers have emerged as a sophisticated solution for properties that exceed NFIP caps. These policies often offer replacement cost limits well into the millions, providing essential security for high-value Broward assets. Beyond just higher limits, private options often include loss of use, coverage for other structures like guest houses, and even pool or basement coverage. At Si Insurance Agency, we prioritize carriers with strong AM Best ratings to ensure our clients are protected by financially stable institutions that can withstand major catastrophic events.

Wait times are another major differentiator. While the NFIP requires a month to take effect, private carriers often offer waiting periods as short as seven to fourteen days. This agility is vital if you're closing on a home or if hurricane season is approaching. For luxury estates, we often recommend "Excess Flood" coverage. This strategy layers a private policy on top of an NFIP base, ensuring that even the most expensive coastal properties are fully indemnified against catastrophic water damage. By shopping both markets simultaneously, you can find a balance that protects your equity without overpaying for unnecessary federal surcharges.

Actionable Strategies to Lower Your Broward Flood Premium

Managing the flood insurance cost Broward County homeowners face requires moving beyond generic assumptions and toward data-driven precision. While FEMA's automated models provide a baseline for risk, they aren't infallible. Securing an Elevation Certificate (EC) remains one of the most effective ways to challenge a high premium. By providing exact, survey-grade measurements of your home's lowest floor relative to the base flood elevation, you can often prove your risk is lower than what the satellite models suggest. If your land has been built up or naturally sits higher than the surrounding area, a Letter of Map Change (LOMC) can permanently reclassify your property, potentially removing mandatory purchase requirements and lowering your rates.

Physical Mitigation and Retrofitting

Physical improvements to your property offer some of the most reliable returns on investment. In South Florida, air conditioning units and water heaters are frequently installed at ground level, making them vulnerable to the "rising water" events we discussed earlier. Elevating this mechanical equipment onto platforms above the base flood elevation can earn you direct premium credits. For business owners, professional floodproofing—such as installing removable flood barriers or reinforced doors—is a sophisticated way to protect commercial assets while reducing overhead.

It's also vital to understand the "50% Rule" when planning renovations in cities like Pompano Beach or Sunrise. If the cost of your improvements exceeds 50% of the structure's market value, local building codes require the entire building to be brought up to current flood-resistant standards. Proactively installing FEMA-compliant flood vents in your garage or crawlspace can provide immediate relief. These vents allow water to flow through the structure rather than exerting hydrostatic pressure against your foundation, which significantly lowers your risk profile in the eyes of both federal and private underwriters.

Strategic Policy Adjustments

You may also find savings by refining the scope of your policy. If you have detached structures like a shed or a gazebo that are of low value, you can often exclude them from your coverage to reduce the total insured amount. Increasing your deductible is another powerful lever, though it requires a calculated look at your liquid reserves. You must ensure that the annual premium savings outweigh the additional risk you're assuming. This holistic approach to risk management is part of a broader strategy, much like the one outlined in our Guide to Home Insurance in Florida, which helps you balance multiple lines of coverage for maximum financial efficiency.

Bundling these specialized policies through an independent agency like Si Insurance Agency ensures that your entire portfolio is managed with a singular, cohesive vision, providing both administrative ease and potential multi-policy advantages.

Securing Your Broward Property with Si Insurance Agency

The complexities of the 2026 insurance market require more than just a standard policy; they demand a partnership with a consultant who views your property through the lens of specialized risk management. Managing the flood insurance cost Broward County residents face shouldn't feel like a solitary burden or a series of automated transactions. Our agency operates as a bridge between the intricate technical requirements of FEMA and the practical needs of South Florida homeowners. By combining rigorous analysis with a commitment to long term security, we ensure that your coverage is as resilient as the structures we protect.

The Value of a Local Broward County Agent

Local knowledge is an irreplaceable asset when navigating the specific coastal dynamics of Pompano Beach or the unique inland drainage patterns of Sunrise. A national call center operates on broad data sets, but we understand the nuances of your neighborhood because we live and work here too. This proximity allows us to act as your protective guardian, especially during the high-stakes period following a storm. We don't just facilitate a policy; we engineer a risk strategy that accounts for your specific elevation, foundation type, and historical exposure. Whether you're managing a residential estate or a commercial portfolio, our role is to provide the intellectual confidence that comes from knowing every mitigation opportunity has been explored.

Requesting a Strategic Quote

To provide a quote that accurately reflects your 2026 risk profile, we take a methodical approach that goes far beyond a simple address search. While we can generate preliminary figures quickly, a truly strategic assessment requires a few key pieces of information. If you have an Elevation Certificate (EC), it serves as the cornerstone of our analysis. We also review your property's claims history and any physical mitigation steps you've already taken, such as the installation of flood vents or the elevation of mechanical systems. This detail allows us to present a side by side comparison of NFIP and private market options, ensuring you aren't paying for federal surcharges if a private carrier offers a more efficient structure.

Our independent model is designed for your benefit. We aren't beholden to a single carrier, which means we can shop a diverse network of providers to find the most competitive rates and robust coverage limits available in the current market. This transparency is vital for high value assets that require excess flood layers or specialized endorsements. When you're ready to move beyond generic estimates and secure a tailored protection plan, we invite you to Consult with a Broward County flood specialist at Si Insurance Agency. We'll guide you through the process with the precision and steady hand your investment deserves.

Securing Your Legacy Against Shifting Tides

The transition toward risk-based pricing has fundamentally changed how we approach property protection in South Florida. Effectively managing the flood insurance cost Broward County demands more than a standard policy; it requires a calculated strategy that accounts for individual elevation and specific topographic vulnerabilities. Whether you're navigating new requirements from Citizens or seeking higher limits through the private market, the goal is to align coverage with the actual replacement value of your assets. By utilizing tools like Elevation Certificates, you can take control of your premiums while ensuring absolute security.

At Si Insurance Agency, we act as your protective guardian, leveraging our deep roots in Sunrise and Pompano Beach to provide personalized risk engineering. Our independent model gives you access to both the NFIP and elite private carriers, allowing us to shop the market on your behalf. You deserve a partner who understands the high stakes of Florida’s unique landscape and provides the intellectual confidence you need. We're ready to navigate these complexities with you.

Secure a Strategic Flood Insurance Consultation with Si Insurance Agency

Protecting your property today builds a more resilient foundation for tomorrow, and we're honored to assist you in that work.

Frequently Asked Questions

Is flood insurance required in Broward County if I am not in a high-risk zone?

While federal law only mandates flood insurance for homes in Special Flood Hazard Areas with a mortgage, Florida's landscape is changing. By January 1, 2027, all Citizens Property Insurance policyholders must carry flood coverage regardless of their specific zone. It's a strategic move to secure coverage now, as many properties in "low risk" zones still experience significant damage from localized heavy rainfall and ground saturation.

What is the average cost of flood insurance in Pompano Beach versus Sunrise?

Costs are determined by individual property risk profiles rather than broad city averages. Coastal properties in Pompano Beach often see premiums influenced by storm surge potential and wave action. In contrast, inland homes in Sunrise may face risks associated with the "Western" Everglades seepage. Your specific distance to the coast or a canal will ultimately dictate the premium more than the municipal border itself.

How does FEMA Risk Rating 2.0 affect my Broward County premiums in 2026?

Risk Rating 2.0 replaces the old system of broad flood zones with a highly granular, address-specific methodology. This means your 2026 premiums are calculated using modern catastrophe models that look at your home's first floor height and proximity to water sources. This approach ensures that the flood insurance cost Broward County residents pay more accurately reflects the mathematical probability of a loss at their specific front door.

Can I switch from NFIP to private flood insurance at any time?

You can transition to the private market at any time, though it's best to do so at your policy renewal to avoid complicated pro rata refunds. Private carriers often provide much higher limits than the NFIP's $250,000 building cap. If you have a mortgage, simply ensure your lender accepts the private carrier's financial stability rating, which is something an independent agent can easily verify for you.

Does a standard homeowners policy in Florida cover any type of water damage?

Standard homeowners insurance only covers water that originates from inside the home, such as a failing appliance or a burst pipe. It doesn't provide protection against "rising water" from the ground up, which is the legal definition of a flood. Without a specialized flood policy, you're left to pay for structural repairs and contents replacement out of your own pocket after a tropical system or heavy rain event.

How long is the waiting period for a new flood insurance policy to take effect?

The National Flood Insurance Program generally requires a 30-day waiting period before a new policy becomes active. Private insurance options are much more flexible, frequently offering waiting periods as short as seven to fourteen days. Because you can't secure coverage once a storm is named and approaching, it's vital to have your policy in place well before the peak of the hurricane season.

What is an Elevation Certificate, and do I need one in Broward County?

An Elevation Certificate is a document prepared by a licensed surveyor that records the exact height of your home's lowest floor. While FEMA's new rating system uses satellite data to estimate risk, an EC provides concrete proof of your home's actual elevation. In many parts of Broward, providing this certificate can lead to significant premium reductions if it shows your home sits higher than FEMA's models assumed.

Are there discounts available for flood insurance in Broward County?

Many Broward municipalities participate in the Community Rating System, which provides automatic discounts on NFIP premiums. Cities like Pompano Beach and Sunrise earn these credits by implementing better drainage systems and stricter building codes. You can also secure individual discounts by installing FEMA-compliant flood vents or elevating your mechanical equipment, such as your AC unit, above the base flood elevation level.

Comments